In the present day we’re lucky to current a visitor submit written by Natasha Che, Alexander Copestake and Davide Furceri (all on the Worldwide Financial Fund) and Tammaro Terracciano (IESE Enterprise College, Barcelona). The views expressed on this paper are these of the authors and never essentially these of the establishments with which they’re affiliated.

Crypto belongings range considerably of their design and worth proposition—from an inflation hedge to a supplier of extra environment friendly funds, censorship-resistant computing or property rights—but their costs have moved in frequent cycles. Intervals of exponential returns have attracted retail and institutional traders alike, whereas subsequent crashes have drawn rising consideration from politicians and regulators. And fluctuations in crypto markets may be more and more synchronized with different asset courses: previous to 2020, Bitcoin offered a partial hedge in opposition to market threat, but it has since turn out to be more and more correlated with the S&P500 (Adrian, Iyer, and Qureshi, 2022).

In a new paper, we make clear the drivers of crypto asset costs by answering the next questions. To what extent is there a standard cycle throughout crypto belongings? Are crypto markets changing into extra synchronized with international fairness markets? In that case, why? Provided that US financial coverage has been recognized as a key driver of the worldwide monetary cycle (Miranda-Agrippino and Rey, 2020), does US financial coverage affect the crypto cycle to an analogous extent? In that case, by means of which channels?

We start by utilizing a dynamic issue mannequin to establish a single dominant development in crypto-asset costs. Utilizing a panel of every day costs for a number of of the longest-lived tokens, which collectively account for roughly 75% of complete crypto market capitalization, we decompose their variation into asset-specific idiosyncratic disturbances and a standard part. We discover that the ensuing “crypto issue” explains roughly 80% of the variance within the crypto value information.

We then research the connection of this crypto issue to a set of world fairness elements, constructed utilizing the fairness indices of the most important nations by GDP (within the spirit of Rey, 2013; Miranda-Agrippino and Rey, 2020). We discover a optimistic correlation over all the pattern, pushed by a very robust correlation since 2020. The rising co-movement just isn’t restricted to Bitcoin vis-a-vis the S&P500, however pertains extra broadly to the crypto and international fairness elements. Disaggregating throughout fairness markets, we discover that the crypto issue correlates most strongly with the worldwide tech issue and the small-cap issue since 2020, whereas it’s apparently much less correlated with the worldwide monetary issue.

The elevated correlation between crypto and equities coincides with the expansion within the participation of institutional traders in crypto markets since 2020. Though establishments’ publicity is small relative to their steadiness sheets, their absolute buying and selling quantity is way bigger than that of retail merchants. Specifically, the amount of buying and selling by institutional traders in crypto exchanges elevated by greater than 1700% (from roughly $25 billion to greater than $450 billion) from 2020Q2 to 2021Q2 (Auer et al., 2022). Since institutional traders commerce each shares and crypto belongings, this has led to a progressive improve within the correlation between the chance profiles of marginal fairness and crypto traders, which in flip is related to the next correlation between the worldwide fairness and crypto elements. When decomposing issue actions following Bekaert, Hoerova, and Lo Duca (2013), we discover that correlation within the mixture efficient threat aversion of crypto and equities can clarify a big share (as much as 65%) of the correlation between the 2 elements.

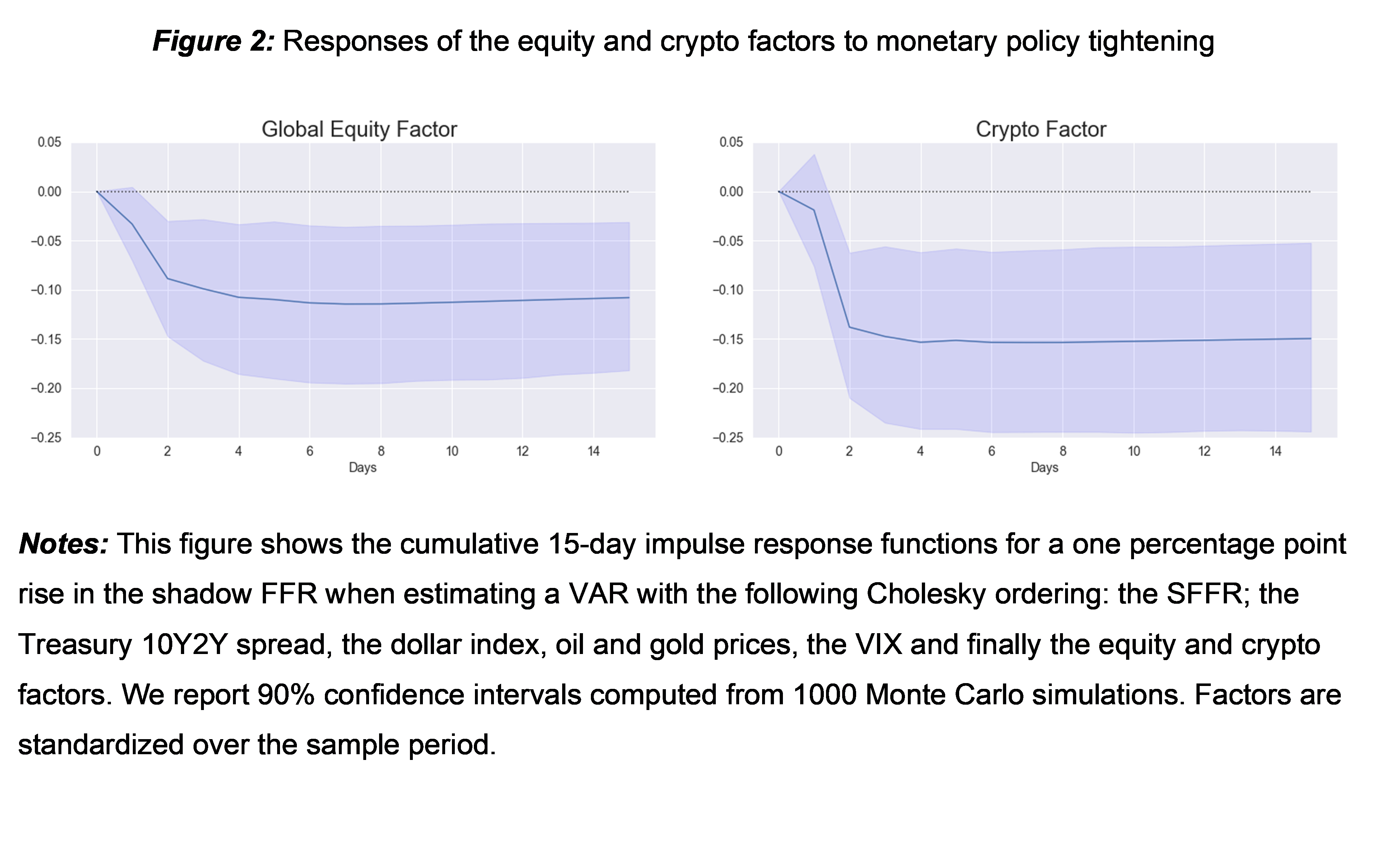

Since US financial coverage impacts the worldwide monetary cycle (Miranda-Agrippino and Rey, 2020), the excessive correlation between equities and crypto suggests an analogous affect on crypto markets. We check this speculation utilizing a every day VAR with the shadow federal funds price (SFFR) of Wu and Xia (2016) to account for the essential position of steadiness sheet coverage over our pattern interval. We discover that US financial coverage impacts the crypto cycle, because it does with the worldwide fairness cycle, contrasting starkly with claims that crypto belongings present a hedge in opposition to market threat. A one proportion level rise within the SFFR results in a persistent 0.15 normal deviation decline within the crypto issue over the next two weeks, relative to a 0.1 normal deviation decline within the fairness issue.

We discover proof that the risk-taking channel of financial coverage is a vital channel driving these outcomes, paralleling the findings of Miranda-Agrippino and Rey (2020) for international fairness markets. A financial contraction results in a discount of the crypto issue that’s accompanied by a surge in a proxy for the mixture efficient threat aversion in crypto markets. When splitting the pattern in 2020, we discover that the affect on threat aversion in crypto markets is important just for the post-2020 interval, in keeping with the entry of institutional traders reinforcing the transmission of financial coverage to the crypto market.

We rationalize our leads to a mannequin with two heterogeneous brokers, specifically crypto and institutional traders. The upper the relative wealth of institutional traders, the extra comparable the crypto mixture efficient threat aversion turns into to their threat urge for food and the extra correlated are crypto and fairness markets. Even in our easy framework, spillovers from crypto to equities can come up: if establishments’ crypto holdings turn out to be massive, a crash in crypto costs reduces equilibrium returns in equities.

Total, our outcomes spotlight that regardless of the vary of explanations for crypto asset values, most variation in crypto markets is extremely correlated with fairness costs and extremely influenced by Fed insurance policies. Development in institutional participation has strengthened these conclusions and elevated the chance of spillovers from crypto markets to the broader economic system.

References

Adrian, Tobias, Tara Iyer, and Mahvash S. Qureshi, 2022, Taking shares: Financial coverage transmission to fairness markets, IMF Weblog.

Auer, Raphael, Marc Farag, Ulf Lewrick, Lovrenc Orazem, and Markus Zoss, 2022, Banking within the shadow of Bitcoin? The institutional adoption of cryptocurrencies, BIS Working Papers.

Bekaert, Geert, Marie Hoerova, and Marco Lo Duca, 2013, Danger, Uncertainty and Financial Coverage, Journal of Financial Economics.

Miranda-Agrippino, Silvia, and Helene Rey, 2020, U.S. Financial Coverage and the World Monetary Cycle, Evaluate of Financial Research.

Rey, Helene, 2013, Dilemma not Trilemma: The World Monetary Cycle and Financial Coverage Independence, Jackson Gap Convention Proceedings.

Wu, Jin Cynthia, and Fan Dora Xia, 2016, Measuring the Macroeconomic Impression of Financial Coverage on the Zero Decrease Sure, Journal of Cash, Credit score and Banking.

This submit written by Natasha Che, Alexander Copestake, Davide Furceri and Tammaro Terracciano.

{kind=link}