loveguli

Funding Thesis

Yum China Holdings, Inc. (NYSE:YUMC) has good income and margin development prospects forward. The corporate’s income development ought to profit from a gradual improve in mobility as a consequence of financial reopening after a three-year-long lockdown. This could unleash the pent-up demand for dine-in providers, and improve visitor visitors. Additional, a rise in engaging provides and promotional actions, power within the supply and digital channels, and new unit enlargement must also assist the gross sales development shifting ahead.

On the margins entrance, the corporate ought to profit from bettering gross sales leverage, rising productiveness, and effectivity beneficial properties within the eating places. Along with encouraging development prospects, the valuation can also be engaging with the inventory buying and selling at a reduction to the historic averages. Therefore, I’ve a purchase ranking on the inventory.

Income Evaluation and Outlook

In my previous article, I talked about the corporate’s development prospects forward given the financial reopening of China, publish a three-year-long lockdown. The corporate has reported its first and second-quarter earnings of 2023 since then and posted good outcomes. Nevertheless, the inventory worth corrected publish my earlier article in step with the broader market correction, regardless of good outcomes. I imagine the current inventory correction has made the inventory a good higher purchase given bettering fundamentals.

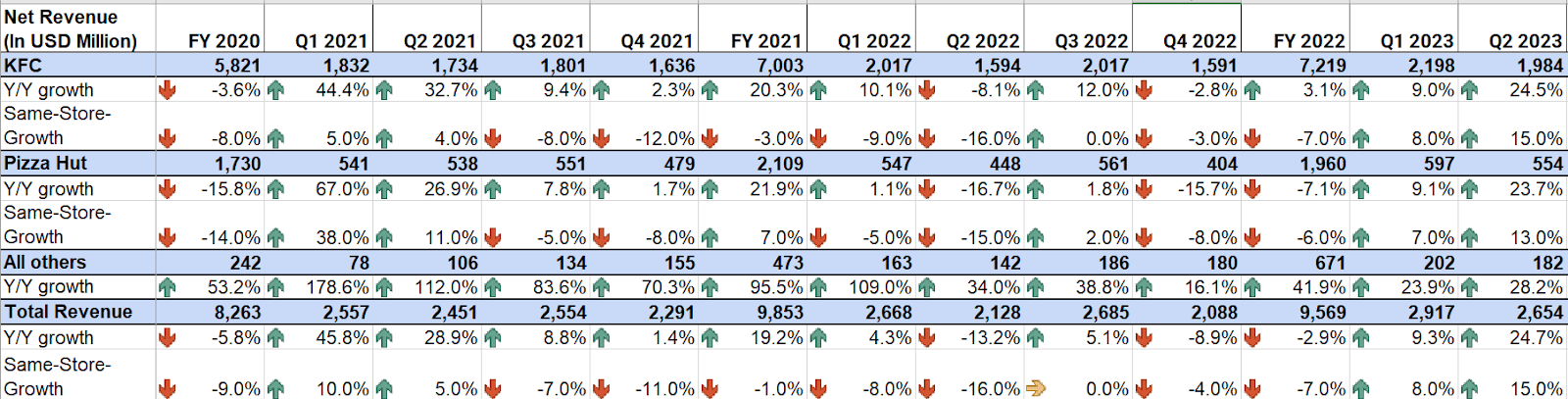

Within the final quarter, the corporate noticed recovering gross sales development as a result of reopening of the economic system, which supported pent-up demand for dine-in meals providers. As well as, the corporate additionally noticed an excellent contribution from greater transactions as a result of firm’s promotions and worth choices together with the pent-up demand. New restaurant openings additionally benefited the gross sales development. This resulted in a 24.7% YoY improve in complete gross sales to $2.6 billion. Excluding a 6 share level impression from unfavorable overseas forex, gross sales grew by 32% YoY. This good income development mirrored a 15% YoY same-store gross sales and the remaining contribution from new restaurant growth. The simple comparisons from the earlier yr’s quarter as a consequence of short-term restaurant closures on account of COVID-19 additionally helped.

YUMC’s Historic Income (Firm Information, GS Analytics Analysis)

Wanting ahead, I imagine the corporate ought to be capable to get well its income development additional because it continues to learn from financial reopening and easing of mobility restrictions. Additional, the expansion ought to be aided by a rise in worth provides and promotions, power in supply and digital channels, and new unit growth.

China is witnessing a gradual reopening of its economic system and a return to normalcy after the three-year-long lockdowns and restrictions on mobility. Because the economic system continues to adapt to the post-pandemic routine, mobility ought to additional improve and restaurant visitors on the firm’s eating places ought to be boosted as a consequence of pent-up demand. The post-pandemic world is seeing a major surge in pent-up demand for dine-in providers. After enduring lockdowns and restrictions, individuals are wanting to return to the social and culinary experiences that eating places supply. Whether or not it is celebrating missed events, or just having fun with the comfort of eating out, shoppers are flocking to eating places looking for a way of normalcy. This resurgence in demand is a promising signal for the meals service business. So, the pent-up want for dine-in providers ought to assist the business’s restoration in a post-pandemic world and likewise assist YUMC’s gross sales development shifting ahead.

Moreover, the corporate can also be targeted on rising its visitor visitors. For this objective, the corporate has been rising worth choices to assist the buyer take care of inflation whereas having fun with the long-waited expertise of dine-in post-pandemic. The corporate has expanded its pricing choices by introducing promotions and reducing entry-level prices. Up to now yr, KFC successfully rolled out interesting promotions, resembling KFC’s Loopy Thursday, which has been serving to drive 50% extra gross sales than different weekdays, and the continued Sunday Purchase Extra Save Extra deal at KFC, which is boosting weekend gross sales. For Pizza Hut, Scream Wednesday the place the corporate provides completely different meal selections from pizza, steak, rice, and pasta to appetizers at a gorgeous worth of US$3 to US$5, helps improve visitor visitors.

These efforts resulted in a 21 share level improve in transactions in KFC and a 27 share level improve at Pizza Hut within the second quarter of 2023, serving to the same-store gross sales development. The corporate plans to additional speed up these worth and promotional provides shifting forward as properly with a view to seize the pent-up demand whereas supporting shoppers throughout inflationary instances. So, I anticipate these will increase in promotions ought to proceed to assist the same-store gross sales development shifting ahead.

Furthermore, throughout the pandemic, the corporate noticed an excellent surge in on-line supply channels which helped in partially offsetting the short-term dine-in closures. Now because the dine-in providers have resumed, supply and digital channel gross sales development are normalising. Nevertheless, regardless of normalization, it’s nonetheless properly above the pre-pandemic and at very wholesome ranges. Within the second quarter of 2023, supply gross sales grew by 25% YoY at KFC and by 9% YoY at Pizza Hut on a relentless forex foundation. The corporate is working with third-party on-line platforms to broaden its attain, for instance, pay as you go low cost vouchers and geographically particular offers, that are serving to entice new members and have elevated the spending of present clients.

Additional, digital gross sales together with supply, cellular orders, and kiosk orders, accounted for about 90% of KFC and Pizza Hut’s Firm gross sales within the second quarter of 2023, with 66% of member gross sales, up 400 bps YoY. This was a results of rising loyalty program membership which exceeded 445 million members, up 15.6% YoY. To additional recruit and have interaction members, YUMC is introducing fascinating member-exclusive perks to clients, resembling app-exclusive new product presales and fortunate attracts using member factors. So, I anticipate supply and digital channels to maintain fueling the general gross sales development regardless of their development price normalization.

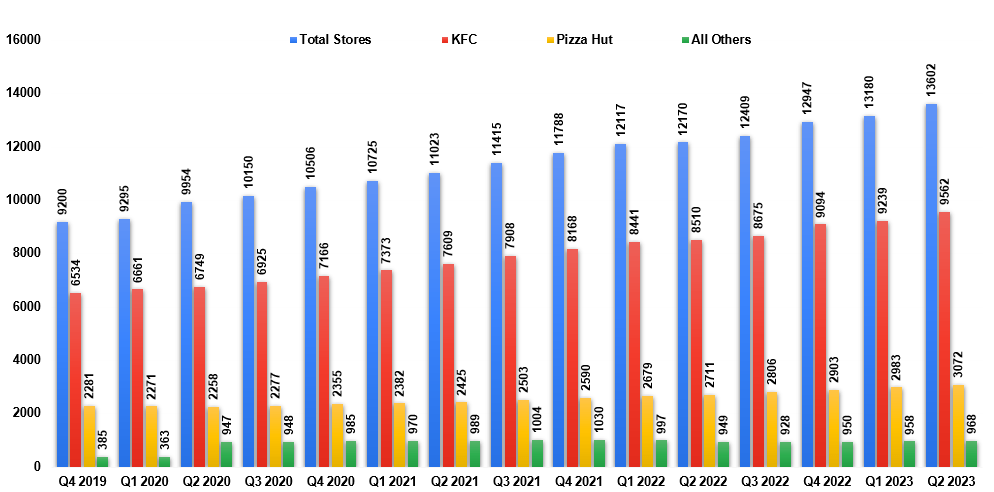

Lastly, the corporate can also be properly poised to broaden its gross sales development with the assistance of recent unit growth. Over the current years, the corporate has been specializing in alternatives to broaden its attain and improve market share, and it has accelerated the online unit growth. The corporate noticed an 11.8% YoY improve within the second quarter of 2023 with a 3.2% sequential improve to a complete unit depend of 13,602.

YUMC’s Historic Retailer Rely Development (Firm Information, GS Analytics Analysis)

This improve in unit growth has helped the corporate improve its market share and, as post-pandemic normalcy returns, this robust development in restaurant footprint ought to assist the gross sales development. The corporate plans to maintain the tempo of recent unit growth fixed shifting ahead as properly with a objective to open ~445 to 645 web new shops within the second half of 2023 to succeed in the goal of 1100 to 1300 web new unit growth for the present yr.

Furthermore, the corporate is increasing its footprint each in top-tier cities in addition to low-tier cities which helps entice shoppers throughout geographies and earnings brackets. Whereas it’s serving to the corporate acquire good traction and pent-up demand, the corporate can also be targeted on increasing in numerous geographies by using completely different channels resembling universities, hospitals, and high-speed railway service stations. It is usually diversifying its retailer codecs by opening up smaller format shops targeted on takeaway and supply which requires much less funding and has an excellent payback of two years. These shops are serving to in boosting off-premise gross sales and likewise improve market share. Additional, these additionally embody pop-up shops and meals vans which assist entice visitors by rising buyer comfort and retailer accessibility. The corporate plans to open extra of those retailer codecs for holidays and festivals, which ought to assist add incremental visitor visitors. So, I anticipate the corporate to speed up its top-line development by means of new unit growth within the coming years.

Therefore, I stay optimistic in regards to the firm’s gross sales development prospects forward.

Margin Evaluation and Outlook

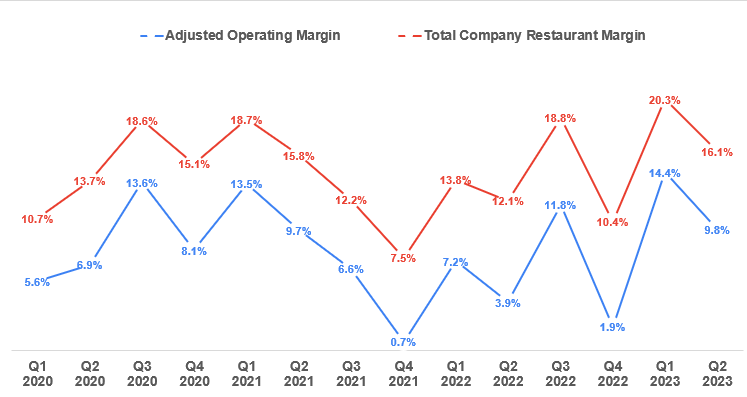

Within the second quarter of 2023, the corporate’s margins noticed favourability from commodity and wage prices as a consequence of quantity leverage. As well as, worth will increase additionally helped the corporate’s margins. Furthermore, cost-savings and productiveness enhancements additionally supported the margin development within the quarter. This resulted in a 400 bps YoY improve in complete company-owned restaurant-level margins to 16.1%. On a consolidated foundation, the adjusted working margin elevated by 590 bps YoY to 9.8%.

YUMC’s Historic Firm-Owned Restaurant Margin and Adjusted Working Margin (Firm Information, GS Analytics Analysis)

Wanting ahead, I imagine the corporate ought to be capable to ship margin development. One of many greatest margin drivers for any firm is gross sales leverage and, over the previous three years, YUMC noticed headwinds from gross sales deleverage as a consequence of declining gross sales. Now, that gross sales development is recovering, the corporate is ready to drive gross sales leverage. So, I anticipate because the gross sales proceed to get well, gross sales leverage ought to assist in delivering margin development shifting ahead within the yr.

Furthermore, the corporate can also be seeing advantages from productiveness and effectivity initiatives accelerating. The corporate is enhancing its provide chain community with superior applied sciences with a view to enhance retailer economics. These initiatives have helped the corporate save prices by means of provide chain efficiencies and rising labor productiveness. The corporate has additionally taken steps to spice up operational efficiencies inside its eating places. These efforts embody using digitization to permit retailer administration groups to work throughout a number of shops. AI-driven techniques applied in these initiatives have streamlined administrative duties, liberating up Restaurant Normal Managers (RGMs) from repetitive duties. So, by additional integrating its retailer administration system, the corporate has improved the visibility into retailer operations and in flip, supporting RGMs in additional successfully managing a number of shops whereas sustaining operational requirements. These initiatives ought to unlock additional value financial savings and enhance productiveness.

Furthermore, as mentioned within the income evaluation, the corporate has accelerated its new unit growth, and these new retailer openings are geared up with all these productiveness measures and enhanced digital infrastructure. This has meaningfully improved the per-store economics of recent shops as in comparison with the shops within the pre-pandemic period. Round 40% of YUMC’s present shops have opened after 2019, and presently, the corporate is opening a median of 1 new retailer each 5 hours. This increasing portfolio of shops is well-positioned to function effectively within the altering market panorama as a result of firm’s effectivity initiatives. Subsequently, as the corporate continues so as to add new items, the related enhancements in effectivity and price construction ought to proceed to spice up margins in the long term. Therefore, I stay optimistic in regards to the firm’s margin development prospects forward.

Valuation and Conclusion

Yum China is presently buying and selling at a ahead P/E ratio of 24.66x primarily based on the FY23 consensus EPS estimate of $2.18, and 20.72x primarily based on the FY24 consensus EPS estimate of $2.59. That is at a reduction to its 5-year historic common ahead P/E of 34.40x. Submit my earlier article, the inventory worth noticed a correction largely as a consequence of broader market correction and likewise as a consequence of some issues round decrease shopper spending in an inflationary atmosphere.

Nevertheless, I’m not nervous in regards to the firm’s development prospects forward, as the corporate is properly poised to learn from a gradual return to normalcy and additional improve in mobility shifting ahead. The pent-up demand for dine-in providers, rising promotional actions, power in supply and digital channels, new unit growth, gross sales leverage, and improved retailer economics ought to assist the corporate’s development prospects forward. This could offset any weak point arising from macroeconomic uncertainty and, therefore, I imagine the current correction has made the inventory much more engaging by way of valuation. So, I’m persevering with to have a purchase ranking on the inventory. I’m additionally trying ahead to listening to administration updates on the corporate’s long-term development plans within the upcoming Investor Day on 14th September 2023, which I imagine ought to additional enhance the funding group’s understanding of the corporate’s long-term prospects and act as a catalyst for the inventory.

{kind=link}