sbelov

Abstract

Following my protection of Lumentum Holdings (NASDAQ:LITE), I really useful a maintain score attributable to my expectation that gross margins can be negatively impacted by decrease gross margins within the coming quarters. This publish is to offer an replace on my ideas on the enterprise and inventory. I reiterate my maintain score, as I do not see any enhancements within the stock scenario to date. In reality, the feedback made by administration led me to imagine the scenario was worse than I had initially anticipated.

Funding thesis

LITE’s income for 4Q23 was $371 million, which was barely greater than the $350 million to $380 million steerage vary’s midpoint. In the meantime, gross margins got here in at 36.7%, working margins at 9.1%, and EPS at 0.59. Whereas income did exceed the midpoint of projections, I don’t imagine the scenario has improved (which is why I remained impartial on the inventory). In reality, the outcomes of 4Q23 satisfied me that the effort and time required to digest buyer stock can be larger than I had anticipated. The service suppliers, who’re LITE’s prospects, have surplus inventory, which I didn’t account for in my authentic expectation. Which suggests there are two levels to clear earlier than LITE will profit from the inventory normalization course of. The present scenario is actually within the arms of LITE, the place they merely should chunk the bullet and sit by this course of. As I’ve stated earlier than, administration’s monitor document in estimating stock ranges is poor, so I would not be shocked if issues are worse than they appear. This solely serves to intensify issues concerning the future trajectory of each income and, extra importantly, gross margin.

Administration has additionally traditionally been inaccurate as they appear to not be capable of appropriately predict how lengthy it should take for purchasers to appropriate their extra stock ranges. As an example, in 1Q23, administration’s forecast that the Datacom slowdown brought on by extra stock amongst ICP prospects would proceed for the remainder of FY23 was incorrect. The identical factor occurred in China two years in the past with an EML laser chip oversupply that lasted many extra quarters than anticipated. Subsequently, I lack confidence in administration’s assurance that this stock drawback will likely be resolved by CY23. – Jay Capital

Nevertheless, LITE’s Datacom enterprise seems to be a brilliant spot, pushed by rising demand related to AI-based purposes amongst cloud supplier prospects. LITE’s present involvement within the AI trade stems from the sale of EMLs to transceiver producers to be used in making 800 gigabit transceivers. From what I can inform, LITE’s presence and development potential are simply getting began, as administration has solely simply begun re-introducing further assets and capability to serve this market. This momentum ought to start to materialize within the type of improved monetary outcomes throughout the subsequent few quarters. Trying forward, LITE can be engaged on a VCSEL-based resolution for short-range purposes in AI-based architectures, and it must be prepared in 2CH24. As short-range, multi-mode optical hyperlinks regularly change copper, VCSELs are anticipated to expertise vital development over the subsequent few years. As such, I feel this provides nice publicity to LITE within the AI house. That stated, I do not suppose this development expectation is ample to beat the uncertainty with reference to the stock overstock scenario.

Valuation

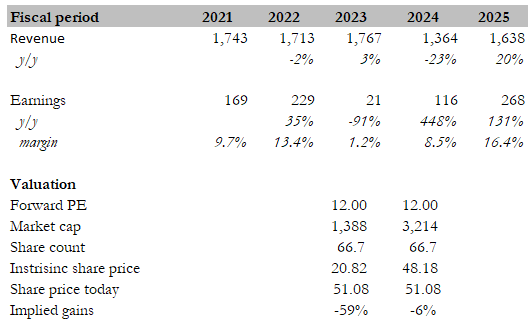

Personal calculation

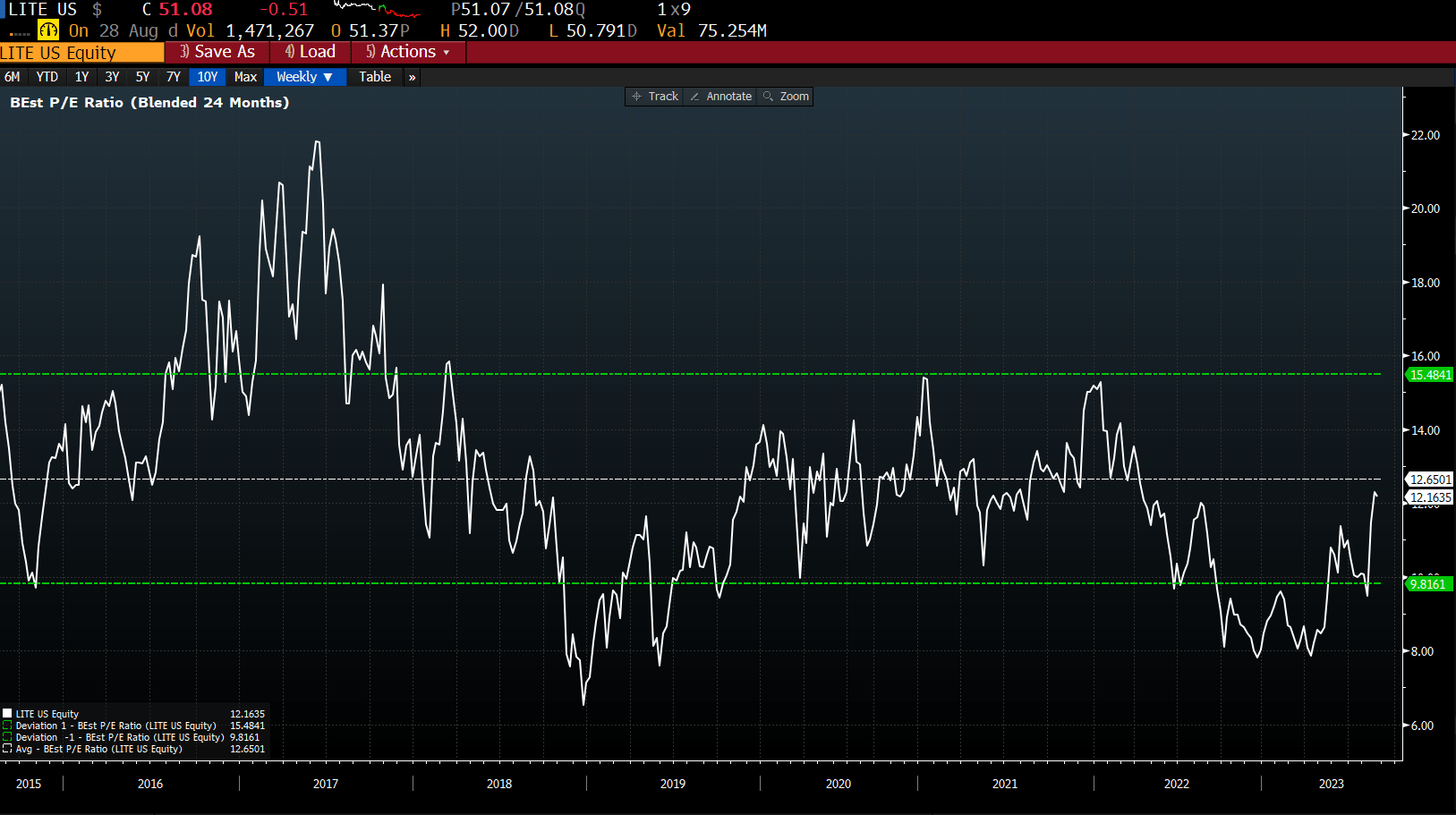

Beforehand, I confirmed the potential upside if valuation goes again to 12.7x 2Y ahead earnings, when it was buying and selling at 10x 2Y ahead earnings. With the a number of buying and selling at 12x immediately, I not imagine that is the case. Utilizing consensus estimates as a information for anticipated earnings development, I feel it’s obvious that any potential upside will come from expectations of FY25 earnings efficiency. The consensus is anticipating income to say no by 23% in FY24, which I see as a good assumption contemplating the stock scenario. The issue is, when will this finish? The present expectation is for a FY25 restoration, however word that no one actually is aware of how unhealthy the scenario is-even administration acquired it mistaken. I imagine this uncertainty is one thing that can preserve the inventory value vary sure till at the least 2FH24, after we may have higher info to evaluate the scenario. One other destructive level is that even when I assume consensus is correct, the inventory appears to be pretty valued at 12x 2Y ahead PE.

Bloomberg

Conclusion

In conclusion, LITE stock overstock problem persists, and the scenario could be extra dire than what I initially anticipated. My suggestion to carry stays unchanged attributable to this ongoing concern. Whereas LITE’s Datacom enterprise reveals promise, the uncertainty surrounding stock overstock overshadows potential development. The valuation additionally seems to have adjusted to the present circumstances, and any substantial upside hinges on expectations for FY25 efficiency. Given the unpredictability of the stock concern, the inventory would possibly stay range-bound till higher readability emerges, probably round 2H24.

{kind=link}