Milko

Motive for the replace: Q2 replace and Acquisition of Acer Therapeutics

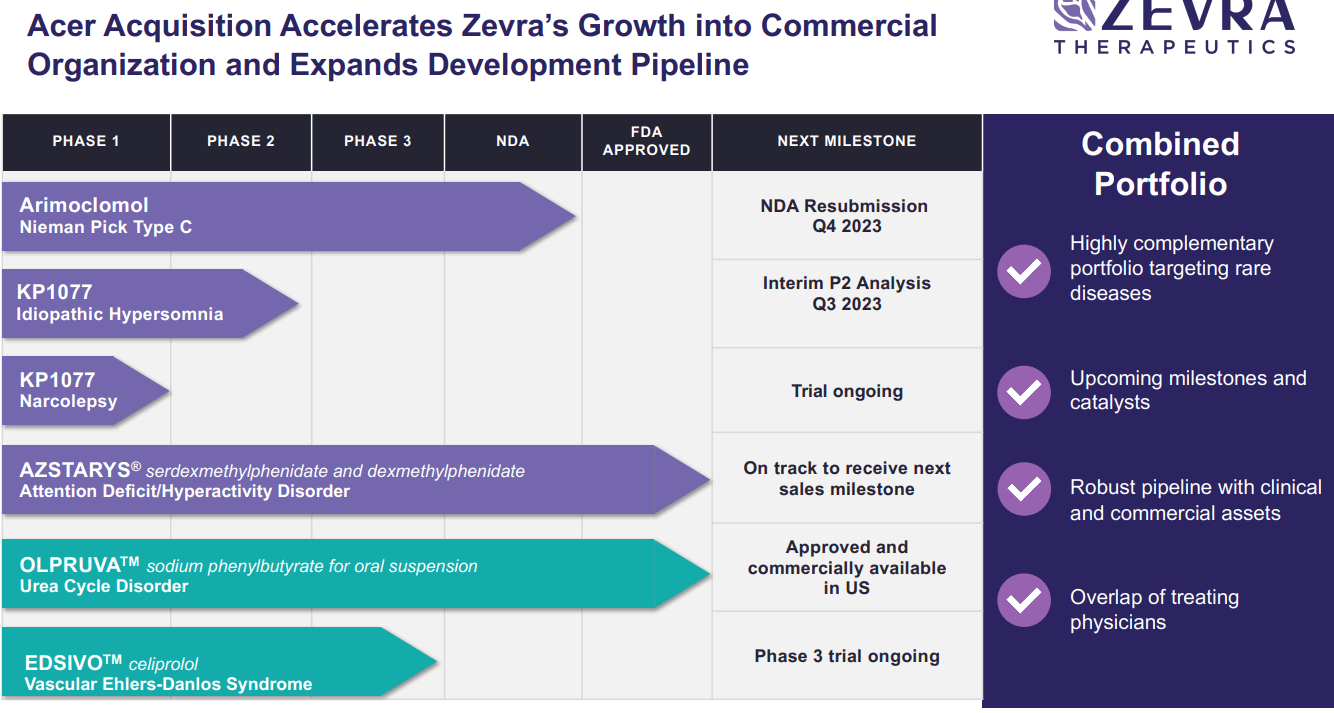

Zevra Therapeutics’ (NASDAQ:ZVRA) latest announcement of acquiring Acer Therapeutics for $91 million in inventory provides vital weight to their worth proposition. The deal construction – involving contingent worth rights, Acer’s debt buyout at a reduction, and a bridge mortgage extension – cements ZVRA’s dedication to the uncommon disease-focused technique. Acer’s introduction of the newly launched product Olpruva, for urea cycle problems (UCDs) aligns with ZVRA’s potential industrial efforts with arimoclomol, each concentrating on profitable uncommon illnesses. Moreover, though a secondary asset, Acer’s Edsivo, present process a Part 3 trial for vascular Ehlers-Danlos syndrome (vEDS) fills an unmet want given the absence of accepted merchandise for this uncommon illness.

Zevra (Firm presentation)

Central to Acer’s worth proposition is OLPRUVA™, an FDA-approved drugs designed for the continual administration of Urea Cycle Problems, uncommon genetic situations affecting ammonia removing from the bloodstream. OLPRUVA™ presents a novel formulation of phenylbutyrate that is extra palatable and handy than current remedies, with the potential to considerably enhance affected person compliance. We like the truth that its patent extends till 2036, assuring a long-term aggressive benefit. Moreover, Acer’s pipeline consists of EDSIVO™, a Part 3 program (that just lately began) concentrating on vascular Ehlers-Danlos syndrome, a extreme genetic dysfunction impacting blood vessels.

Of observe, Acer Therapeutics initiated affected person screenings for its Part III DiSCOVER scientific examine inspecting EDSIVO™ (celiprolol) in treating people with COL3A1-positive vascular Ehlers-Danlos Syndrome final year.

Upon reaching full enrollment, the DiSCOVER examine is projected to final round 3.5 years earlier than completion, considering statistical evaluations and the variety of fundamental occasions. An interim assessment is scheduled about two years after full enrollment. It is essential to notice that EDSIVO stays an experimental drug, with no approval from the U.S. FDA. There is not any assurance it’ll get regulatory nod or attain the industrial market within the U.S. for any use.

The Design of the Part III DiSCOVER Research:

The DiSCOVER trial is a potential, Part III, randomized, double-blind, placebo-controlled efficacy trial designed to judge EDSIVO (celiprolol) in sufferers with genetically confirmed COL3A1-positive vEDS utilizing a decentralized scientific trial design and an unbiased adjudication committee. The first goal of the trial is to find out whether or not EDSIVO (celiprolol) reduces the prevalence of vEDS-related scientific occasions requiring medical consideration, together with deadly and non-fatal cardiac or arterial occasions, uterine rupture, intestinal rupture, and/or unexplained sudden loss of life, relative to placebo as measured by time to occasion. Acer plans to enroll roughly 150 COL3A1-positive vEDS sufferers, all within the U.S., randomized 2:1 to obtain both EDSIVO (celiprolol) or placebo, respectively.

From an funding perspective, we imagine Zevra’s Acer acquisition presents a number of compelling factors:

- Complementary Portfolio: The addition of Acer’s merchandise aligns with and enhances Zevra’s uncommon illness focus.

- Income Potential: OLPRUVA™’s superior formulation addresses vital unmet wants in UCD remedies, providing an expansive market potential.

- Value Synergies: The mixed entities can notice vital financial savings throughout industrial operations.

- Operational Advantages: The merger boosts Zevra’s industrial and purposeful capabilities, positioning it higher for future product launches.

Anticipation Surrounding Arimoclomol NDA

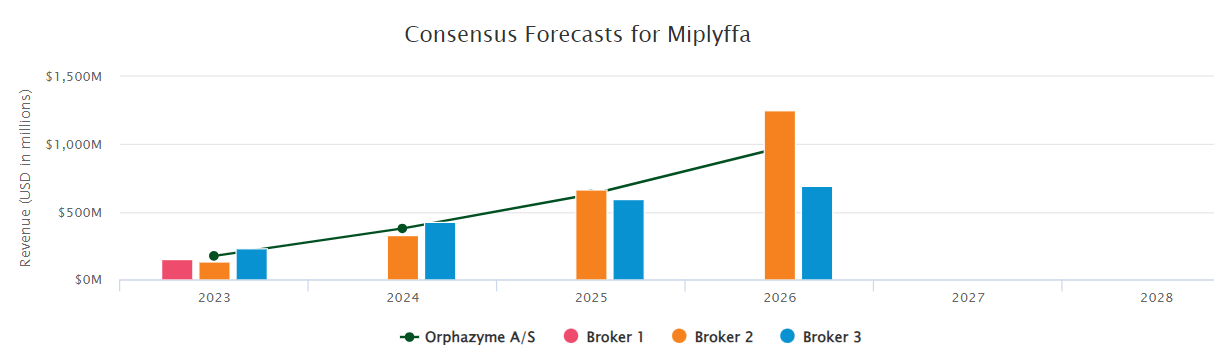

ZVRA’s arimoclomol for Niemann-Decide Sort C (NPC) illness is poised for a possible re-filing within the 4th quarter of 2023. Encouragingly, after a constructive assembly with the FDA, no extra scientific work was requested, signaling a smoother path to approval. This upcoming NDA resubmission catalyzes investor curiosity, given the excessive unmet want in NPC and the potential market awaiting the drug post-approval. In response to the pharma intelligence’s forecast, the height gross sales appear to be revolving round $500m-1Bn. Though, scientific and regulatory dangers stay, the optionality for a possible approval contemplating that the corporate is buying and selling at an fairness worth of $87m. For a extra detailed evaluation of the compound, please learn our earlier article.

BMT Consensus database (Arimoclomal gross sales projection)

Outperforming Expectations with Azstarys Royalties

The surge in Azstarys gross sales for ADHD therapy, surpassing $25 million, and Zevra earned $5M milestone funds and a royalty of $0.8M throughout Q2, which we imagine signifies the drug’s market traction. We spotlight that with the FDA declaring ADHD drug scarcity, we imagine the ramp of Azstarys to proceed, but, it seems the market is but to acknowledge the total potential of those escalating royalties in ZVRA’s valuation. Reaching additional milestones, as projected by the top of 2023, will solely amplify this income stream and underscore the corporate’s sturdy place.

Dangers

Nonetheless, it’s important to weigh the dangers in ZVRA’s journey. Arimoclomol’s refiling could encounter unexpected hurdles and even fail to get the nod from regulators. Challenges within the aggressive panorama for NPC and different illnesses can emerge. Potential administration shifts or board modifications may disrupt the corporate’s focus. And whereas the acquisition of Acer holds promise, any hiccups in its completion would pose a setback. Lastly, unpredictable issues of safety, trial delays or failures, and potential FDA disapprovals of pipeline merchandise may undermine the funding.

Conclusion: Sustaining a “Purchase” Stance on ZVRA

Wrapping up, ZVRA’s acquisition of Acer amplifies its strategic alignment in direction of uncommon illness remedies, additional diversifying and de-risking its portfolio. The anticipation surrounding the arimoclomol NDA and the encouraging trajectory of Azstary’s royalties, mixed with the substantial money runway into 2026, make ZVRA a compelling funding. Holding $87.4 million in cash on the finish of the second quarter of 2023, with expectations to increase its money runway into 2026 (contemplating annual money burn of ~$35m anticipated primarily based on earlier a number of quarter’s burn), the corporate is well-capitalized, and we’re not apprehensive about near-term dilution. Furthermore, the potential addition of income from arimoclomol post-approval and proceeds from potential monetization of the pediatric illness precedence assessment voucher boosts this outlook. Given these strengths and the mitigation of short-term dilution dangers, we’re inclined to keep up our purchase ranking on ZVRA, emphasizing its undervaluation within the present market.

{kind=link}