MahmutSonmez

Oil costs are the discuss of Wall Road now that Q3 earnings season has come to an finish. WTI is above $85, at recent 2023 highs, as Brent approaches $90. Whereas many sell-side analysts have assumed an oil worth within the $70s to low $80s, any bump up towards $90 and even $100 might result in a slew of earnings upgrades and better multiples throughout the low-P/E Power sector.

I’m reiterating my buy score on Devon Power (NYSE:DVN) for its low valuation and stable free money move yield, although the chart nonetheless has some work to do.

WTI Jumps to Recent YTD Highs

TradingView

In keeping with Financial institution of America World Analysis, DVN is an unbiased vitality firm that explores for, develops, and produces oil, pure fuel, and pure fuel liquids in america. It is a diversified large-cap US E&P firm with fourth-quarter 2022 every day manufacturing was roughly 315,000 barrels of oil, about 150,000 barrels of pure fuel liquids and greater than 1 billion cubic ft of pure fuel. It operates in Delaware, Anadarko, Williston, Eagle Ford, and Powder River Basin.

The Oklahoma-based $33.9 billion market cap oil and fuel exploration and manufacturing business firm throughout the Power sector trades at a low 7.2 trailing 12-month GAAP price-to-earnings ratio and pays a hard and fast and variable dividend, at present at a 3.7% ahead yield if we extrapolate ahead the latest dividend announcement. Forward of earnings on the finish of subsequent month, the inventory has a modest 25% implied volatility proportion and a brief curiosity of simply 2.2%.

Again in early August, the corporate issued a considerably gentle Q2 report. Working earnings per share verified at $1.18, a one-cent miss, whereas quarterly income got here in 39% decrease than year-ago ranges – a modest miss. The excellent news was that its oil manufacturing reached an all-time excessive of 323,000 barrels per day in Q2 and the agency declared a fixed-plus-variable dividend payout of $0.49 per share based mostly on the outcomes. In all, it was a lukewarm report, and lowered pure fuel costs undoubtedly dinged income whereas share buybacks had been a assist.

Free money move was about what analysts had been anticipating and the administration crew maintained its full-year capex and manufacturing steerage. The agency continues to goal to return as much as 50% of its free money move to shareholders by way of dividends and share repurchases, although I think about we would see a decrease dividend price in comparison with historical past with extra of a buyback focus. Then in mid-August, analysts at Mizuho removed Devon from its high E&P picks however stored the Power title as a purchase.

Key dangers to the bullish thesis embrace any downward strikes in oil and fuel costs, which might harm margins and free money move. Furthermore, firm-specific delays in upstream initiatives might end in Devon not assembly its manufacturing targets. Increased capex bills might chew into free money move and potential shareholder accretive actions.

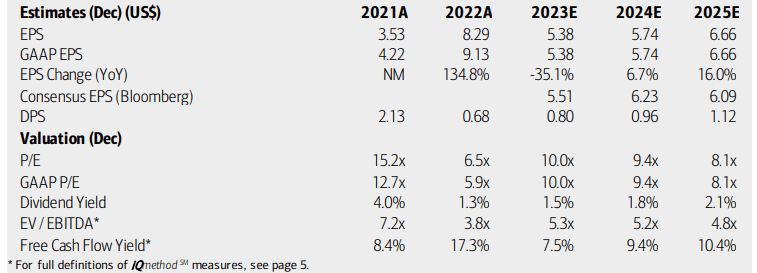

On valuation, analysts at BofA see earnings falling sharply this 12 months after oil’s growth within the first half of 2022. Per-share income are seen as normalizing close to $6 over the out years with strong progress. The Bloomberg consensus forecast is about on par with what BofA initiatives. Dividends, in the meantime, are anticipated to rise at a gradual tempo regardless of the variable characteristic of the payout. With first rate free cash flow per share, at present simply $1.65 on a trailing foundation (although it ought to rise over the approaching durations), and a low EV/EBITDA ratio, DVN has enticing earnings multiples.

Devon: Earnings, Valuation, Dividend, Free Money Circulation Forecasts

BofA World Analysis

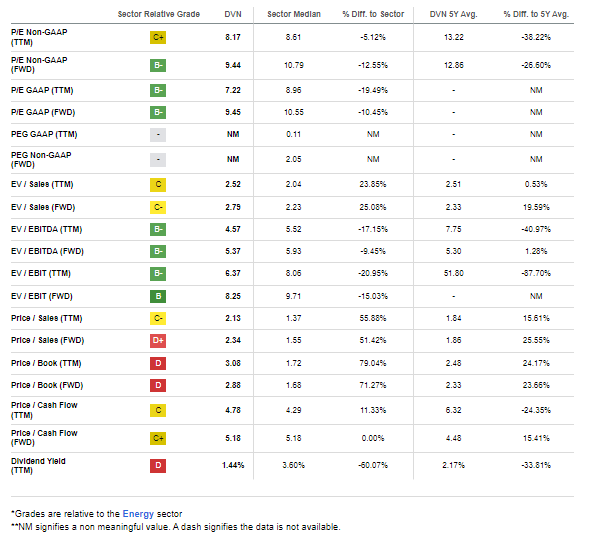

If we apply a sector median P/E ratio to the inventory and assume normalized next-12-month EPS of $6 then shares must be close to $65. Given increased oil costs at the moment and the truth that DVN has a 5-year common working earnings a number of nearer to 13, a barely increased valuation is warranted. Thus, if we use an 11 or 12 a number of, then shares must be within the $66 to $72 vary, making it a purchase.

DVN: Combined Valuation Image, Nonetheless Low-cost On a P/E Foundation

In search of Alpha

In comparison with its peers, DVN has much less favorable valuation grades, nevertheless it nonetheless seems low-cost in my opinion, notably contemplating its free money move observe document and strong profitability. As earnings normalize, the expansion score ought to enhance in my opinion. Nonetheless, earnings have been a bit shaky this 12 months versus expectations, so I wish to see higher execution on that entrance.

Competitor Evaluation

In search of Alpha

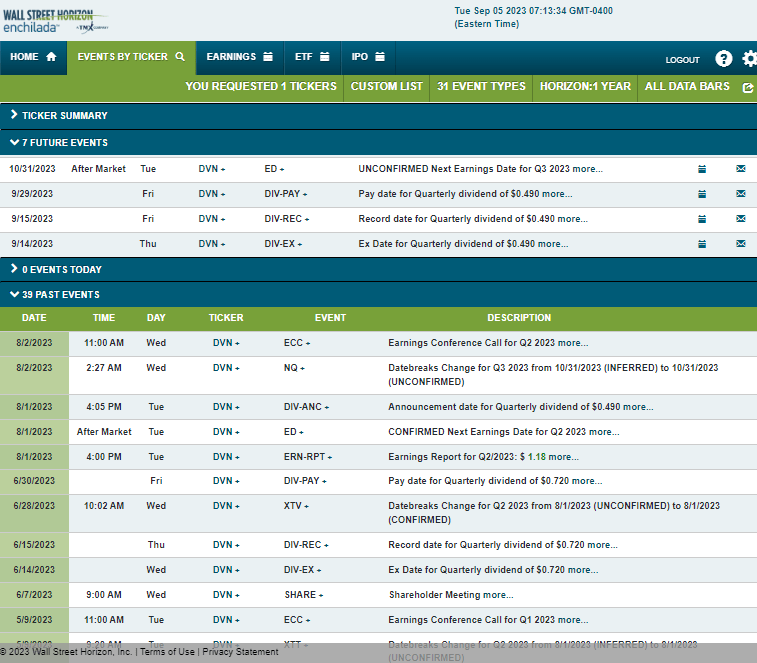

Wanting forward, company occasion information offered by Wall Road Horizon present an unconfirmed Q3 2023 earnings date of Tuesday, October 31 AMC. Earlier than that, DVN trades ex-div on September 14. No different volatility catalysts are seen on the calendar.

Company Occasion Threat Calendar

Wall Road Horizon

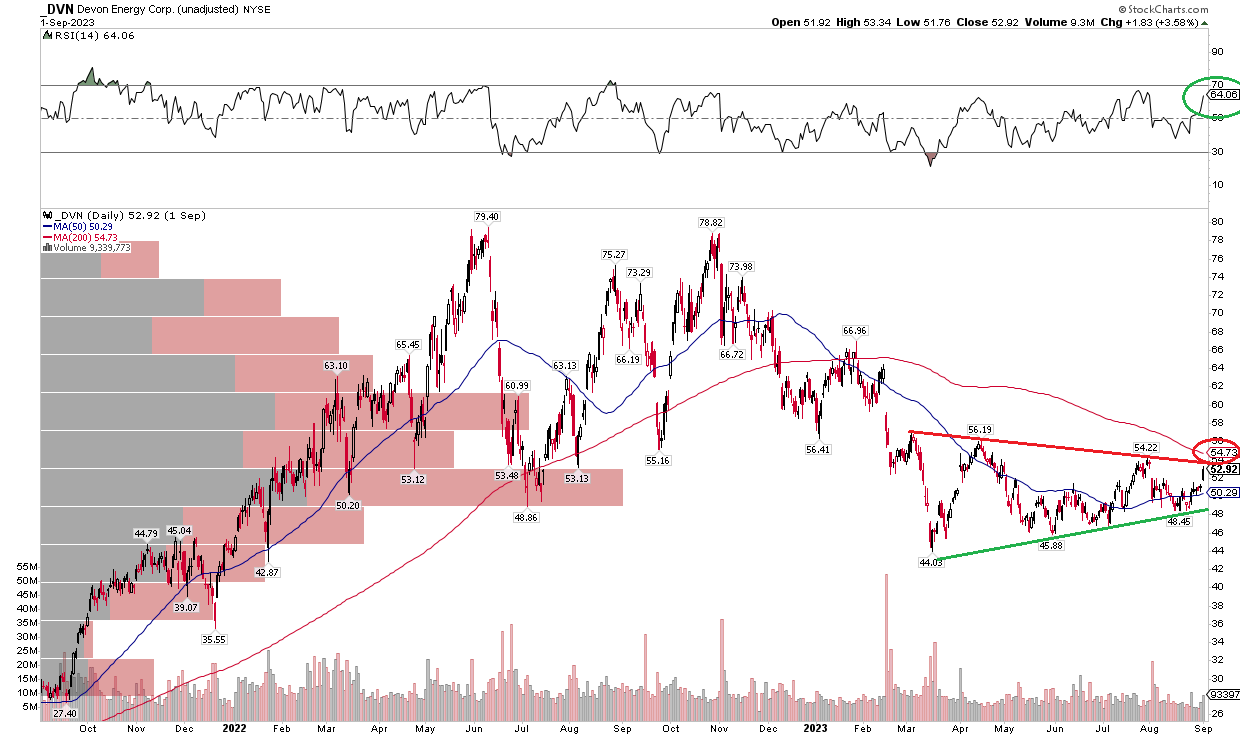

The Technical Take

Since I final reviewed Devon within the first half of the 12 months, there have been some attention-grabbing developments. Discover within the chart under {that a} symmetrical triangle has taken form. Now, usually this can be a continuation sample, indicating that DVN ought to finally break down decrease, however there are some causes for optimism.

First, the RSI momentum indicator on the high of the graph has usually been trending increased after notching a low again in March. Additionally, if the inventory can climb above the falling 200-day shifting common, at present slightly below $55, that may assist assist an upward transfer and it might even be a breakout from the triangle/coil sample. With a excessive quantity of quantity by worth beneath the closing worth final Friday, there must be some assist right down to about $49. Thus, we’ve got a worth level to watch.

Total, the chart is not at all a screaming purchase, however lengthy with a cease beneath the August low might work, and in the end, I’d nonetheless wish to see DVN rise above the $56 stage I famous back in May.

DVN: Regarding Symmetrical Triangle/Coil Sample

StockCharts.com

The Backside Line

I reiterate my purchase score on DVN inventory. I proceed to love the valuation, however the chart has not but come round as a lot as I would really like. Maybe the transfer up in oil that has been ongoing may give shares a lift and a breakout.

{kind=link}