One argument for sustaining tight financial coverage is inflationary pressures — however the query is whether or not it’s from a constructive output hole or cost-push shocks (or expectations). One huge query is what’s the measurement of the output hole.

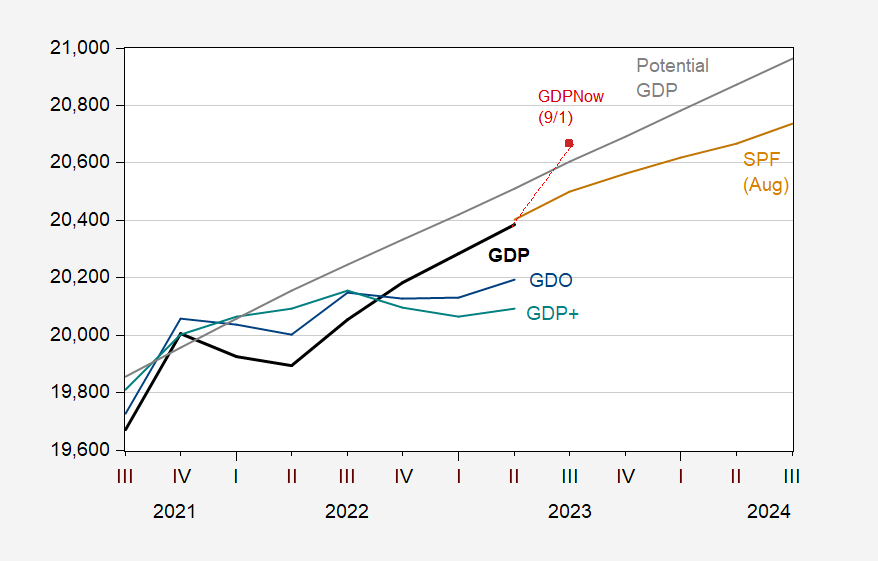

Determine 1: GDP (daring black), SPF median August forecast (tan), GDO (blue), GDP+ (teal), GDPNow of 9/1 (crimson sq.), and potential GDP (grey), all in bn.Ch.2012$ SAAR. Supply: BEA 2023Q2 2nd launch, Philadelphia Fed (GDP+), Philadelphia Fed (SPF), Atlanta Fed, CBO, and writer’s calculations.

Be aware that the output hole as of Q2 was -0.6%, utilizing GDP as reported. Utilizing GDPNow as of 9/1 (a blistering 5.6% q/q SAAR) will set the output hole at primarily zero in Q3. However, GDO — which is prone to be extra dependable than ultimate revised GDP — is at -1.6% in 2023Q2 (GDP+ is at -2.1%).

If the output hole is at the moment damaging, then the case for continued tightening is weak. That is much more so, even taking reported GDP as correct, if the SPF median is right and the output hole might be more and more damaging over time.

These calculations depend upon estimates of potential GDP. On this level, there’s some disagreement. For example, as of 2022, CBO’s output hole is 1.2 share factors of potential GDP lower than OECD’s (June 2023 Financial Outlook). The estimate for 2023 is 1.1 ppts decrease. Relying upon the OECD estimate implies a greater case for tight financial coverage.

For comparability’s sake, 2023Q2 CBO hole is -0.6 ppts, HP deviation is 0.3 ppts, and Hamilton filter is 0.6 ppts.

One argument for sustaining tight financial coverage is inflationary pressures — however the query is whether or not it’s from a constructive output hole or cost-push shocks (or expectations). One huge query is what’s the measurement of the output hole.

Determine 1: GDP (daring black), SPF median August forecast (tan), GDO (blue), GDP+ (teal), GDPNow of 9/1 (crimson sq.), and potential GDP (grey), all in bn.Ch.2012$ SAAR. Supply: BEA 2023Q2 2nd launch, Philadelphia Fed (GDP+), Philadelphia Fed (SPF), Atlanta Fed, CBO, and writer’s calculations.

Be aware that the output hole as of Q2 was -0.6%, utilizing GDP as reported. Utilizing GDPNow as of 9/1 (a blistering 5.6% q/q SAAR) will set the output hole at primarily zero in Q3. However, GDO — which is prone to be extra dependable than ultimate revised GDP — is at -1.6% in 2023Q2 (GDP+ is at -2.1%).

If the output hole is at the moment damaging, then the case for continued tightening is weak. That is much more so, even taking reported GDP as correct, if the SPF median is right and the output hole might be more and more damaging over time.

These calculations depend upon estimates of potential GDP. On this level, there’s some disagreement. For example, as of 2022, CBO’s output hole is 1.2 share factors of potential GDP lower than OECD’s (June 2023 Financial Outlook). The estimate for 2023 is 1.1 ppts decrease. Relying upon the OECD estimate implies a greater case for tight financial coverage.

For comparability’s sake, 2023Q2 CBO hole is -0.6 ppts, HP deviation is 0.3 ppts, and Hamilton filter is 0.6 ppts.

{kind=link}