Does an error correction mannequin of the Divisia M4 amount idea or a previous model expectations and provide shock augmented Phillips curve match the put up 2019 interval higher (utilizing 1998-2019 information)? Reply: The Phillips curve works higher.

To be honest to the Amount Concept, I take a look at for cointegration between PCE deflator and M4 divisia divided by GDP (therefore imposing a unit coefficient on GDP). The Johansen most chance method often detects cointegration. I then estimate an error correction mannequin:

Δpt = 0.114 – 0.016(p-m+y)t-1 + 0.224Δpt-1 – 0.001Δmt-1 + 0.222Δyt-1

Adj-R2 = 0.13, SER = 0.0036, DW = 1.90, NObs = 88

and Phillips curve:

Δpt = 0.002 + 0.020(y-ypot)t-1 + 0.077πet-1 + 0.0008gscpit-1 + 0.0009gscpit2 + 0.019Δpoilt + 0.006Δpoilt-1

Adj-R2 = 0.69, SER = 0.0021, DW = 1.98, NObs = 88

The place p is the log PCE deflator, Δp is q/q inflation, m is log M4M divisia, y is log actual GDP, ypot is potential GDP (CBO), πe is Michigan anticipated inflation, Δpoil is q/q progress price of oil costs, and gscpi is the NY Fed International Suppy Chain Strain Index.

Observe that the amount idea/divisia mannequin estimates make some sense. The statistically vital and unfavorable coefficient on the error correction time period signifies that the value degree reverts to revive equilibrium in the long term, at about 1.6% per quarter. (Apparently, GDP and cash each revert at a sooner tempo than costs.)

The Phillips curve match is a lot better, with an adj-R2 of 0.69. The output hole enters with a big and constructive coefficient. Anticipated inflation additionally enters, together with oil costs.

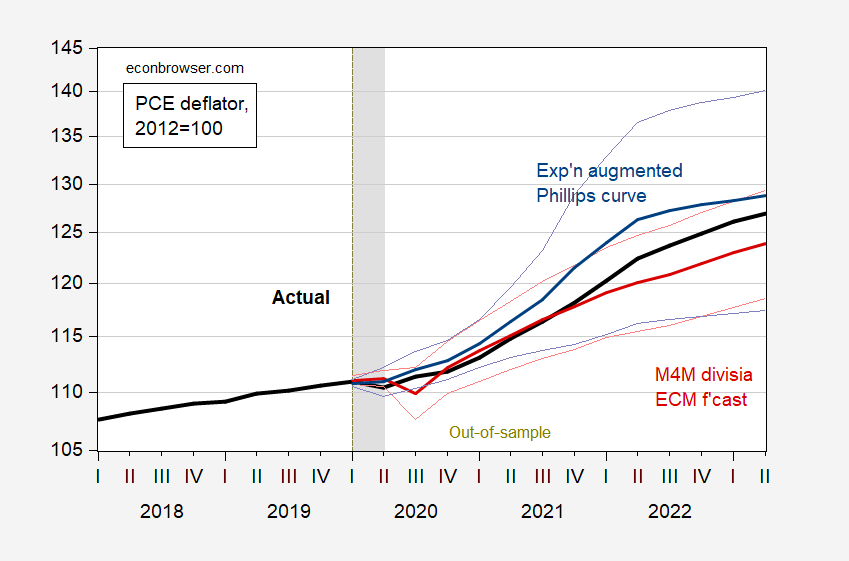

How do the 2 empirical fashions evaluate? The out-of-sample forecasts (strictly talking, two ex put up historic simulations, for the reason that proper hand aspect variable are taken as given).

Determine 1: PCE deflator (daring black), amount idea/divisia mannequin (pink), plus/minus one std error band (pink traces), expectations and cost-push shock augmented Phillips curve mannequin (blue), plus/minus one std error band (mild blue traces), all 2012=100. NBER outlined peak-to-trough recession dates shaded grey. Supply: writer’s calculations.

In different phrases, the Phillips curve truly predicts the value degree effectively, opposite to assertions that inflation was not effectively predicted. Truly, if one had identified that oil costs had been going to rise particularly in early 2022, and provide chain pressures had been to be elevated in 2021, then the persistence of inflation would have been unsurprising.

Does an error correction mannequin of the Divisia M4 amount idea or a previous model expectations and provide shock augmented Phillips curve match the put up 2019 interval higher (utilizing 1998-2019 information)? Reply: The Phillips curve works higher.

To be honest to the Amount Concept, I take a look at for cointegration between PCE deflator and M4 divisia divided by GDP (therefore imposing a unit coefficient on GDP). The Johansen most chance method often detects cointegration. I then estimate an error correction mannequin:

Δpt = 0.114 – 0.016(p-m+y)t-1 + 0.224Δpt-1 – 0.001Δmt-1 + 0.222Δyt-1

Adj-R2 = 0.13, SER = 0.0036, DW = 1.90, NObs = 88

and Phillips curve:

Δpt = 0.002 + 0.020(y-ypot)t-1 + 0.077πet-1 + 0.0008gscpit-1 + 0.0009gscpit2 + 0.019Δpoilt + 0.006Δpoilt-1

Adj-R2 = 0.69, SER = 0.0021, DW = 1.98, NObs = 88

The place p is the log PCE deflator, Δp is q/q inflation, m is log M4M divisia, y is log actual GDP, ypot is potential GDP (CBO), πe is Michigan anticipated inflation, Δpoil is q/q progress price of oil costs, and gscpi is the NY Fed International Suppy Chain Strain Index.

Observe that the amount idea/divisia mannequin estimates make some sense. The statistically vital and unfavorable coefficient on the error correction time period signifies that the value degree reverts to revive equilibrium in the long term, at about 1.6% per quarter. (Apparently, GDP and cash each revert at a sooner tempo than costs.)

The Phillips curve match is a lot better, with an adj-R2 of 0.69. The output hole enters with a big and constructive coefficient. Anticipated inflation additionally enters, together with oil costs.

How do the 2 empirical fashions evaluate? The out-of-sample forecasts (strictly talking, two ex put up historic simulations, for the reason that proper hand aspect variable are taken as given).

Determine 1: PCE deflator (daring black), amount idea/divisia mannequin (pink), plus/minus one std error band (pink traces), expectations and cost-push shock augmented Phillips curve mannequin (blue), plus/minus one std error band (mild blue traces), all 2012=100. NBER outlined peak-to-trough recession dates shaded grey. Supply: writer’s calculations.

In different phrases, the Phillips curve truly predicts the value degree effectively, opposite to assertions that inflation was not effectively predicted. Truly, if one had identified that oil costs had been going to rise particularly in early 2022, and provide chain pressures had been to be elevated in 2021, then the persistence of inflation would have been unsurprising.

{kind=link}