FatCamera

Overview

I like to recommend a purchase score for Elevance (NYSE:ELV) as I count on the enterprise to hit administration’s FY27 goal of rising EPS by 15%, which is able to doubtless lead to multiples shifting as much as be consistent with friends. This can be a reiteration of my earlier buy rating for ELV, the place I believed it will be straightforward for ELV to fulfill its progress targets by 2027. In that situation, the corporate would seem low cost because it was buying and selling at lower than 10x PE based mostly on FY27 numbers.

2Q23 outcomes have been stable, resulting in a beat and lift

Adjusted EPS for ELV got here in at $9.04, exceeding the $8.78 consensus estimate, and the corporate elevated its adjusted EPS steering for 2023 by $0.15, to greater than $32.85. In my view, the beat and lift efficiency is a mirrored image of stable basic efficiency and can go a great distance towards easing current worries about the associated fee development and utilization. The advance in 2Q outcomes was pushed by increased MLR, barely increased SG&A, and better funding earnings than anticipated.

It is price noting that ELV as soon as once more locations an emphasis on its MCR steering and sticks to the identical message, which is that the upper utilization in comparison with pre-pandemic ranges is in keeping with their pricing and expectations. I imagine this reassuring communication has helped calm investor fears and improved the managed care sector as a complete. I might remind {that a} massive bear narrative surrounding the inventory was the MA utilization stress, which was flagged by ELV’s friends (UnitedHealth Group and Humana Inc.). That stated, I might level out that ELV has structurally much less publicity to Medicare.

Trying into the longer term, I’m assured that ELV is poised to attain its Well being Advantages margin goal on account of a number of elements. These embody sturdy industrial pricing, steady Medicaid margins, and constant MA margins, excluding Puerto Rico. As ELV continues its efforts in direction of long-term targets, reminiscent of implementing increased pricing and revised advantages within the MA sector, I count on its margins to expertise continued progress in 2024. ELV has already noticed early optimistic recapture and acuity knowledge factors, and the corporate stories that state Medicaid charges are both assembly or surpassing their expectations. Nevertheless, I imagine that the potential impression of redeterminations stays a major concern for traders.

Redeterminations impression manageable

As of 2Q23, ELV’s Medicaid membership stood at 11.76 million, and the corporate’s administration remained assured that between 40 and 45 p.c of latest members gained in the course of the redetermination freeze would stay on Medicaid, 20 to 25 p.c would change to employer protection, and 20 to 25 p.c would land in employer protection, with a lag in recapture anticipated. Nevertheless, it’s feared that margins shall be eroded as the danger pool worsens because of the disenrollment of the double counted inhabitants. Excellent news is that administration expects the danger hall payable stability to soak up among the blow that twin enrollment will trigger. In addition they identified the second half of the 12 months, when alternatives abound and industrial progress is predicted to re-accelerate by 2024.

Carelon Providers

Regardless of the behavioral and MSK stress, Carelon Providers’ efficiency stays sturdy. ELV famous that Carelon Providers’ working achieve was dampened by increased utilization of behavioral companies in the course of the quarter as a result of the corporate takes capitated threat for each behavioral companies and MSK. This 12 months, administration stated it anticipated increased utilization, so it set capitated charges accordingly. I count on Carelon Providers margins to be increased in 2024 on account of the corporate’s pricing reflecting its revised utilization assumptions.

Valuation

Personal mannequin

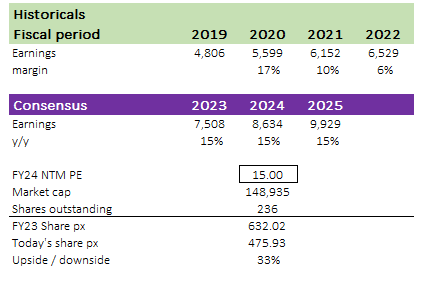

Utilizing administration’s long-term (I wrote about it in my earlier replace) EPS progress steering of 15%, I worth ELV at $475.93. As ELV demonstrates sturdy EPS progress, I imagine the market will re-rate valuation upwards to friends’ ranges of 15x ahead PE. ELV at present trades at 13.5x ahead PE, whereas UnitedHealth Group trades at 19x and Humana trades at 15x. This massive valuation low cost is, I imagine, on account of ELV’s slowed anticipated earnings progress fee, which I imagine shouldn’t be reflecting administration’s long-term steering.

Danger

Any surprising enhance in medical value traits has the potential to considerably cut back working earnings.

Conclusion

In conclusion, I like to recommend a purchase score for ELV inventory based mostly on its stable 2Q23 efficiency and its potential to fulfill administration’s FY27 targets. The corporate’s beat and lift outcomes replicate sturdy basic efficiency, easing issues about value traits and utilization. ELV’s give attention to MCR steering has supplied reassurance to traders, and its decrease publicity to Medicare mitigates utilization stress dangers. Trying forward, ELV’s Well being Advantages margin goal appears achievable, supported by industrial pricing and steady Medicaid margins. Nevertheless, it is important to be aware of any surprising enhance in medical value traits that would impression working earnings.

{kind=link}