maybefalse/iStock Unreleased through Getty Photographs

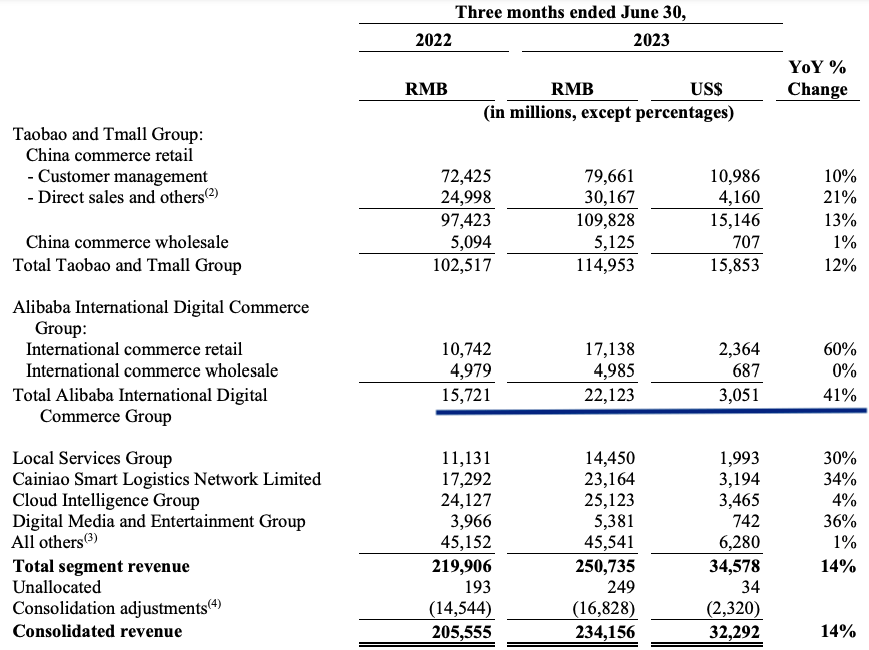

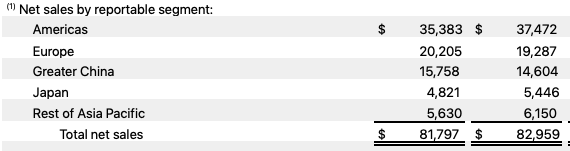

Alibaba (NYSE:BABA) is quickly diversifying its income base which can assist the corporate scale back China-centric headwinds and construct an extended progress runway. Within the latest quarter, the Worldwide Commerce section reported YoY income progress of 41% in contrast to a 14% total progress charge. This exhibits that the Worldwide Commerce section has reported a YoY income progress charge 27 share factors greater than the general progress charge. The same pattern could possibly be seen within the March-ending quarter when the Worldwide Commerce section reported 29% YoY income progress in comparison with 2% total progress charge. In the previous article, “Alibaba: Simpler comps can ship earnings shock”, it was talked about that Alibaba might simply beat the consensus which was clearly seen within the earnings.

The upper progress charge in worldwide commerce has elevated its income share to 9.5% of the consolidated income. If the present pattern continues, the worldwide commerce section will contribute over 25% of the cumulative income base by the tip of 2025. This may assist scale back the geographic danger for Alibaba inventory and supply the corporate with new progress choices. Alibaba has already reached market management in a number of main geographic areas. It’s also attempting to achieve the next market share within the profitable European market by investing in logistics and enhancing the platform.

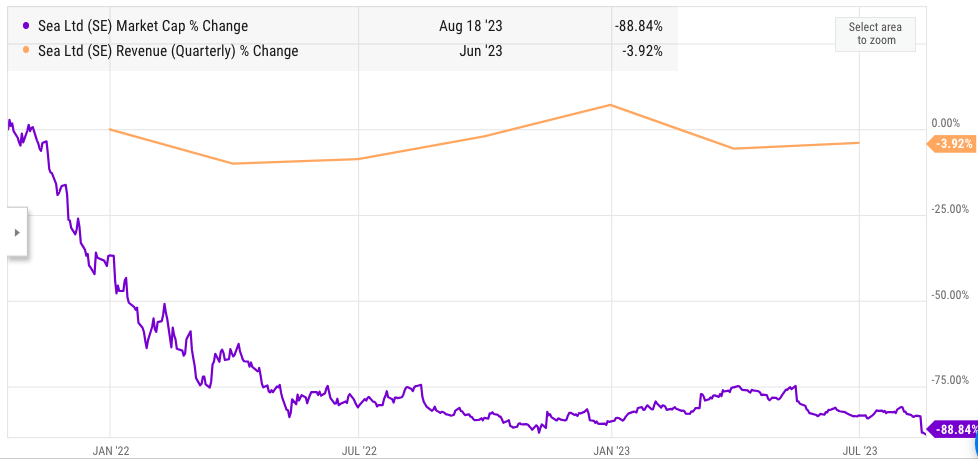

Considered one of its fundamental worldwide rivals, Sea Restricted (SE), is dealing with vital challenges and its market cap has dropped by near 90% making it tough to boost new funds. This could assist the corporate enhance margins and ship sooner progress in key worldwide areas. Alibaba inventory is buying and selling at a really low a number of which may give long-term traders an excellent entry level as the corporate pivots its focus to worldwide areas.

Optimistic diversification pattern

A brief look on the latest income progress metrics for various segments of Alibaba exhibits that the Worldwide Digital Commerce enterprise has a totally totally different progress trajectory in comparison with different segments. The reopening of the economic system has helped the Digital Media enterprise. Nonetheless, the YoY progress of Digital Media at 36% remains to be decrease than Worldwide Commerce section. The largest section is Taobao and Tmall Group which reported solely 12% YoY income progress. This exhibits that there are sturdy basic progress alternatives within the Worldwide commerce section which is driving the expansion on this enterprise.

Firm Filings

Determine 1: The expansion trajectory of Worldwide commerce is greater than all different segments

A better income base and sooner progress in worldwide commerce is lifting the general income progress of the corporate. Within the latest quarter, the worldwide commerce section contributed 23% of the whole incremental income for the corporate on a YoY foundation. If the present pattern continues, we might see worldwide commerce contribute over half of the whole incremental income for Alibaba by the tip of 2025. This may put extra give attention to worldwide operations and scale back the headwinds confronted by the corporate inside China.

The same pattern was seen in the previous quarter when the worldwide commerce section reported 29% YoY income progress in comparison with 2% YoY total income progress. Therefore, the worldwide enterprise had income progress 27 share factors greater than total progress.

Decrease aggressive stress

Alibaba faces a lot decrease aggressive stress in a number of worldwide areas. Considered one of its subsidiaries is Trendyol which has achieved market leadership in Turkey and is constructing a serious logistics hub as an entry level for items to Europe. E-commerce enterprise requires large funding potential to construct logistics and drive costs decrease for patrons. That is normally not potential for smaller firms. We might see many of the e-commerce enterprise in worldwide areas get divided by larger firms like Alibaba, Amazon (AMZN), Walmart (WMT), and some others. This pattern has been seen in larger worldwide areas like India the place a majority of e-commerce market share is carved between Amazon and Walmart’s Flipkart subsidiary.

One of many greatest rivals for Alibaba is Sea Restricted which competes in opposition to Alibaba’s Lazada in Southeast Asia. Sea Restricted has seen its market cap decline by a staggering 90% within the final two years attributable to large losses.

Ycharts

Determine 2: Market cap and quarterly income progress of Sea Restricted in final 2 years

One of many issues dealing with Sea Restricted is that it’s too small to successfully compete with Lazada. The corporate used to burn money to develop its market share. Nonetheless, this technique won’t work now because the market cap of Sea Restricted has declined considerably and the corporate won’t achieve leverage by diluting the shares additional.

Alibaba has just lately invested $845 million in Lazada. This can be a long-term benefit with Lazada and different worldwide models that may depend upon Alibaba for sources and technical expertise to enhance logistics and their platform.

Lengthy-Time period Tailwind

The regulatory setting in numerous areas could be very totally different. For instance, Alibaba has stopped investments in India attributable to rising geopolitical tensions between India and China. However, the laws are very engaging in Southeast Asia the place Alibaba has reported speedy progress. Even inside totally different European Union international locations, there are very totally different laws. Therefore, worldwide progress diversifies the regulatory danger for the corporate.

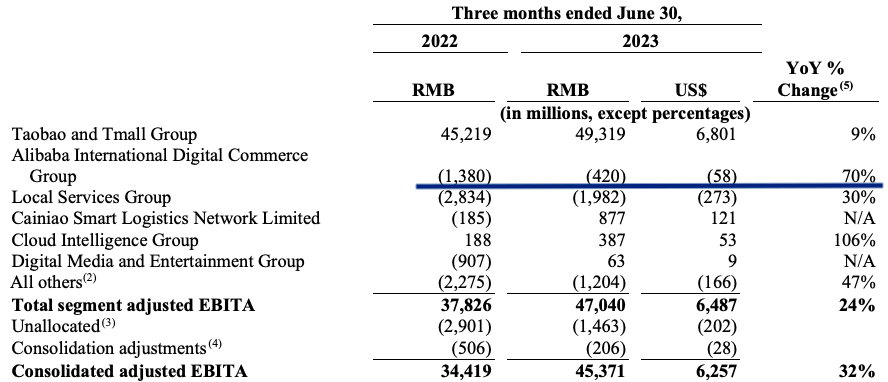

The Worldwide commerce section can also be near the break-even level. Within the latest quarter, the Worldwide commerce enterprise reported losses of $58 million in comparison with greater than 3 times this stage within the year-ago quarter.

Firm Filings

Determine 3: Fast decline in losses for Worldwide commerce

There are a variety of worldwide areas the place Alibaba can develop. On the present progress trajectory, this section will contribute over 25% of the whole income base for the corporate by the tip of 2025. This could scale back the China-based danger for the inventory considerably. The long run spinoffs carry some uncertainty in how and when the administration will divide totally different segments. Nonetheless, it’s extremely doubtless that the Worldwide commerce section will likely be a key driver for future inventory progress.

Affect on Alibaba inventory

Any unfavourable information from China causes an on the spot headwind for Alibaba inventory. Now we have seen this in latest days when unfavourable macroeconomic knowledge in China led to a ten% decline in inventory regardless of good earnings numbers. The geopolitical tensions between U.S. and China are additionally rising and we might see better commerce restrictions on chips and different items because the presidential race heats up.

On this background, the significance of Worldwide commerce will increase considerably. Alibaba’s administration is prone to focus all its consideration on enhancing the expansion trajectory inside totally different worldwide areas for the following few quarters. Wall Road might reward affected person long-term traders with good returns as Alibaba inventory turns into extra of a world e-commerce platform as an alternative of a China-centric firm.

Ycharts

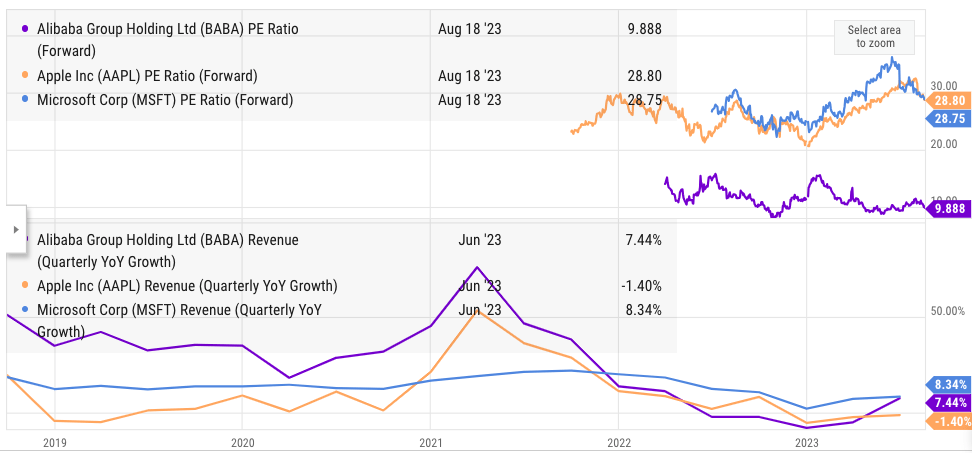

Determine 4: Quarterly YoY income progress and ahead P/E comparability between Alibaba and different tech firms

Alibaba’s ahead P/E ratio is lower than 10 which is a large low cost to different massive tech firms like Apple (AAPL) and Microsoft (MSFT). The YoY income progress of Alibaba is beginning to enhance and we might see higher numbers on this metric because the macroeconomic scenario improves in China. The rise in income share from worldwide areas will even enhance the general progress trajectory for Alibaba. Presently, Alibaba’s worldwide operations contribute solely 10% of the income whereas firms like Apple obtain over 60% of income from outdoors the home U.S. market. Apple receives shut to twenty% of the income from China.

Apple’s Filings

Determine 5: Apple’s income share from totally different areas within the latest quarter

As this decade progresses, we should always proceed to see greater geographic diversification of Alibaba’s income base. It’s definitely potential that Alibaba’s income base will look a bit like Apple the place the home market contributes lower than 50% of the whole income. This may take one other decade however long-term traders might see decrease danger from Alibaba inventory within the subsequent few years.

Investor Takeaway

Alibaba’s Worldwide commerce section is rising at a sooner tempo in comparison with different segments. This has elevated the income share of Worldwide commerce to 10%. On the present progress pattern, Worldwide Commerce section might contribute 25% of the income share by the tip of 2025. This could scale back the geopolitical danger related to the inventory and we might see higher valuation a number of.

Current earnings report exhibits that Alibaba’s YoY income progress is beginning to enhance and it’s already a lot better than Apple. The ahead income progress estimates are additionally fairly sturdy for Alibaba. Lengthy-term traders might take into account Alibaba as an excellent buy-and-hold possibility and wait out the present macroeconomic and geopolitical headwinds.

{kind=link}