One of many puzzles of present occasions is why total assessments of the financial system haven’t risen in accord with precise developments (say, as summarized by the Distress Index), and relatedly why these positive factors haven’t redounded to the incumbent president’s approval rankings (dialogue here). I don’t have solutions, however I’ve some observations.

Financial Circumstances and (Measured) Financial Sentiment

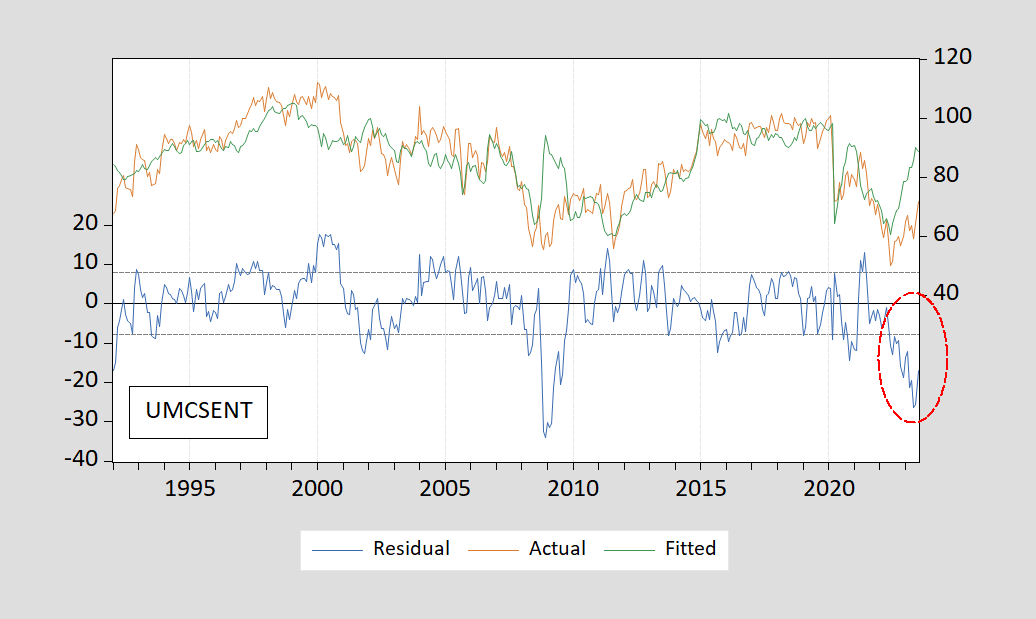

First, how a lot as the present studying of the Michigan Index of Financial Sentiment (FRED collection UMCSENT) deviated from what is anticipated over the previous 30 years? Pictured in Determine 1 is the precise UMCSENT collection (pink), the fitted collection (inexperienced), and residuals (blue).

Determine 1: Precise, fitted, and residual for UMCSENT regression.

The regression (utilized in my previous post on this topic) is (gasoline value is CPI deflated):

UMCSENT = 44.26 – 4.06MISERY – 16.4pgasoline

Adj-R2 = 0.61, SER = 8.30, DW = 0.28, Nobs = 379, pattern 1992M01-2023.07. Daring Italics denotes significance at 10% msl, utilizing HAC sturdy customary errors.

(I’ve used Bloomberg consensus for July unemployment fee, and Cleveland Fed 8/1 nowcast for July CPI.)

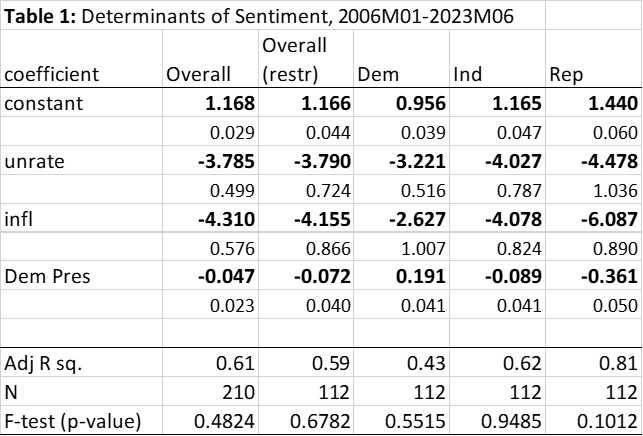

Carola Binder has a wonderful dialogue of partisan results in sentiment, present and expectations. Right here, I deal with the differential impacts of Distress Index elements (the unemployment fee and the y/y CPI inflation fee) on the disaggregated sentiment indexes. First, right here’s an image of the totally different collection.

Determine 2: College of Michigan Index of Financial Sentiment (daring black), for Democrats (blue), for Independents (chartreuse), for Republicans (pink). NBER outlined peak-to-trough recession dates shaded grey. Supply: College of Michigan by way of FRED, University of Michigan, NBER.

Notice that the Republican view is far more optimistic than Republicans throughout the Trump administration, however switched to far more adverse throughout the Biden. It is a reflection of the well-known tendency for sentiment to be a lot increased than in any other case when the president is a member of the respondent’s occasion. It could be good to see if this impact is stronger in newer occasions than earlier many years, however a reasonably steady time collection just isn’t obtainable earlier than 2006, so it’s exhausting to reply this query.

As of July, Republicans have a 51 studying, whereas Democrats have a 92 studying.

How totally different to Democrats, Independents and Republicans view financial circumstances primarily based on realizations of unemployment and inflation? I examine this query by regressing varied UMCSENT measures on these variables in addition to a dummy variable for a Democratic president.

UMCSENTit = α0 + α1Ut + α2πt + α3DEMPRESt

The place i = total, Democrat, Impartial, Republican, 2006M01-2023M07. UMCSENT is split by 100, Ut and πt are in decimal kind. Desk 1 presents the outcomes.

Notes: Daring face denotes significance at 10% msl utilizing HAC sturdy customary errors. F-test (p-value) is p-value for restriction that coefficients on unemployment and inflation are the identical.

Column 1 reveals the outcomes for the UMCSENT (total) drawn from FRED. The unemployment fee and inflation fee present up with about the identical sized coefficient. Democratic presidential administrations present up with a adverse coefficient: a Democratic president is related to a 0.05 discount in UMCSENT (imply of normalized index is 0.86). If one restricts the pattern to the identical interval for which we’ve the disaggregated outcomes (column 2), then outcomes are largely the identical; therefore the interval for which we’ve the disaggregate knowledge doesn’t look like anomalous.

Democrats seem to put barely decrease weight on inflation than on unemployment — however not a statistically considerably decrease. In distinction, Republicans place considerably increased weight on inflation than on unemployment (the F-test practically rejects the null of equal coefficients).

The coefficient on the dummy variable confirms the discovering that views on the financial state are extra optimistic when the presidency is held by somebody of the identical political occasion/affiliation: the coefficient on DEMPRES is optimistic for Dem (+0.191), and adverse for Rep (-0.361), and barely much less adverse for Ind (suggesting that Ind are extra like Rep than Dem). Usually, the standardized coefficients (“beta” coefficients) point out largest impacts are related to the dummy variable.

There may be an asymmetry within the influence of presidential occasion affiliation. Throughout this era (2006-2013), Republicans have an outsized influence of presidential affiliation — 0.361 vs. 0.191 (in absolute worth). Ceteris paribus, they actually view circumstances negatively when a Democrat holds the presidency.

Apparently, whereas each Ind and Rep sentiment is determined by the unemployment and inflation charges (Adj R2 round 0.5), Dem sentiment is essentially unexplained (Adj R2 round 0.04). The y/y progress fee of the actual S&P500 appears to have a a lot bigger influence (as measured by the “beta” coefficient) for Dem than for Rep or Ind.

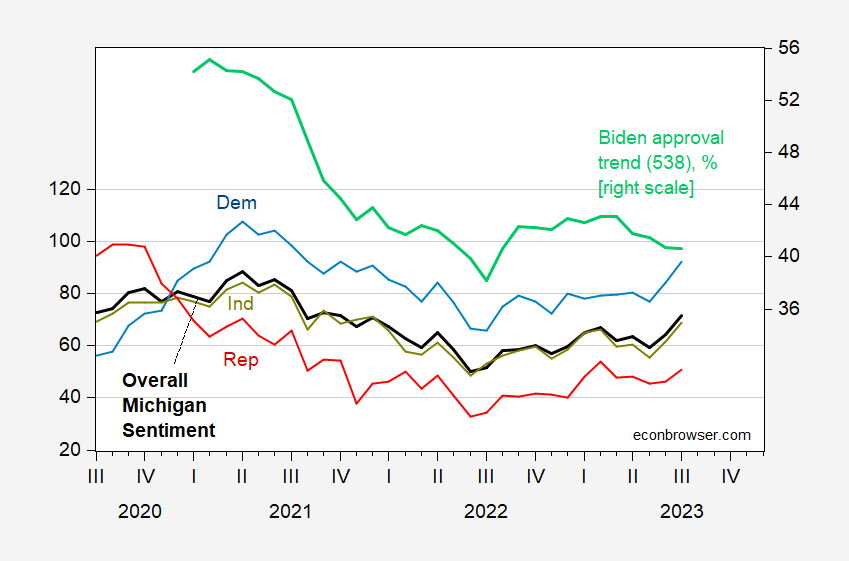

(Measured) Financial Sentiment and Biden Approval

A commonplace chorus is that Biden just isn’t getting credit score for the robust efficiency of the financial system. This level is verified by inspecting Biden’s approval fee development (from FiveThirtyEight) and the sentiment indexes.

Determine 3: College of Michigan Index of Financial Sentiment (daring black, left scale), for Democrats (blue, left scale), for Independents (chartreuse, left scale), for Republicans (pink, left scale), Biden Approval Pattern, % (gentle inexperienced, proper scale). Supply: College of Michigan by way of FRED, University of Michigan, FiveThirtyEight.

Utilizing the connection between UMCSENT and Biden approval over the 2021M11-2023M07 interval, the July Biden approval fee needs to be 43.1, versus the 538 development worth of 40.5.

One of many puzzles of present occasions is why total assessments of the financial system haven’t risen in accord with precise developments (say, as summarized by the Distress Index), and relatedly why these positive factors haven’t redounded to the incumbent president’s approval rankings (dialogue here). I don’t have solutions, however I’ve some observations.

Financial Circumstances and (Measured) Financial Sentiment

First, how a lot as the present studying of the Michigan Index of Financial Sentiment (FRED collection UMCSENT) deviated from what is anticipated over the previous 30 years? Pictured in Determine 1 is the precise UMCSENT collection (pink), the fitted collection (inexperienced), and residuals (blue).

Determine 1: Precise, fitted, and residual for UMCSENT regression.

The regression (utilized in my previous post on this topic) is (gasoline value is CPI deflated):

UMCSENT = 44.26 – 4.06MISERY – 16.4pgasoline

Adj-R2 = 0.61, SER = 8.30, DW = 0.28, Nobs = 379, pattern 1992M01-2023.07. Daring Italics denotes significance at 10% msl, utilizing HAC sturdy customary errors.

(I’ve used Bloomberg consensus for July unemployment fee, and Cleveland Fed 8/1 nowcast for July CPI.)

Carola Binder has a wonderful dialogue of partisan results in sentiment, present and expectations. Right here, I deal with the differential impacts of Distress Index elements (the unemployment fee and the y/y CPI inflation fee) on the disaggregated sentiment indexes. First, right here’s an image of the totally different collection.

Determine 2: College of Michigan Index of Financial Sentiment (daring black), for Democrats (blue), for Independents (chartreuse), for Republicans (pink). NBER outlined peak-to-trough recession dates shaded grey. Supply: College of Michigan by way of FRED, University of Michigan, NBER.

Notice that the Republican view is far more optimistic than Republicans throughout the Trump administration, however switched to far more adverse throughout the Biden. It is a reflection of the well-known tendency for sentiment to be a lot increased than in any other case when the president is a member of the respondent’s occasion. It could be good to see if this impact is stronger in newer occasions than earlier many years, however a reasonably steady time collection just isn’t obtainable earlier than 2006, so it’s exhausting to reply this query.

As of July, Republicans have a 51 studying, whereas Democrats have a 92 studying.

How totally different to Democrats, Independents and Republicans view financial circumstances primarily based on realizations of unemployment and inflation? I examine this query by regressing varied UMCSENT measures on these variables in addition to a dummy variable for a Democratic president.

UMCSENTit = α0 + α1Ut + α2πt + α3DEMPRESt

The place i = total, Democrat, Impartial, Republican, 2006M01-2023M07. UMCSENT is split by 100, Ut and πt are in decimal kind. Desk 1 presents the outcomes.

Notes: Daring face denotes significance at 10% msl utilizing HAC sturdy customary errors. F-test (p-value) is p-value for restriction that coefficients on unemployment and inflation are the identical.

Column 1 reveals the outcomes for the UMCSENT (total) drawn from FRED. The unemployment fee and inflation fee present up with about the identical sized coefficient. Democratic presidential administrations present up with a adverse coefficient: a Democratic president is related to a 0.05 discount in UMCSENT (imply of normalized index is 0.86). If one restricts the pattern to the identical interval for which we’ve the disaggregated outcomes (column 2), then outcomes are largely the identical; therefore the interval for which we’ve the disaggregate knowledge doesn’t look like anomalous.

Democrats seem to put barely decrease weight on inflation than on unemployment — however not a statistically considerably decrease. In distinction, Republicans place considerably increased weight on inflation than on unemployment (the F-test practically rejects the null of equal coefficients).

The coefficient on the dummy variable confirms the discovering that views on the financial state are extra optimistic when the presidency is held by somebody of the identical political occasion/affiliation: the coefficient on DEMPRES is optimistic for Dem (+0.191), and adverse for Rep (-0.361), and barely much less adverse for Ind (suggesting that Ind are extra like Rep than Dem). Usually, the standardized coefficients (“beta” coefficients) point out largest impacts are related to the dummy variable.

There may be an asymmetry within the influence of presidential occasion affiliation. Throughout this era (2006-2013), Republicans have an outsized influence of presidential affiliation — 0.361 vs. 0.191 (in absolute worth). Ceteris paribus, they actually view circumstances negatively when a Democrat holds the presidency.

Apparently, whereas each Ind and Rep sentiment is determined by the unemployment and inflation charges (Adj R2 round 0.5), Dem sentiment is essentially unexplained (Adj R2 round 0.04). The y/y progress fee of the actual S&P500 appears to have a a lot bigger influence (as measured by the “beta” coefficient) for Dem than for Rep or Ind.

(Measured) Financial Sentiment and Biden Approval

A commonplace chorus is that Biden just isn’t getting credit score for the robust efficiency of the financial system. This level is verified by inspecting Biden’s approval fee development (from FiveThirtyEight) and the sentiment indexes.

Determine 3: College of Michigan Index of Financial Sentiment (daring black, left scale), for Democrats (blue, left scale), for Independents (chartreuse, left scale), for Republicans (pink, left scale), Biden Approval Pattern, % (gentle inexperienced, proper scale). Supply: College of Michigan by way of FRED, University of Michigan, FiveThirtyEight.

Utilizing the connection between UMCSENT and Biden approval over the 2021M11-2023M07 interval, the July Biden approval fee needs to be 43.1, versus the 538 development worth of 40.5.

{kind=link}