Reader Econned, in response to my posting of images of M2 divided by actual GDP, and the GDP deflator, castigates me for the usage of standard financial aggregates:

M2? It is a pitifully disingenuous put up – those that see worth in QTM use a divisia index because the financial combination. And you recognize this.

I’m conscious of the theoretical bases for the usage of divisia financial measures. I’m, nonetheless, unaware that use of those measures validates in a sturdy vogue the amount idea of cash.

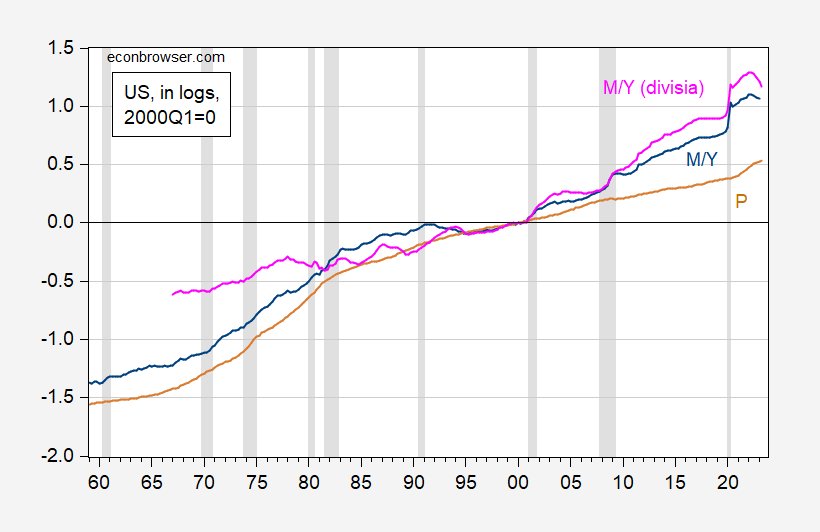

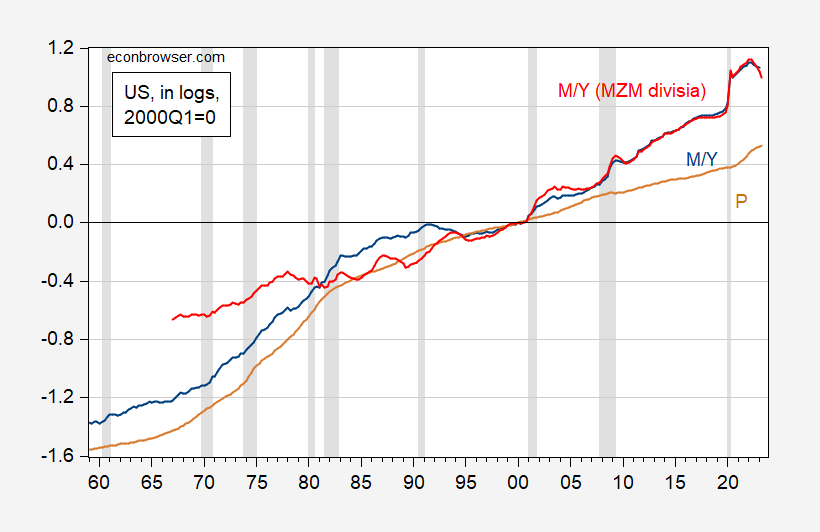

I reprise Determine 1 from the allegedly offending post, including in M2M and MZM (Figures 1 and a pair of, respectively).

Determine 1: Log M2 divided by actual GDP (blue), log GDP deflator (tan), log M2M divisia (pink), all 2000Q1=0. NBER outlined peak-to-trough recession dates shaded grey. Supply: BEA, Federal Reserve Board by way of FRED, Center for Financial Stabiity, NBER, and writer’s calculations.

Determine 2: Log M2 divided by actual GDP (blue), log GDP deflator (tan), log MZM divisia (crimson), all 2000Q1=0. NBER outlined peak-to-trough recession dates shaded grey. Supply: BEA, Federal Reserve Board by way of FRED, Center for Financial Stabiity, NBER, and writer’s calculations.

Now, it’s true that if one makes use of MZM or M2M as an alternative of M2 in a most probability estimation of the cointegrating vector over the 1968-2023 interval, one can discover a bit extra proof for cointegration (reject at 10% msl utilizing hint and max eigenvalue assessments, asymptotic important values, and permitting for intercept in cointegrating vector and VAR), however the worth coefficient has the improper signal. So, I’m completely satisfied to make use of the divisia indices as an alternative of standard, however I’m undecided you resurrect the empirical model of the amount idea by doing so.

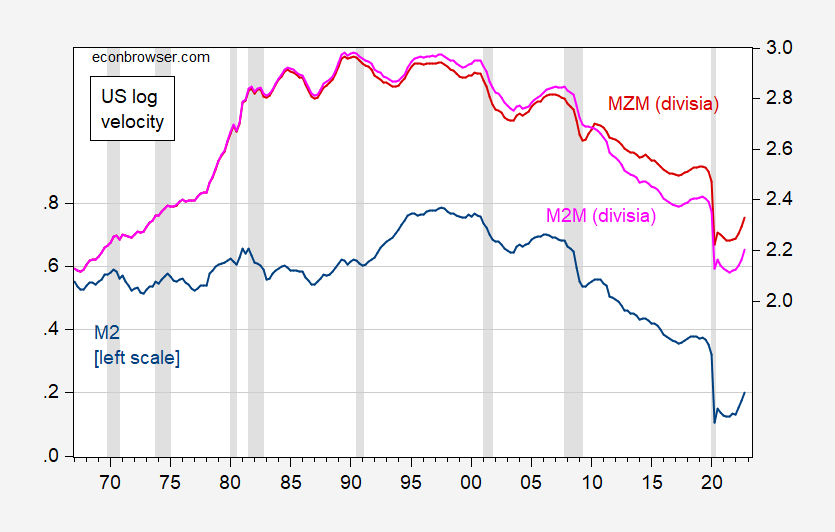

For completeness’s sake, I plot velocity for M2 (blue), MZM (crimson), and M2M (pink).

Determine 3: Log nominal GDP divided by M2 (blue, left scale), divided by M2M divisia (pink), divided by by MZM divisia (crimson), all 2000Q1=0. NBER outlined peak-to-trough recession dates shaded grey. Supply: BEA, Federal Reserve Board by way of FRED, Center for Financial Stabiity, NBER, and writer’s calculations.

Reader Econned, in response to my posting of images of M2 divided by actual GDP, and the GDP deflator, castigates me for the usage of standard financial aggregates:

M2? It is a pitifully disingenuous put up – those that see worth in QTM use a divisia index because the financial combination. And you recognize this.

I’m conscious of the theoretical bases for the usage of divisia financial measures. I’m, nonetheless, unaware that use of those measures validates in a sturdy vogue the amount idea of cash.

I reprise Determine 1 from the allegedly offending post, including in M2M and MZM (Figures 1 and a pair of, respectively).

Determine 1: Log M2 divided by actual GDP (blue), log GDP deflator (tan), log M2M divisia (pink), all 2000Q1=0. NBER outlined peak-to-trough recession dates shaded grey. Supply: BEA, Federal Reserve Board by way of FRED, Center for Financial Stabiity, NBER, and writer’s calculations.

Determine 2: Log M2 divided by actual GDP (blue), log GDP deflator (tan), log MZM divisia (crimson), all 2000Q1=0. NBER outlined peak-to-trough recession dates shaded grey. Supply: BEA, Federal Reserve Board by way of FRED, Center for Financial Stabiity, NBER, and writer’s calculations.

Now, it’s true that if one makes use of MZM or M2M as an alternative of M2 in a most probability estimation of the cointegrating vector over the 1968-2023 interval, one can discover a bit extra proof for cointegration (reject at 10% msl utilizing hint and max eigenvalue assessments, asymptotic important values, and permitting for intercept in cointegrating vector and VAR), however the worth coefficient has the improper signal. So, I’m completely satisfied to make use of the divisia indices as an alternative of standard, however I’m undecided you resurrect the empirical model of the amount idea by doing so.

For completeness’s sake, I plot velocity for M2 (blue), MZM (crimson), and M2M (pink).

Determine 3: Log nominal GDP divided by M2 (blue, left scale), divided by M2M divisia (pink), divided by by MZM divisia (crimson), all 2000Q1=0. NBER outlined peak-to-trough recession dates shaded grey. Supply: BEA, Federal Reserve Board by way of FRED, Center for Financial Stabiity, NBER, and writer’s calculations.

{kind=link}