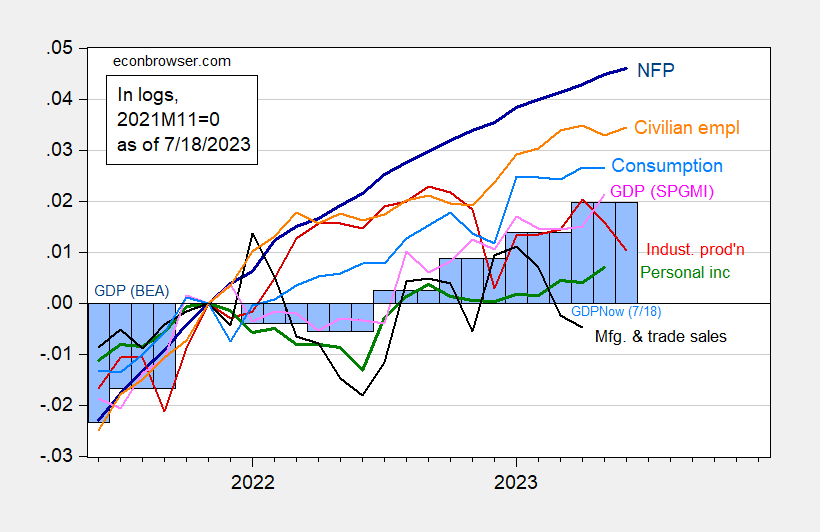

Industrial manufacturing surprises on the draw back (-0.5% vs. 0% Bloomberg consensus m/m), as does manufacturing (-0.3% vs. 0% m/m). Right here’s the image of key indicators adopted by the NBER BCDC, together with month-to-month GDP (SPGMI), in addition to GDPNow (Q2 up by 10 bps relative to 7/10).

Determine 1: Nonfarm payroll employment, NFP (darkish blue), civilian employment (orange), industrial manufacturing (crimson), private earnings excluding transfers in Ch.2012$ (inexperienced), manufacturing and commerce gross sales in Ch.2012$ (black), consumption in Ch.2012$ (gentle blue), and month-to-month GDP in Ch.2012$ (pink), GDP (blue bars), 2023Q2 is GDPNow of seven/18, all log normalized to 2021M11=0. Supply: BLS, Federal Reserve, BEA 2023Q1 third launch through FRED, Atlanta Fed (7/18), S&P Global/IHS Markit (nee Macroeconomic Advisers, IHS Markit) (7/3/2023 launch), and writer’s calculations.

GDPNow for Q2 at 2.4% SAAR as of right now. GS at 2.5%, whereas SPGMI at 1.7%.

Retail gross sales have been typically underneath consensus. Right here’re time sequence of business manufacturing, manufacturing manufacturing, and retail gross sales deflated by remaining demand/completed items PPI, over the identical interval proven in Determine 1.

Determine 2: Industrial manufacturing (crimson, left log scale), manufacturing manufacturing (purple, left log scale), and retail gross sales ex-food companies deflated by PPI remaining demand completed items, thousands and thousands 1982$ (inexperienced, proper log scale), all seasonally adjusted. Supply: Federal Reserve, Commerce Division, BLS all through FRED, and writer’s calculations.

Industrial manufacturing surprises on the draw back (-0.5% vs. 0% Bloomberg consensus m/m), as does manufacturing (-0.3% vs. 0% m/m). Right here’s the image of key indicators adopted by the NBER BCDC, together with month-to-month GDP (SPGMI), in addition to GDPNow (Q2 up by 10 bps relative to 7/10).

Determine 1: Nonfarm payroll employment, NFP (darkish blue), civilian employment (orange), industrial manufacturing (crimson), private earnings excluding transfers in Ch.2012$ (inexperienced), manufacturing and commerce gross sales in Ch.2012$ (black), consumption in Ch.2012$ (gentle blue), and month-to-month GDP in Ch.2012$ (pink), GDP (blue bars), 2023Q2 is GDPNow of seven/18, all log normalized to 2021M11=0. Supply: BLS, Federal Reserve, BEA 2023Q1 third launch through FRED, Atlanta Fed (7/18), S&P Global/IHS Markit (nee Macroeconomic Advisers, IHS Markit) (7/3/2023 launch), and writer’s calculations.

GDPNow for Q2 at 2.4% SAAR as of right now. GS at 2.5%, whereas SPGMI at 1.7%.

Retail gross sales have been typically underneath consensus. Right here’re time sequence of business manufacturing, manufacturing manufacturing, and retail gross sales deflated by remaining demand/completed items PPI, over the identical interval proven in Determine 1.

Determine 2: Industrial manufacturing (crimson, left log scale), manufacturing manufacturing (purple, left log scale), and retail gross sales ex-food companies deflated by PPI remaining demand completed items, thousands and thousands 1982$ (inexperienced, proper log scale), all seasonally adjusted. Supply: Federal Reserve, Commerce Division, BLS all through FRED, and writer’s calculations.

{kind=link}