Photofex/iStock Editorial through Getty Photographs

Pricey readers/followers,

It should not shock you at this level that I favor investing in high quality dividend shares which have through-cyclic security. Whereas I do spend money on cyclical corporations, I attempt to ensure that these corporations come at very excessive cyclical safeties, that means that you’ve got some form of a baseline dividend. Except for this, credit score rankings ought to be excessive, and you need to really feel protected, primarily based on the asset high quality, that you simply’re not uncovered to something that is more likely to massively plummet in worth.

Whereas Hydro (OTCQX:NHYDY) is actually a unstable enterprise as a result of it is uncovered to the ups and downs of the sector, it is from any form of dangerous firm. I’ve made returns within the triple digits, as you’ll be able to see right here (Source) with this funding, although I do not imagine that the corporate has a very huge upside from the present valuation.

Let’s examine what we’ve going for us as we transfer into 3Q23, and what we may anticipate from Hydro on a ahead foundation.

Norsk Hydro – A lot to love about Aluminum, simply not the valuation

2Q23 outcomes are the newest set of outcomes we’ve. This quarter noticed, as earlier than, money circulation within the billions of NOK, and an adjusted RoACE on a very good stage – above 13.5%. Given the cyclicality we’re going into, that is good.

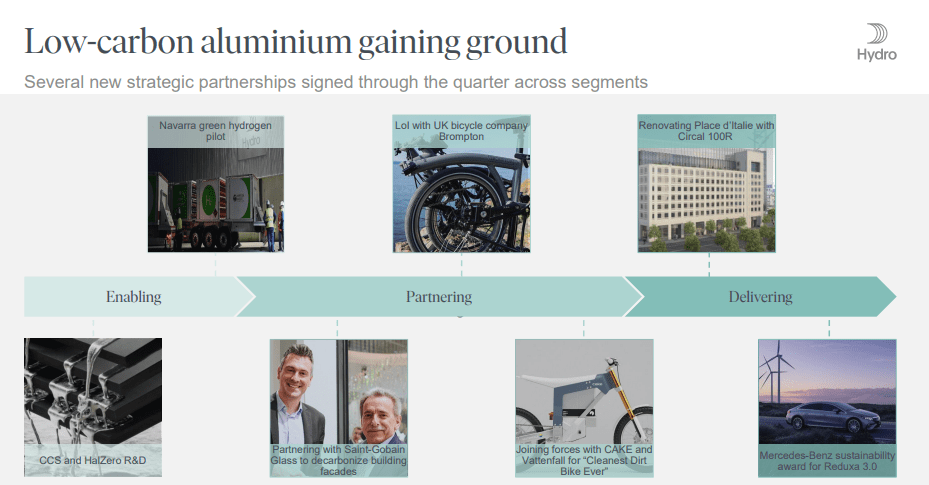

Hydro’s enchantment general has been its entry into “inexperienced” aluminum coupled with legacy operations. Inexperienced aluminum not essentially as a result of I’m an ESG investor, however for a similar cause I imagine inexperienced investments in Europe are literally not a nasty thought. As a result of the EU is already taxing non-ESG-adjusted assets and fundamental supplies at a excessive stage, this makes it “simple” to decide on suppliers like Hydro, which in flip get pleasure from important gross sales upsides over time in dwelling markets.

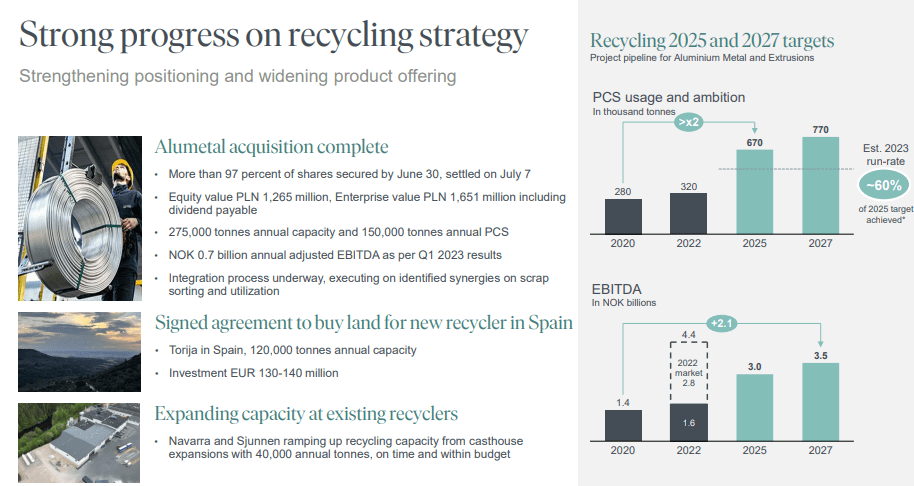

Hydro has delivered good progress on this quarter on its low-carbon aluminum options, and its M&A of Alumetal considerably strengthens its place in aluminum recycling. A lot to love there.

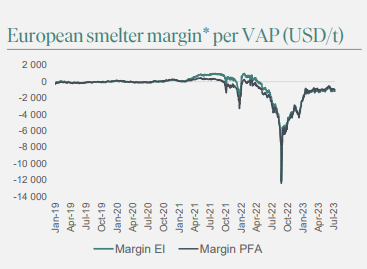

The corporate additionally elevated, on the unfavourable aspect, its CapEx estimate, attributable to investments, FX, and inflation, that are closely impacting issues. The market stability general, particularly smelter margins, is making ready to say no attributable to weaker demand in most Western markets.

Hydro IR (Hydro IR)

Hydro, to remind you, has been promoting plenty of aluminum to China. The Chinese language market, as a result of decline in property, has gone down. There’s additionally Russian metallic inventories, the place availability is rising resulting in a present provide/demand imbalance on the unfavourable aspect. Since Might of 2022, for a couple of yr, this has seen declining Aluminum costs. We’re not all the way down to a 2020 stage simply but – not right now, at the very least. However we’re actually down from earlier excessive ranges. And with the Geopolitical macro, we appear to be seeing a rise in Russian major aluminum export.

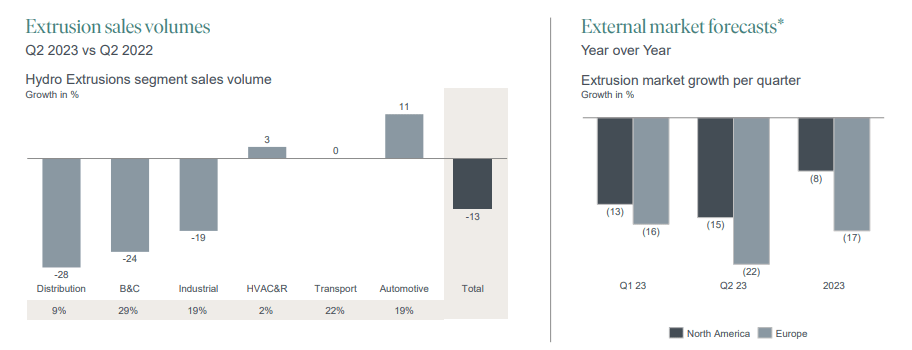

For Hydro-specific segments, there are enhancements and positives value noting. First amongst them is the enhancements in Automotive within the extrusion section – although the section continues to be up, market down for different demand forecast declines, from the economic B&C, and Distribution sectors. So automotive is nearly the one factor that is “up”.

NHY IR (NHY IR)

The essential factor, in case you’re trying to spend money on Hydro, stays to maintain your eye on the “ball” right here, on this case, the corporate’s long-term 2025E objectives. These objectives embrace diversification and management/robust market place in each low carbon alu and new energies.

The enhancements to those objectives, that is figuring out. The corporate’s enchancment packages are above expectations, and general it is simply very spectacular how shortly Norsk Hydro has turned this “ship” round. I say that as a result of I keep in mind not that a few years in the past when the corporate was being mentioned by analysts of being “achieved”, as a result of scandal with Alunorte. This has clearly not develop into the case.

Norsk Hydro IR (Norsk Hydro IR)

This has additionally pushed enhancements within the extrusion section, regardless of decrease demand, as a result of firm introducing section enhancements on the margin aspect. The greener product providing can also be a internet constructive right here attributable to higher gross sales. Enhancements have come from restructuring, higher SG&A, procurement enhancements, and operational enhancements.

Recycling is one other section I actually need to spotlight for the corporate as a result of it is working so properly.

NHY IR (NHY IR)

I anticipate the recycling section to develop into a main contributor to general firm revenue on the long run – and one of many recycling crops is definitely lower than quarter-hour away from the place I grew up.

In the meantime, once I began reviewing Norsk Hydro, low-carbon alu was nonetheless very a lot in its infancy. In the middle of only some years, it is develop into one of many hottest issues in your entire business – and companions appear to be lining up for the corporate.

NHY IR (NHY IR)

The corporate additionally nonetheless has ongoing renewable segments with its Hydro Rein section. The long-term plan is a strong portfolio of renewable producing belongings, each on the offshore wind (probably), onshore wind and photo voltaic. The corporate has already acquired 4 photo voltaic tasks throughout Scandinavian with a mixed capability when completed of upwards of 800 Mw.

On a excessive stage, outcomes have been good, regardless of decrease costs, larger fastened prices, larger debt prices, and FX not with the ability to weigh up the positives from vitality pricing, bettering margins, and effectivity positive factors. The corporate is lifting its steering, and the plans going ahead stay the identical. Working capital/working capital can also be seeing enhancements, and although the corporate’s internet debt/EBITDA really elevated each attributable to dividends (nearly 11.5B NOK) and changes of round 4.6B NOK, it is nonetheless not at something near a worrying stage.

As a substitute, what I might control is to see if these extrusion margins and revenue ranges are literally sustainable. That was an enormous shock for me on this quarter, as I anticipated them to be worse. Nonetheless, attributable to robust effectivity and powerful financial savings, the corporate really did very properly right here.

We must be clear that we’re going right into a “downcycle” with the corporate really happening when it comes to earnings right here. The forecasts at the moment verify this (in case you imagine them). The 2023E EPS on an adjusted foundation is ready to say no by greater than 45% (Supply: FactSet). What occurs past that is then a query of your outlook. The typical estimate from the identical analyst is a median reversal of round 7-8% per yr till 2025E. Me, I say that is solely probably partly – and I derive this from the truth that Hydro nearly cannot be precisely forecast at any historic time limit.

Let me present you what I imply within the valuation part.

Hydro – Valuation stays excessive for what’s forward, however I nonetheless say “BUY” on the long-term upside.

When you recall my final article on the corporate, I did name it enticing and gave it a 68 NOK share value. I simply did not name it “low cost”. I am not shifting my value goal on this article, regardless of the outlook for what can solely be thought of a slightly important drop in revenue.

What I imply when the corporate is not forecastable is that solely 6-17% of the time, analysts are capable of precisely forecast this firm with any form of accuracy even with a 10-20% margin of error. At different instances, we’ve misses near the triple digits each on the unfavourable and the constructive aspect. Such beats usually are not essentially a constructive to me, it simply implies that the corporate is tough to forecast – as this one really is.

To place this into context, NHY is anticipating a -13% common EPS development price till 2025E – although that is from a present stage of practically 11 NOK/share on an adjusted foundation.

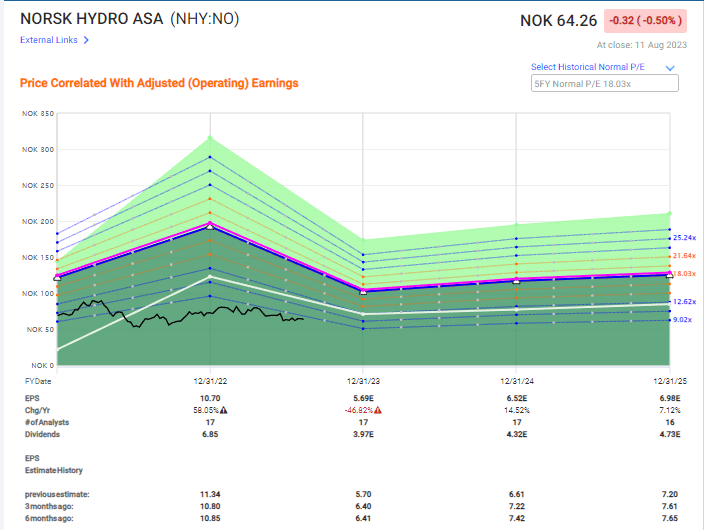

NHY Valuation (F.A.S.T graphs)

As you can even see, the corporate hasn’t actually seen any form of development inv valuation attributable to its 2022A outcomes. Most of these got here properly forward of the document outcomes, solely to drop down. I, due to this fact, imagine that it might be exuberant to anticipate the corporate to considerably go upward to normalize at 15-18x from right here on when it comes to P/E.

As a substitute, I might forecast it nearer to 10-12x P/E. 12x P/E could be probably the most I might see as lifelike right here, and that upside implies annualized RoR of simply above 15%, with a PT of round 79 NOK primarily based on a 2025E 12x P/E.

S&P International analysts give the corporate a median share value of 55 NOK on the low aspect and 100 NOK on the excessive aspect. I remind you at this level, that I invested in Hydro at under 27 NOK and held to a return above 170% of that valuation earlier than I bought the lion’s share of my funding. In comparison with the over 6% I held on the time, I am at the moment under 1.5%, and I’ve no intention of massively growing my stake right here.

Out of 14 analysts, solely 4 give the corporate a “BUY” – most are at “HOLD” or related. That is to not say Hydro is not massively overvalued right here – if it was, I would not have my “BUY” goal or my “BUY” Ranking.

However it’s removed from probably the most interesting, and even any considerably interesting funding right here right now.

At above 68 NOK, the thesis with a double-digit upside falls clearly aside as I see it. You simply cannot simply make that upside there in case you purchase at 70 NOK, even when the corporate realizes the present forecast.

When you spend money on Hydro, you need to deal with the basics and the valuation of the corporate. Going by DCF or different forecast strategies actually does not work, particularly when you begin ratcheting up that share value. For steering as to what can occur in unfavourable instances, simply take a look at how deeply the corporate fell throughout “dangerous” instances. It may accomplish that once more.

That is why I focus very clearly on shopping for this firm solely at low cost pricing – and if I can not, I am prepared to attend.

So whereas I do say “BUY” right here – and I do – I additionally say to have a look at different options.

Thesis

- Norsk Hydro is at the moment near pretty valued to normalized future earnings and my new improved value goal going into 2Q23.

- The potential returns from at the moment’s ranges at the moment are acceptable in comparison with what different funding options out there provide us.

- At its present valuation, Norsk Hydro is a bare-bones “BUY” with at the very least the beginnings of what I think about to be a lovely upside. The value goal is 68 NOK.

Bear in mind, I am all about:

- Shopping for undervalued – even when that undervaluation is slight and never mind-numbingly huge – corporations at a reduction, permitting them to normalize over time and harvesting capital positive factors and dividends within the meantime.

- If the corporate goes properly past normalization and goes into overvaluation, I harvest positive factors and rotate my place into different undervalued shares, repeating #1.

- If the corporate does not go into overvaluation however hovers inside a good worth, or goes again all the way down to undervaluation, I purchase extra as time permits.

- I reinvest proceeds from dividends, financial savings from work, or different money inflows as laid out in #1.

Listed below are my standards and the way the corporate fulfills them (italicized).

- This firm is general qualitative.

- This firm is basically protected/conservative & well-run.

- This firm pays a well-covered dividend.

- This firm is at the moment low cost.

- This firm has a practical upside primarily based on earnings development or a number of enlargement/reversion.

I can not name Hydro “low cost”, however I’m calling it “enticing” right here even after a slight drop after my final articles.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a serious U.S. trade. Please concentrate on the dangers related to these shares.

{kind=link}