WANAN YOSSINGKUM

Abstract

Following my coverage on MSCI (NYSE:MSCI), which I really useful a purchase score primarily based on my optimistic long-term view of the enterprise, the place its distinctive databases function a powerful aggressive benefit regardless of short-term earnings drags. This put up is to offer an replace on my ideas on the enterprise and inventory. I reiterate my purchase score as I proceed to see upside. I anticipate MSCI to proceed rising because it has finished so up to now, with a potential higher-than-my-expected progress charge in FY24 because it compares in opposition to a straightforward FY23 (FY23 has quite a lot of macro headwinds that ought to ease in FY24).

Funding thesis

MSCI 2Q23 outcomes have been just about in keeping with consensus, with a modest beat. Income got here in at $621 million vs. consensus $602 million, adj. EBITDA at $377 million vs. $363 million, and EPS at $3.26 vs. $3.11. Because of using the downturn playbook and gaining working leverage, EBITDA margins elevated by 70 bps to 60.7%. Nonetheless, non-recurring index income doubtless inflated the obvious beat in opposition to the consensus. This was a determine of $14 million, and if we again it out from 2Q23 reported income, the income would have been just about the identical ($607 million vs. $602 million).

When damaged down by enterprise line, we see that Index gross sales are up 13% yr over yr, Analytics gross sales are up 6%, ESG & Local weather gross sales are up 29.3%, and Non-public Belongings gross sales are up 11.9%. The whole run charge of subscriptions elevated by 11.8% yr over yr, and the run charge of asset-based charges elevated by 7.2%, for an annualized enhance of 10.7%. With Index exhibiting progress of 10.4% and Analytics rising by 5.1%, however ESG & Local weather falling by 43.2% and Non-public Belongings falling by 49.7%, whole web new recurring subscription gross sales fell by 15.0% y/y in 2Q, in comparison with a decline of twenty-two.2% in 1Q. For 2Q23, the typical AUM of ETFs pegged to MSCI indexes was $1.33 billion, representing a year-over-year enhance of three.8%.

Regardless of the section’s obvious success, I consider that the quarter’s main focus, ESG new subscription gross sales, nonetheless confronted challenges, with declines of 37.5% yr over yr in 2Q23, slowing by 2.5 share factors from 1Q23 regardless of a way more favorable comparability. That stated, administration stays optimistic about ESG’s new gross sales restoration, which I consider appears to be the case on the bottom as effectively. My concern concerning the ESG headwind in Europe was additionally addressed through the name. When requested about what must occur for ESG net-new subscription progress to reaccelerate through the 2Q23 name:

“[Europe]…it’s already starting to speed up at a small base in Europe after a interval of understanding the regulation, classifying funds, understanding the elements that they want to be able to — to be able to market these funds as sustainable funding funds and all of that… that is not essentially going to be a ramp-up instantly, however it’s starting to preface or preface, hopefully, a rise in gross sales and the likes…” 2Q23 earnings name

Primarily based on the efficiency of the inventory worth after earnings, I feel the market shares my optimism. I anticipate this pattern to proceed and strengthen past FY23 as MSCI studies improved ESG web new gross sales in subsequent quarters, printing robust relative progress in opposition to simple comps in that yr. Because of macroeconomic weak point, gross sales cycles have lengthened and budgets have been tightened, making FY24 simpler to check to FY23. Plus, MSCI noticed very robust progress in Index Subscriptions and Analytics regardless of these delicate macro headwinds, which I consider additional demonstrates the robustness of its enterprise mannequin.

Valuation

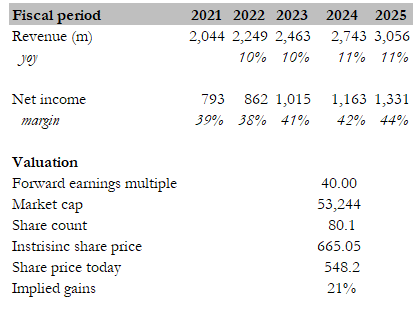

I consider the truthful worth for MSCI primarily based on my mannequin is $665. My mannequin assumptions are that MSIC will proceed to develop within the low teenagers shifting ahead, simply because it has finished for the previous years. Web margin will broaden organically because it scales income off its fixed-cost base.

The MSCI valuation of 39x has moved within the route I anticipated beforehand, in the direction of 40x its 5-year common. I consider MSCI ought to have the ability to proceed buying and selling at this a number of so long as it continues to develop because it all the time has. Some buyers could also be involved concerning the excessive absolute a number of, however friends similar to Truthful Isaac Corp. (FICO), Moody’s (MCO), and Verisk Analytics (VRSK) all commerce within the 30-plus ahead earnings vary. They will commerce at this stage as a consequence of their robust moat and excessive margin profile (MSCI and these friends have EBITDA margins starting from 40% to 70%).

Personal calculation

Danger

A decline in fairness markets has a detrimental impact on MSCI’s backside line. The affect on EBITDA, EPS, and free money circulation is exacerbated as a result of these charges are incurred by the corporate’s Index division, which has margins of 75% or extra.

Conclusion

In conclusion, I preserve a bullish outlook on MSCI primarily based on its robust aggressive benefit, regardless of short-term earnings challenges. The corporate’s distinctive databases proceed to offer an edge out there. The current 2Q23 outcomes have been largely in keeping with expectations, with a modest beat. Whereas there have been some considerations about declining ESG new subscription gross sales, administration stays optimistic about their restoration, particularly in Europe. With the potential for improved ESG gross sales and robust progress in different segments, I anticipate MSCI’s efficiency to strengthen past FY23, benefiting from simpler year-on-year comparisons in FY24. The valuation seems cheap, contemplating the corporate’s historic progress and its comparability with friends.

{kind=link}