Scott Olson

DraftKings (NASDAQ:DKNG) has been a giant winner in 2023, because the inventory benefited from a return of progress investing urge for food regardless of persistently greater rates of interest. DKNG has delivered sturdy top-line progress coupled with market share features this yr and continues to seem like a high tier on-line playing firm. Administration is guiding for “meaningfully” optimistic adjusted EBITDA era subsequent yr and simply delivered optimistic adjusted EBITDA within the newest quarter. Regardless of the stable outcomes, I’m of the view that this rally has gone too far. The inventory seems to be pricing in good execution, however the present setup is arguably certainly one of vital execution threat given ongoing GAAP losses and the upcoming entrance of a brand new sports activities betting competitor. That mentioned, some traders should still be drawn to DKNG as it’s legitimately an owner-operator firm, with the CEO having loads of “pores and skin in the sport.”

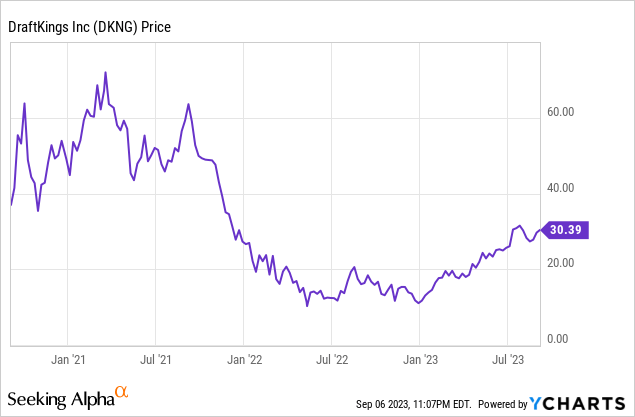

DKNG Inventory Worth

DKNG was one of the hyped SPACs amidst the pandemic, and noticed its inventory crash to the low double-digits throughout the tech crash. The inventory is now up round 200% greater from these lows.

I last covered DKNG in Could of 2021 the place I defined why the inventory was too costly even incorporating the sturdy progress outlook. The inventory has since fallen 36%, however I stay impartial on the valuation because the risk-reward proposition isn’t wanting so favorable for potential traders.

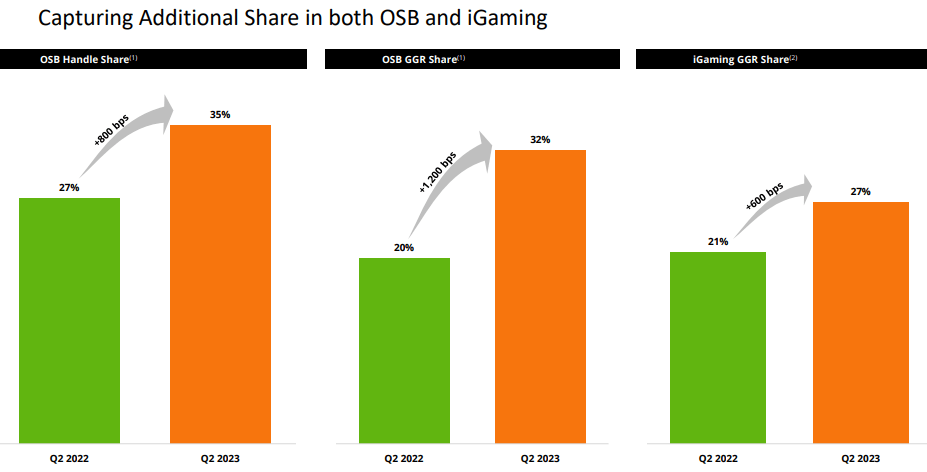

DKNG Inventory Key Metrics

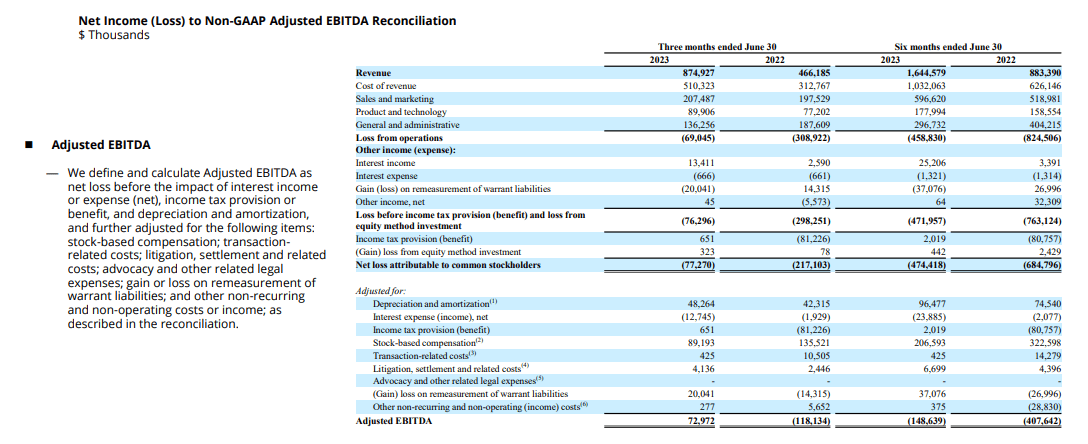

In its most up-to-date quarter, DKNG delivered 88% YoY income progress to $875 million and $73 million of optimistic adjusted EBITDA, up $191 million YoY. DKNG noticed sturdy market share features in each on-line sports activities betting and iGaming.

2023 Q2 Presentation

It has change into clear that DKNG has been capable of differentiate its product choices via innovation and ease of gameplay – traders might have beforehand feared in regards to the dangers of commoditization. DKNG might face one other take a look at on this regard within the close to future with Penn Gaming (PENN) putting a cope with Disney (DIS) to license the ESPN name for online sports betting.

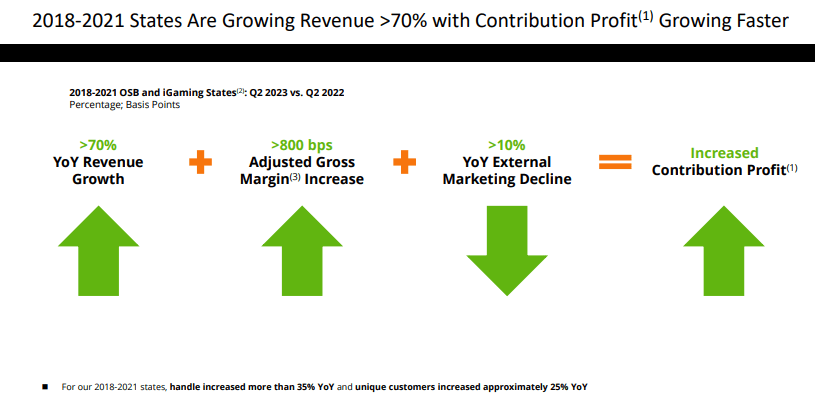

DKNG famous that it was seeing sustained sturdy progress from states that got here on-line in 2018 to 2021 together with lowered exterior advertising and marketing spend, resulting in considerably improved contribution margins.

2023 Q2 Presentation

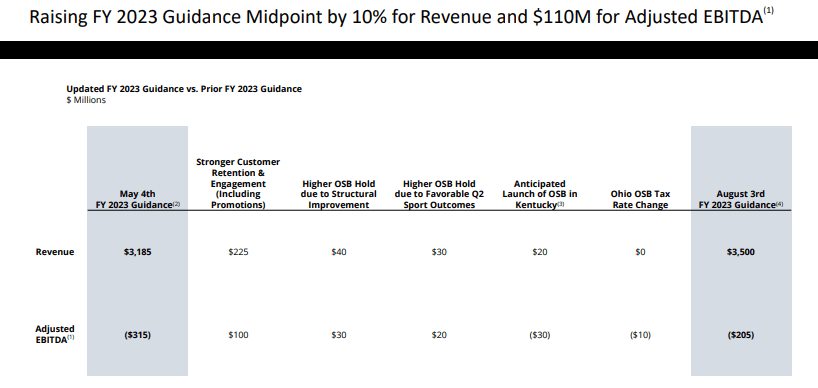

The sturdy outcomes led DKNG to boost full-year steerage for each income and adjusted EBITDA, as administration now expects $3.5 billion in full-year income and $205 million in adjusted EBITDA losses.

2023 Q2 Presentation

DKNG ended the quarter with $1.1 billion of money versus $1.3 billion of convertible notes. Administration expects to finish the yr with over $1 billion of money and to generate “meaningfully optimistic” adjusted EBITDA in 2024. Like many different tech firms, DKNG has accomplished an amazing job in pivoting in direction of profitability amidst the rising rate of interest setting.

On the conference call, administration famous that the focused September launch of Kentucky’s Horse Racing Fee is anticipated to spice up revenues by $20 million and negatively influence adjusted EBITDA by $30 million – DKNG usually invests aggressively in new markets so as to win market share. DKNG expects Ohio’s elevated tax price from 10% to twenty% to result in $10 million of further prices this yr.

Is DKNG Inventory A Purchase, Promote, or Maintain?

DKNG represents a pure-play funding on the expansion of on-line playing. DKNG is just like the “Amazon of casinos.”

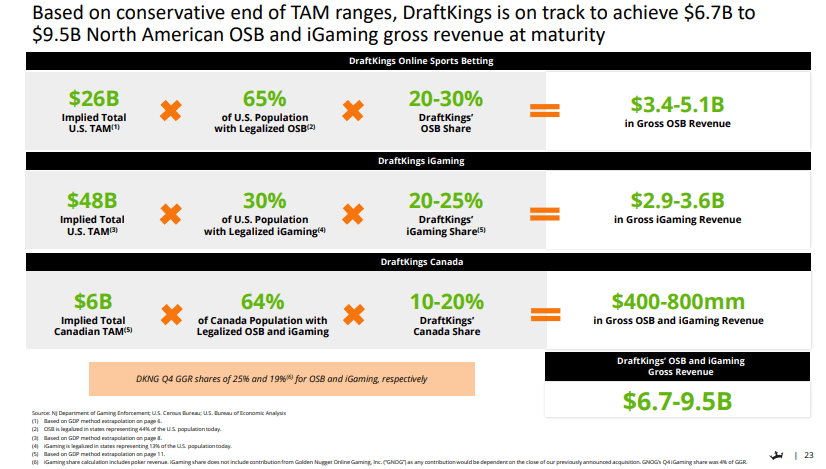

2022 Investor Day

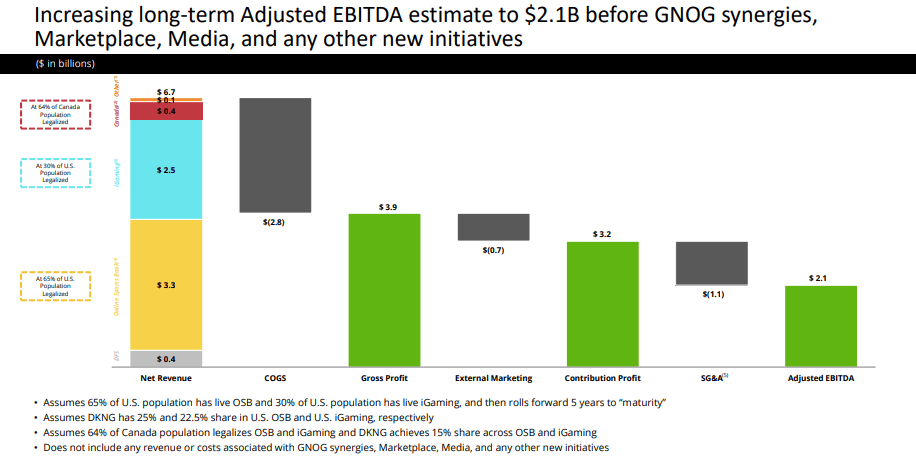

At its 2022 Investor Day, administration outlined a path to between $6.7 billion and $9.5 billion in income at “maturity.”

2022 Investor Day

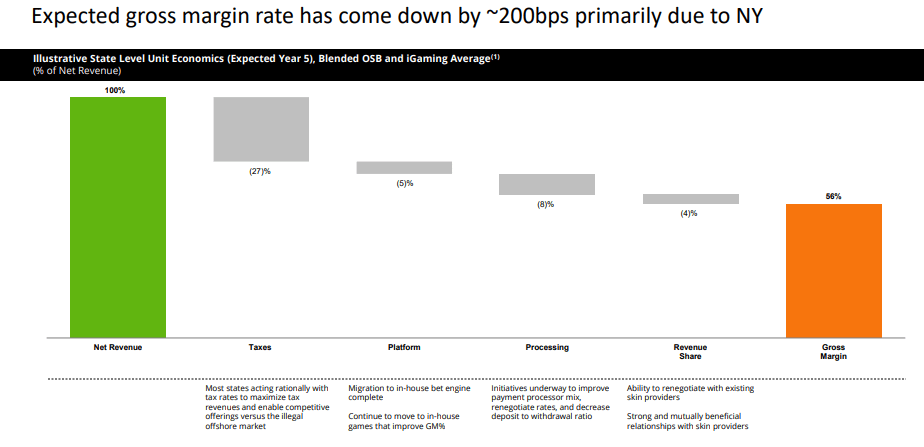

DKNG expects gross margins to rise from the 43% degree right now to 56% at maturity. Native state governments cost a big particular tax price because of playing being a “sinful” exercise. I word that this tax is along with any company earnings tax payable to the federal authorities.

2022 Investor Day

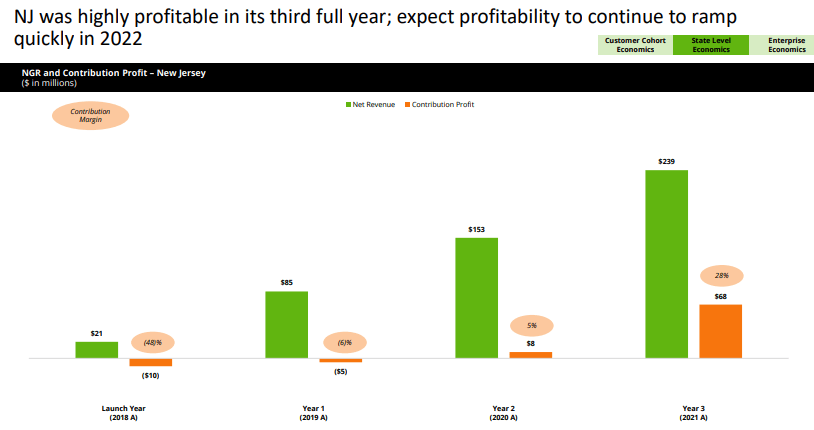

DKNG notes that whereas contribution margins are poor within the early years of recent markets, they have a tendency to enhance quickly as the corporate can spend much less and fewer on exterior advertising and marketing.

2022 Investor Day

DKNG expects to generate a 31% adjusted EBITDA margin at maturity as advertising and marketing spend ranges and the corporate achieves working leverage.

2022 Investor Day

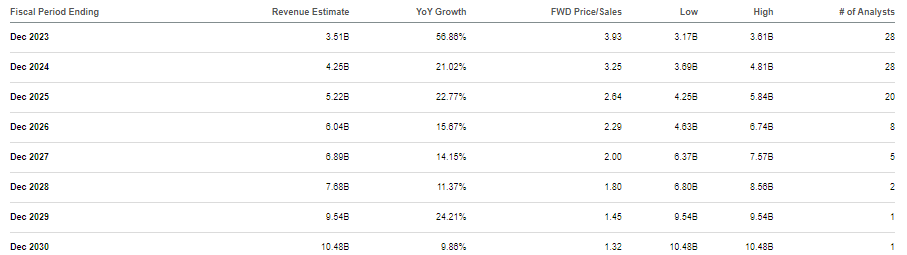

On the convention name, administration said that they don’t see “materials adjustments to both of these targets.” Consensus estimates name for DKNG to hit the excessive finish of that long-term steerage in 2029.

In search of Alpha

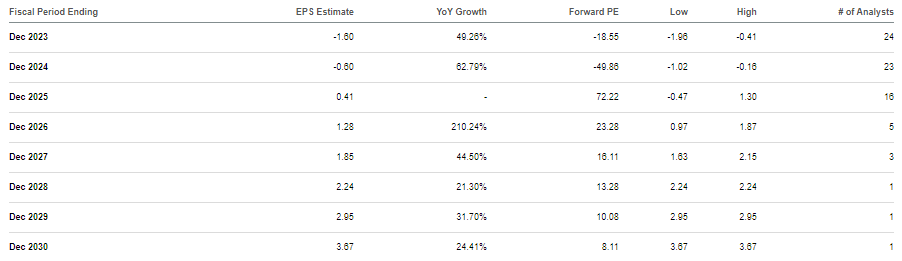

That means round $3 billion in 2029 adjusted EBITDA. Consensus estimates have DKNG incomes a 14.5% web margin in 2029.

In search of Alpha

Whereas it’s attainable that DKNG might be able to convert greater than this implied 50% of adjusted EBITDA into web earnings sooner or later, consensus estimates are arguably very cheap, if not optimistic. We are able to see under that adjusted EBITDA provides again objects reminiscent of depreciation & amortization, stock-based compensation, and earnings taxes.

2023 Q2 Presentation

Being a digital-first firm, precise CapEx outlay tends to be lower than depreciation & amortization, however it isn’t immaterial. DKNG spent $96 million on CapEx and software program amortization in 2022 or 4.3% of income, and is guiding for $120 million this yr, or 3.4% of income. Inventory-based compensation made up greater than the adjusted EBITDA generated within the newest quarter. Maybe that finally ranges off to round 25% of adjusted EBITDA. After then accounting for earnings taxes and future curiosity bills, we will see {that a} 50% conversion to web earnings is not precisely a lowball guess.

What sort of earnings a number of ought to the inventory commerce at? Maybe the inventory deserves to commerce at a premium to the 6x a number of at PENN, as on-line playing is arguably the disruptor. However on-line playing could also be extra inclined to cost competitors than experience-based land casinos, and on-line playing is a extremely aggressive house with rivals like Fanduel, BetMGM (MGM), and the aforementioned ESPN-PENN tie-up. Even so, let’s assume a 2x value to earnings progress ratio (‘PEG ratio’). Primarily based on 10% progress exiting 2029, DKNG would possibly commerce at round 20x earnings. That means a inventory value of $59 per share in 2029, or round 11% annual upside potential over the subsequent 6.3 years. At a 25x earnings a number of the inventory would possibly commerce at $74 per share, providing 14.5% annual upside potential. DKNG isn’t even adjusted EBITDA worthwhile on a full-year foundation, however the inventory is providing arguably meager upside potential even assuming a wealthy exit a number of. Some readers might argue that with the market buying and selling close to all-time highs, projected returns for the broader market may not be as excessive as prior to now. I’ve some doubts relating to such views, besides I feel that it might be a mistake to decrease one’s return hurdles based mostly on such a view, particularly in relation to greater threat names like DKNG. By the way, a inventory value of round $17.50 will increase the potential annual upside potential to over 20% (assuming a $59 inventory value in 2029).

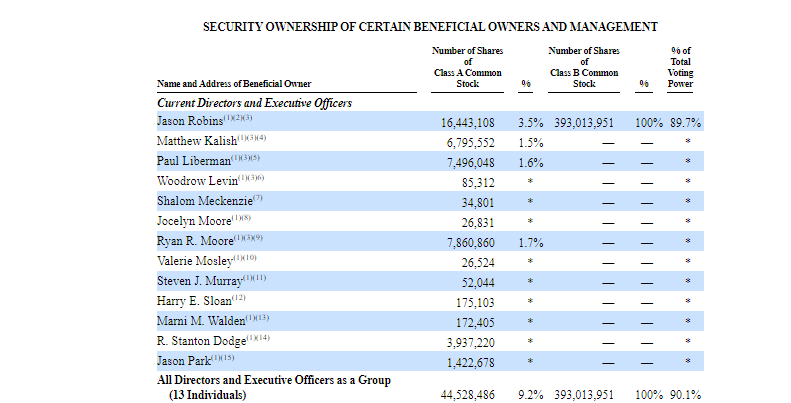

I ought to level out that DKNG is an owner-operator firm, as its founders and administration personal a big stake within the enterprise. CEO and co-founder Jason Robins owns round $500 million price of inventory. I word that the 393 million Class B shares owned by CEO Robins give him voting management of the corporate, however carry no financial rights.

2023 DEF 14A

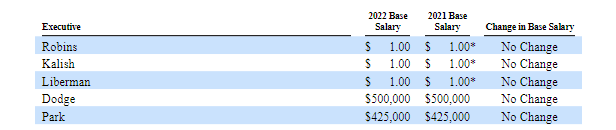

CEO Robins and two different executives have elected to obtain a $1 base wage via 2023.

2023 DEF 14A

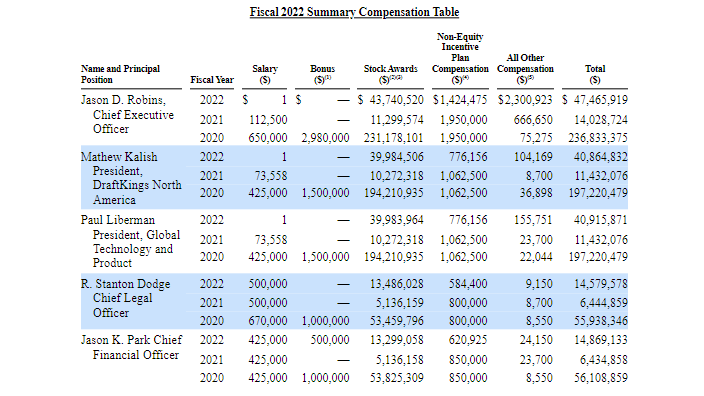

I mustn’t omit that these executives nonetheless had been nonetheless generously compensated with inventory awards over the previous 2 years.

2023 DEF 14A

I would not be stunned to see DKNG commerce as much as very bubbly valuations, however the present inventory value requires aggressive long-term assumptions so as to justify an inadequate potential return. I’ll proceed to watch DKNG as it’s clearly a high tier operator within the on-line playing sector, however should train self-discipline in ready for higher valuations.

{kind=link}