Brandon Bell/Getty Photographs Information

Again in May, I wrote that Chipotle Mexican Grill (NYSE:CMG) was an ideal firm however that the inventory’s valuation appeared stretched given the present unsure outlook and that the market was appearing as if the corporate was recession proof. With the inventory down following its Q2 earnings after a same-store gross sales miss, let’s take a better have a look at its most up-to-date earnings.

Q2 Outcomes

For Q2, CMG noticed its income bounce 13.6% to $2.4 billion. That barely missed analyst estimates by $20 million.

Comparable restaurant gross sales rose 7.4%. Nonetheless, that was wanting the 7.7% improve that analysts had been anticipating. Transactions grew 4%, with menu costs up about 5.5% and blend about -2.5%.

Adjusted EPS got here in at $12.65, simply surpassing analyst estimates of $12.28.

Discussing among the drivers of the quarter on its Q2 earnings call, CFO John Hartung stated:

“And talking of remarkable meals, our menu innovation has been excellent this yr. Rooster Al Pastor has confirmed to be a preferred LTO with 1 in 5 transactions, together with the brand new protein. It’s boosting transactions with a powerful repeat and is attracting new clients to Chipotle and in addition delivered the best constructive social sentiment of any new menu introduction and importantly, was easy for our groups to execute, which resulted in a win throughout. As Rooster Al Pastor wraps up in late August, now we have a deliberate new menu merchandise for later within the quarter. Our rewards program is one other approach we purpose to drive frequency inside our present buyer base as our reward members come extra typically and spend greater than nonrewards members. We launched Freepotle earlier this yr, which was designed to ship a powerful worth proposition and appeal to new members with 10 free rewards dropped into our members’ accounts all year long. Freepotle has been profitable in driving enrollments within the first half of the yr as we surpassed 35 million reward members. With every strategic Freepotle drop, we’re studying extra about our clients’ behaviors and using these learnings to personalize future gives. We are going to proceed to search for artistic methods to drive enrollment and enhance engagement in our rewards program. In conventional media, we stay high of thoughts at sporting occasions as we leverage the basketball playoffs as a high-profile alternative to highlight the Chipotle model and thru our NHL partnership, our Chipotle brand was featured on the ice through the Stanley Cup playoffs.”

Restaurant stage margins had been 25.6%, a 230 foundation level year-over-year improve and a 190bps sequential improve.

Price of gross sales for the quarter was 29.4%, a lower of -100 foundation in comparison with the earlier yr. Menu worth will increase and decrease avocado costs offset increased commodity prices elsewhere. Labor prices as a proportion of gross sales had been 24.3% a -50bps lower versus a yr in the past, as gross sales leverage outweighed wage inflation.

The corporate opened 47 places within the quarter, of which 40 had a Chipotlane.

CMG purchased again $88 million in inventory at a mean worth of $1,937 within the quarter.

Total, the quarter itself was fairly good, however given the place the inventory’s valuation was getting into the report, simply hitting numbers wasn’t going to be ok. A lot of the CMG’s same-store positive factors have come from pricing in current quarters, though the truth that visitors continues to be up solidly within the face of some fairly massive worth hikes does proceed to talk to the energy of the model.

Outlook

For Q3, CMG forecast comparable-restaurant gross sales to develop within the low- to mid-single digit vary. It would see 500bps factors of pricing roll off in August. It’s taking a look at combine a having a couple of -200bps unfavorable affect. Transactions anticipated to be up 3.0-3.5%. For the total yr, the corporate is in search of mid to excessive single digit comps.

The corporate expects margins to say no in Q3 with COGs of round 30% of gross sales, as a result of increased beef and avocado costs. It famous that it’s shifting the place it will get avocados, and that the majority will come from Peru in Q3 to keep away from the worth volatility within the Mexican market. Labor prices are additionally anticipated to extend to about 25% in Q3 of gross sales as a result of wage inflation and seasonally decrease gross sales.

At present, the corporate has not stated if it’ll take any worth will increase, though it has sometimes taken one in This autumn.

The corporate stated that its customers stay robust each for higher-income and lower-income patrons. It stated it exited the quarter with robust visitors and transaction developments and that lower-income customers have really been seeing an enchancment.

The corporate stated it stays on monitor to open 255-285 new eating places this yr, which incorporates 10-15 relocations so as to add Chipotlanes. Roughly 80% of the brand new places may have a Chipotlane. Over 600 places presently have Chipotlanes

With CMG set to lap an enormous worth improve final August, visitors will come into to focus within the 2nd half. Notably, the corporate’s Pastor Al Rooster will wrap up as a restricted time providing on the finish August, as properly. With the corporate saying 20% of transactions included the favored LTO as a protein, this might probably be a headwind as properly. On the similar time, meals and labor prices are nonetheless on the rise.

Valuation

CMG inventory trades at 29.3x the 2023 EBITDA consensus of $1.86 billion and 24.8x the 2024 EBITDA consensus of $2.2 billion.

From an EBITDAR perspective, it trades at ~19.5x 2023 numbers and ~17x 2024 numbers.

From a P/E perspective, it trades at simply over 43x the 2023 EPS estimate of $44.46. In the meantime, it is valued at about 36x the 2024 EPS estimate of $52.58.

It is projected to develop income 13.7% this yr, and have low to mid-teens income development over the following a number of years.

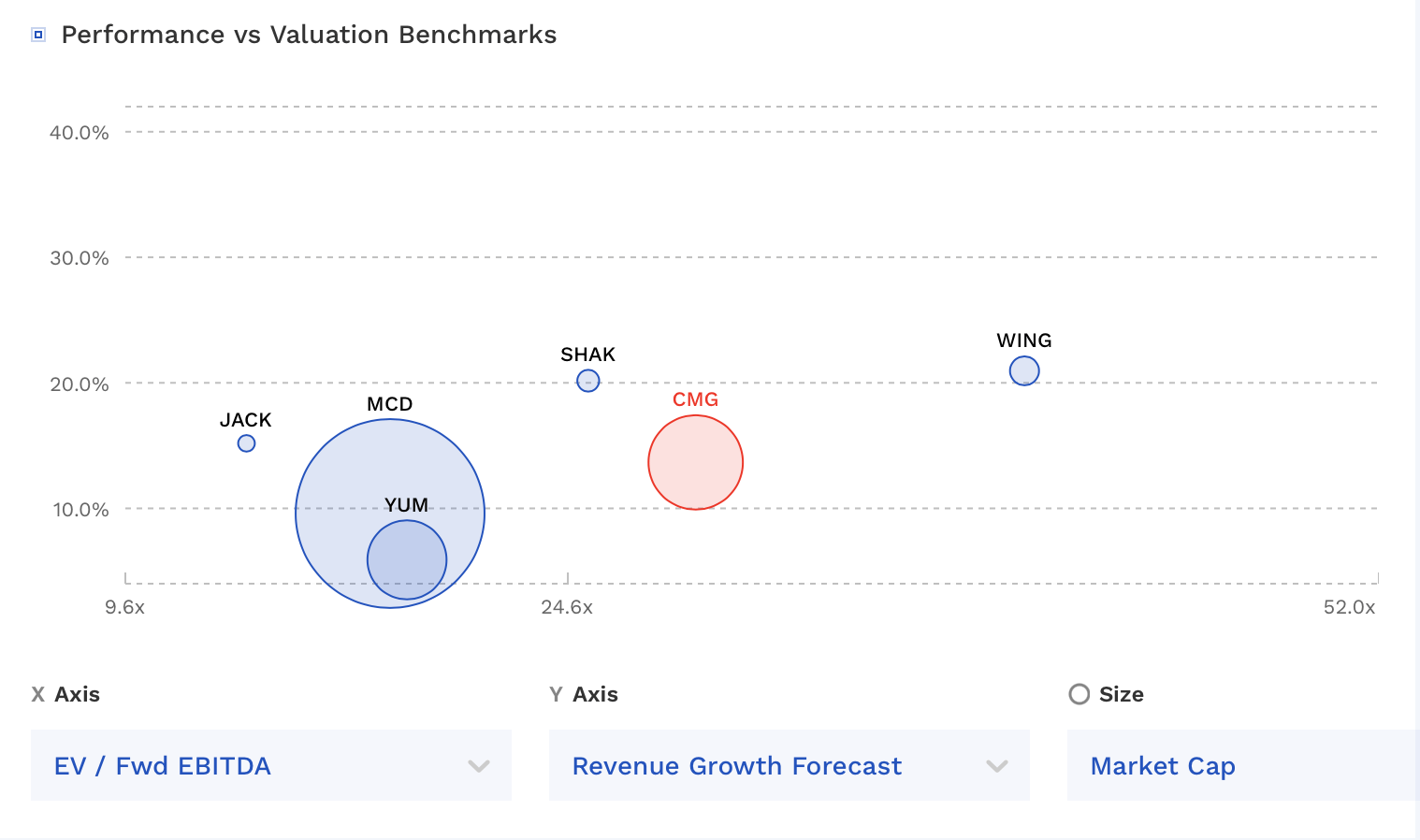

Exterior of Wingstop (WING) CMG is likely one of the highest valued QSR on the market. Notably, WING makes use of a franchise mannequin, which tends to get increased valuations.

CMG Valuation Vs Friends (FinBox)

Conclusion

When a inventory is priced for perfection, an in-line quarter, irrespective of how robust it’s, normally isn’t going to be ok, and never surprisingly, CMG’s inventory fell -10% the next session after its report. CMG continues to be an ideal firm, however within the close to time period, issues additionally actually set to grow to be tougher. It would lap worth hikes, in addition to a very talked-about LTO that was serving to drive gross sales. As such, how the corporate’s gross sales carry out in September needs to be fairly telling. That would be the final month of its Q3 interval, however it’ll actually affect the quarter and extra importantly This autumn steering.

Even with the current decline within the inventory worth, CMG nonetheless isn’t low-cost. In actual fact, I proceed to suppose the QSR house generally is fairly extremely valued, as your entire business has been driving inflationary and worth hike advantages that ought to start to wane, whereas they buying and selling at fairly excessive historic valuations. I’ll proceed to watch CMG, as it’s a nice firm and positively price an funding on the proper worth.

{kind=link}