PeopleImages/iStock through Getty Photographs

Cielo (OTCPK:CIOXY) is certainly one of Latin America’s largest collectors and fee processors that, for a very long time, held a monopoly on bank card machines in Brazil.

Within the final 5 years, elements such because the arrival of stable competitors, the pandemic, commoditization of providers, low penetration of credit score merchandise, and decrease price effectivity have precipitated the corporate’s margins to fall sharply. Cielo’s shares went from $8 per share at first of 2018 to under $1.

Since hitting its lows early final yr, Cielo has recovered, canceling loss-making accounts, chopping prices, enhancing NPS, and rising its presence within the worthwhile middle-tier companies.

Cielo has a optimistic outlook within the quick time period, given the resumption of monetary volumes, improve in merchandise with embedded advances, credit score, and potential divestments in subsidiaries. The discounted valuation may additionally yield some returns within the quick time period.

Nevertheless, regardless of the extra favorable working setting, I see the macroeconomic situation as a progress obstacle for Cielo, together with overwhelming competitors and rising turbulence in complete traded quantity weighing on the funding thesis for the long run.

Cielo’s newest monetary outcomes

Earlier this yr, Cielo demonstrated a stable monetary efficiency in its most up-to-date earnings outcomes, displaying progress in revenues, profitability, and EBITDA margin and establishing environment friendly monetary administration and a technique that conjures up confidence out there.

Cielo’s Investor Relations

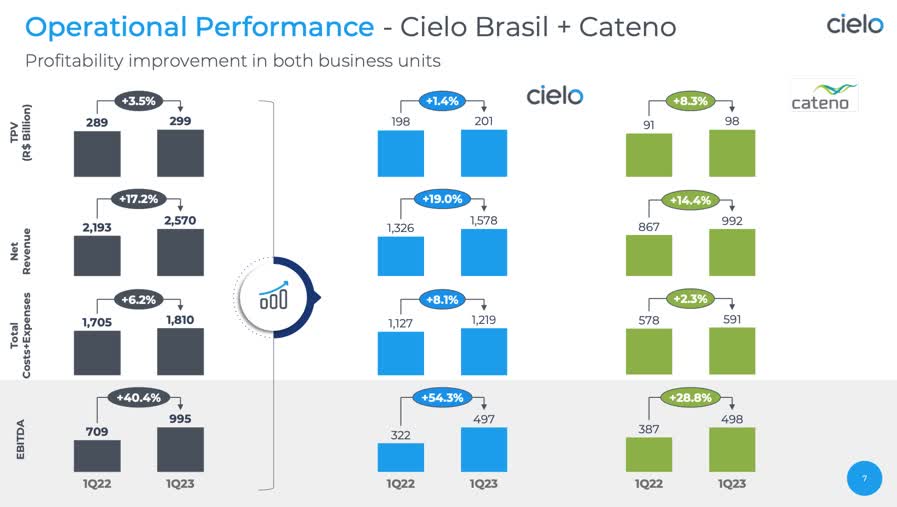

Revenues: The corporate achieved internet working revenues of R$2.57 billion in Q1 2023, a rise of 17.2% year-on-year. This progress was pushed by elevated quantity and yield at Cielo Brasil and Cateno (its subsidiary).

Profitability: Cielo’s recurring internet revenue within the first quarter of 2023 was R$440.8 million, representing a major progress of 85.1% in comparison with Q1 2022. Recurring EBITDA in Q1 2023 was R$994.9 million, up 40.4% from 1Q22. That is the best end result for the primary quarter since 2018. EBITDA margin additionally improved, reaching 38.7%, with a acquire of 6.4 proportion factors in comparison with Q1 2022.

Money and money equivalents: The corporate closed the quarter with R$2.35 billion in money and money equivalents, which represents a lower of R$1.16 billion in comparison with the primary quarter of 2022, however a rise of R$181 million in comparison with the earlier quarter. As well as, Cielo had R$6.43 billion in loans and financing on the finish of the Q1 2023.

Cielo will report its second-quarter leads to early August. The corporate is expected to report EPS of 0.05 and about R$2.91 billion in revenues, the place the monetary end result could are available barely higher than within the first quarter. The income from receivables anticipation could present a slight QoQ progress.

As well as, in keeping with the corporate, the forecast of a drop within the fundamental rate of interest (Selic) ought to cut back monetary bills within the order of R$150 million for each 1 p.p. diminished.

Higher margins however weaker volumes

Regardless of the optimistic outcomes through the first quarter of the yr, which showcased a major restoration in Cielo’s revenue margins, the latest investor assembly make clear more difficult prospects for Whole Cost Quantity (TPV).

At first of the yr, Cielo expected a TPV progress between 10% and 12% YoY for the trade, under that projected by the Brazilian Affiliation of Credit score Card Corporations (ABECS) and Providers of 14% to 18% YoY.

With this, Cielo has a extra conservative view of the longer term, emphasizing that it doesn’t see a restoration in quantity progress within the very quick time period – a number of the elements behind this extra conservative expectation of the autumn within the Brazilian retail trade.

Weaker consumption is said to banks’ restrictions on credit score provide, which have diminished limits and card issuance, along with the Pix (a Brazilian prompt fee system) that exchange debit and credit score operations, and the macroeconomic deterioration, such because the excessive household debt. At present, 80% of Brazilian households have debt, with 30% defaulting. As well as, family money owed signify about 33% of the nationwide GDP.

Cielo offered a TPV progress under the trade in the latest quarter. In response to ABECS knowledge, the TPV reported by the market in Q1 2023 was 10.7% YoY, whereas Cielo’s was just one.4% YoY.

Cielo’s Investor Relations

This weaker TPV progress than the market could be seen within the drop in massive accounts and SMBs, as it’s the firm’s focus phase in the intervening time and is the place it manages to generate probably the most profitability – turning on a warning signal for the corporate’s profitability in the long term.

Competitors is more and more suffocating Cielo

I imagine Cielo has appropriately shifted its focus to profitability quite than market share. At present, the corporate holds 24% of the market (down 2% YoY). The decline in market share ought to proceed with Cielo because it suffers in delivering some differentiator to carry its share versus stable competitors.

Over the previous few years, Cielo’s technique of specializing in small companies has helped increase its revenues, attaining 4 consecutive quarters of year-over-year progress. In Q1 2023, Cielo reported a income yield of 0.78% rising 12 bps YoY.

Nevertheless, as there was a discount in Cielo’s share in small companies, that is one other warning signal as Mercado Pago – a fintech arm of MercadoLibre (MELI) – emerges, which is beginning to take a look at the small enterprise sector (though wanting on the backside of the pyramid of the phase) and the growth of Rede, belonging to Itaú (ITUB) financial institution – one of many largest in Brazil – within the small enterprise market, the place it has as a aggressive differential the mixing with the financial institution’s buying system.

There may be additionally the potential for Mercado Pago and Rede reducing their costs to realize extra market share, which ought to imply that Cielo may additionally must impression its margins to not be left behind in its focus phase.

These are vital challenges for Cielo to face in the long run, the place rising its buyer base ought to grow to be more and more tough. Consequently, this could impose stress on optimizing its income technology.

Valuations mirror the bearishness

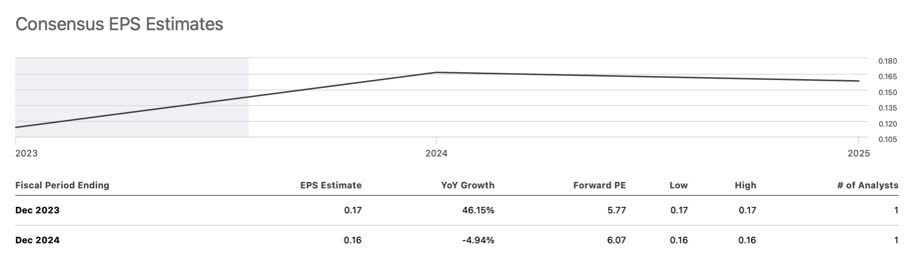

Contemplating that Cielo at the moment trades at a price-to-earnings a number of of 5.7 instances in 2023, which is roughly 42% under the trade common, it turns into evident that the market has little religion within the firm’s long-term prospects.

Though there may be an estimate of virtually 50% EPS progress by the tip of this yr, reaching $0.17, the consensus for 2024 signifies that EPS is predicted to be $0.16, ensuing within the firm nonetheless buying and selling at a ahead P/E a number of of 6 instances, which stays discounted.

Searching for Alpha

However, the discounted valuation could draw the eye of traders and controlling shareholders, probably resulting in Cielo going non-public and delisting from the general public inventory alternate. The corporate’s shareholder composition consists of two of Brazil’s largest banks: Bradesco (BBD), holding 30.1% of Cielo’s shares, and Banco do Brasil (OTCPK:BDORY), holding 28.6% of the corporate’s shares.

With the present inventory buying and selling at a reduced value in comparison with its earnings and the trade common, traders and the controlling shareholders may even see a possibility to accumulate extra shares and even take the corporate non-public. Such a transfer might give them higher management and advantages from a possible restoration in Cielo’s fortunes in the long term.

However, in fact, regardless of being a threat to the bearish thesis, that is nonetheless a purely speculative issue.

The underside line

Cielo is definitely not a foul firm, however it has fallen removed from the extent of success it loved within the not-so-distant previous.

The funding thesis for Cielo doesn’t look like very thrilling, primarily because of the low long-term progress pattern in its core enterprise. Moreover, the corporate faces fixed competitors in its core segments, and the high-risk Brazilian macroeconomic state of affairs with rising defaults and excessive family indebtedness provides additional stress.

However, Cielo’s technique of specializing in its core enterprise to extend monetary volumes and broaden its product portfolio to incorporate options comparable to anticipation and credit score, in addition to contemplating potential divestments in subsidiaries, could assist the corporate enhance its discounted valuation within the quick time period.

Nevertheless, within the long-term outlook, the corporate is experiencing a lack of market share and difficult prospects for Whole Cost Quantity (TPV), elevating doubts about whether or not the profitability-focused technique will likely be profitable.

General, though Cielo could have some potential within the quick time period as a consequence of its strategic initiatives, its uncertainties and challenges name for a cautious method in the long term.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a serious U.S. alternate. Please pay attention to the dangers related to these shares.

{kind=link}