ExperienceInteriors

By Richard Schwam, CFA

Flagging workplace occupancy charges have municipal bond traders involved. However US cities have a couple of card to play within the income sport.

From the Bay Space to Boston, shrinking workplace footprints have been producing gloomy headlines.

With speak of downtown dying spirals, some municipal bond traders concern that declining workplace occupancy – a aspect impact of elevated office flexibility – may deplete massive cities’ coffers.

However whereas workplace vacancies stay a priority, most US cities have mechanisms to guard their funds – and people of municipal bondholders.

Cities Have a Broad Vary of Funding Sources

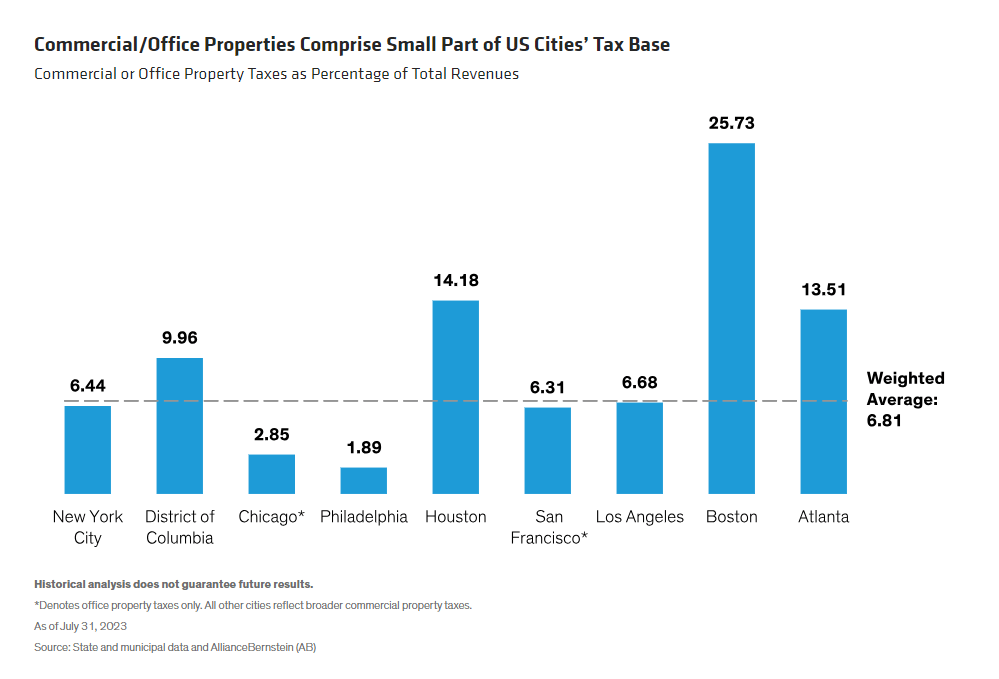

First off, we have to handle a false impression: US cities aren’t almost as depending on industrial and workplace taxes as many imagine.

It’s true that property taxes are sometimes the biggest supply of tax income for big cities, however they account for simply 30% of complete income, on common, in line with the City Institute – with workplace contributing only a portion of that.

In actual fact, of the biggest US cities by debt excellent, industrial or workplace property taxes account for simply 6.8% of complete revenues, on common (Show).

Cities produce other vital sources of income they will faucet. These embrace consumer costs, comparable to sewerage and parking charges, earnings taxes, gross sales and use taxes, and intergovernmental transfers.

The power to attract from a variety of funding implies that even a 50% drop in workplace property tax revenues would symbolize a 3.4% lower, on common, in complete revenues – not a debilitating problem to cities, in our view.

Untethering Taxes from Property Values

Even when workplace properties have been to expertise steep valuation declines, cities have mechanisms to blunt and even nullify the impact on property taxes, cushioning the budgetary impression of declining actual property values.

For instance, Chicago units its property tax levies independently of actual property worth.

The method is analogous for many cities in New York State as effectively, the place annual property-tax will increase are restricted to the lesser of two% or the speed of inflation.

This successfully untethers property taxes from actual property values – although it doesn’t restrict property tax charges or evaluation values.

And whereas New York Metropolis’s property taxes are extra intently tied to actual property values, adjustments within the worth of town’s tax base are phased in over 5 years. This limits draw back threat in any given 12 months and offers town time to regulate to altering values.

Due to related mechanisms throughout the US, metropolis property-tax income is considerably insulated from broader actual property shocks. A 2008 study by the Federal Reserve discovered that property taxes have a beta of 0.4, which means that property taxes rise or fall by 40% as a lot because the broader actual property market. Furthermore, this relationship tends to have a three-year lag, offering time for cities to regulate.

A Nearer Have a look at Workplace Property Values

Like many traders, we’re involved in regards to the worth of workplace properties within the new world of hybrid work and work-from-home.

Dwindling workforces can sap the vitality of downtowns and have a multiplier impact on companies that depend upon foot site visitors.

Increased rates of interest additionally make financing workplace properties more difficult, placing added stress on valuations.

However there’s extra to the image than meets the attention.

Some market observers estimate that workplace property values have fallen within the neighborhood of 30% since March 2022. These estimates are derived from appraisal-based information – not precise transactions, which inform a unique story.

Whereas declines in appraisal-based indices can look dramatic, transaction-based indices present that workplace property values have fallen solely 8% over the previous 12 months ended June 30, 2023, on very low gross sales quantity.

We’re not saying that important declines gained’t occur, however the illiquid nature of economic actual property lengthens the length over which potential declines are realized – to cities’ profit.

Cities Have the Flexibility to Tackle Market Shifts

The trump card for big municipal bond issuers is that, as authorities entities, they will and do change the principles to assist shield themselves in opposition to financial shifts.

For instance, in response to the rise in digital commerce, many states enacted legal guidelines permitting them to gather gross sales taxes from on-line retailers with no bodily presence within the state.

In the same vein, we count on cities to reallocate their taxing authority to seize shifts in financial exercise away from places of work and towards extra energetic makes use of. So long as cities appeal to individuals, governments will discover a technique to tax them.

That ought to present a measure of confidence for municipal bondholders. Based on Moody’s, US cities’ median money steadiness as a proportion of working revenues elevated to 71% in 2021 from 34% in 2013, serving to to buffer in opposition to a weak workplace market.

We imagine the outlook for American downtowns isn’t almost as grim as some preserve. In our view, declining occupancy charges symbolize a shift in how US cities allocate assets, fairly than a harbinger of secular decline.

Fewer staff going to the workplace isn’t hurting the desirability of cities, which have seen a demographic recovery for the reason that pandemic.

In distinction to an period when deindustrialization spurred a decades-long exodus, US cities have the instruments to climate generational adjustments in how People reside and work – excellent news for each cities and the municipal bond traders who place their belief in them.

The views expressed herein don’t represent analysis, funding recommendation or commerce suggestions and don’t essentially symbolize the views of all AB portfolio-management groups. Views are topic to vary over time.

Editor’s Notice: The abstract bullets for this text have been chosen by Looking for Alpha editors.

{kind=link}