yoh4nn/iStock through Getty Pictures

Funding Thesis

LSI Industries (NASDAQ:LYTS) is poised to capitalize on the optimistic outlook with strong citation exercise in Lighting and robust momentum in its Indoor lighting enterprise within the upcoming quarters. Moreover, the corporate’s strategic focus on product innovation to draw new prospects, capability enlargement to satisfy the rising demand for refrigerated show instances, and the notable improve so as backlog are anticipated to considerably enhance the corporate’s income within the close to to mid-term.

The corporate’s inventory is presently buying and selling at a major low cost to its historic ranges. And, contemplating the favorable outlook of the corporate and the valuation of the inventory, I’ve a purchase ranking on this inventory.

Enterprise Overview

LSI Industries is a outstanding firm that focuses on producing lighting and retail show options for the non-residential sector. The corporate operates by way of two segments, Lighting Phase and Show Options section, with the Lighting section being the most important with 57% of the entire gross sales as of the primary quarter of 2023. Within the Lighting section, the corporate provides a variety of LED fixtures, together with cover lighting, space lighting, architectural lighting, floodlighting, and a wide range of Lighting management to help lighting. LYTS’s Lighting Options are particularly designed to satisfy the distinctive want of companies, places of work, retail shops, QSRs (Fast Service Eating places), Industrial services, Parking tons, and Sports activities complexes.

As well as, LYTS supplies Retail show options below its Show options section that helps companies improve their model presence and create visually interesting experiences for his or her prospects. The section’s choices embrace Digital Signage, LED Shows, Menu board, and different Graphics options tailor-made to satisfy the particular necessities of the Retail trade.

Final Quarter Efficiency

Within the third quarter of 2023, the Lighting section offers one other robust quarter with income progress of 17% Y/Y to $66.7 million as the corporate continues to make progress out there, growing gross sales in all main verticals. The first issue for the robust Lighting section progress was strong gross sales of indoor lighting which grew 29% Y/Y, as the corporate continued to strengthen its capabilities for indoor functions. The robust progress within the Lighting section greater than offset the adverse influence from the Show Options Phase, which noticed a Y/Y decline of 4%, as a consequence of decreased digital Signage shipments. This coupled with the profit from ongoing stabilization and reliability within the provide chain resulted in total income progress of 6.7% to $117.5 million within the third quarter of 2023 as in comparison with the prior-year quarter.

The corporate’s margin then again expanded within the third quarter of 2023, with robust Adjusted EBITDA progress throughout each the section, which helped in 190 bps Y/Y Adjusted EBITDA margin progress to 9.6% throughout the third quarter of 2023. This progress was pushed by improved program pricing, favorable program combine, and quantity progress within the Lighting section greater than offsetting the adverse influence of upper SG&A bills.

Product innovation and footprint enlargement

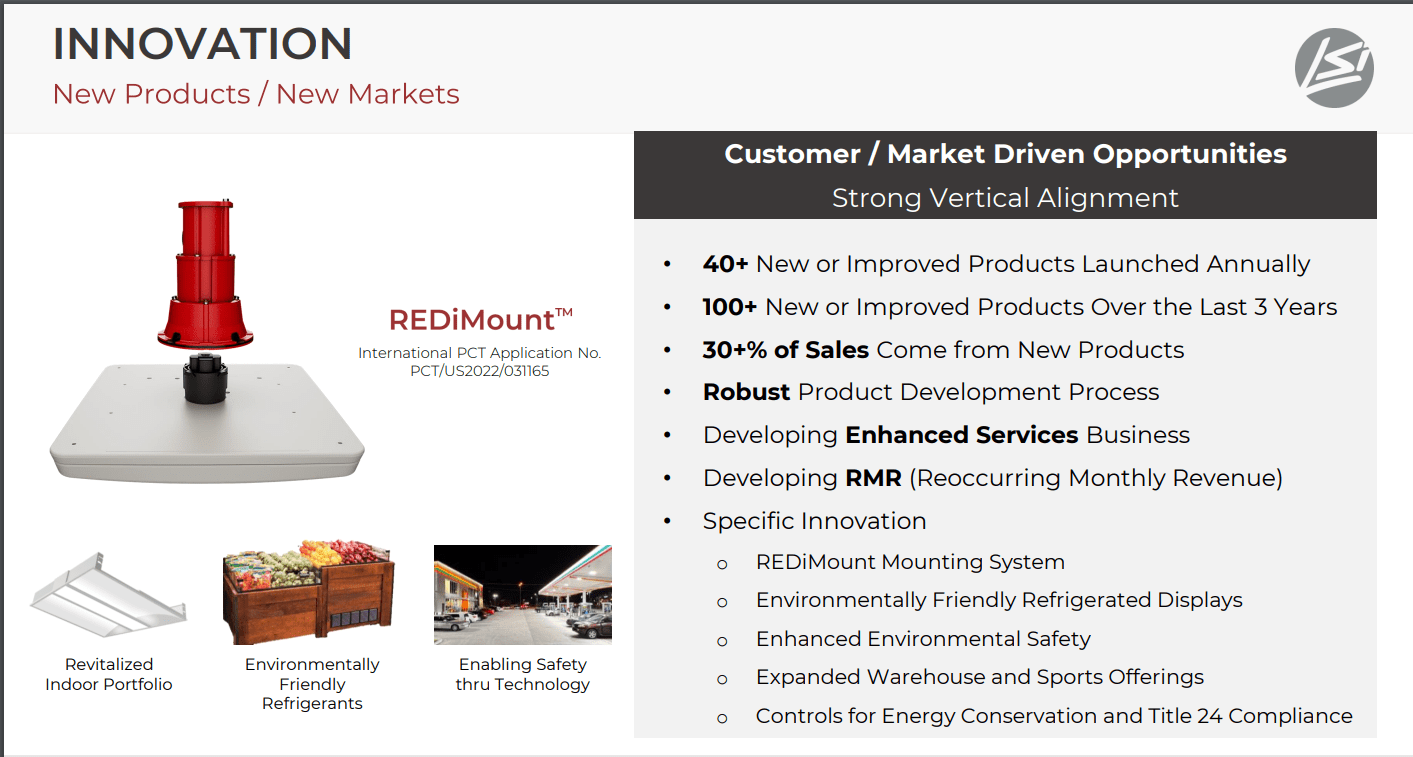

Over the previous few years, the corporate has persistently achieved strong efficiency, largely attributed to the success of its New Merchandise and Innovation initiatives, which stay a elementary driver for its total success. Constructing upon the optimistic outcomes skilled in earlier years, the corporate is additional reinforcing its dedication to steady funding in new merchandise and in new markets.

Throughout the preliminary half of 2023, the corporate efficiently launched its new product referred to as REDI-Mount. This revolutionary mounting answer streamlines the set up of cover lighting, lowering set up time by a outstanding 50%. The introduction of this product is predicted to be instrumental in attracting new prospects for the corporate within the upcoming quarters. Moreover, the corporate has not too long ago introduced a major funding within the Show Answer Group, demonstrating its dedication to this section’s progress and the potential it holds for additional alternatives.

LYTS product innovation (LYTS’s investor presentation)

The corporate is presently increasing its presence within the refrigerated shows group by incorporating a further 65,000 sq. toes of producing and analysis and growth house. This enlargement is geared in direction of enhancing our capability and capabilities to ship next-generation refrigerated options, together with the introduction of an R-290-based product, which is an environment-friendly non-toxic propane-based gasoline refrigerant having zero ozone-depleting properties. Moreover, as the corporate continues to aggressively pursue progress initiatives in Show Options, it has additionally introduced the lease of further manufacturing house, offering further capability to help ongoing market demand for refrigerated show instances, which ought to profit the corporate’s income within the coming quarters.

How ought to LSI industries carry out within the close to time period?

Along with the anticipated income progress ensuing from ongoing product innovation and capability enlargement, different components must also contribute positively to its income within the upcoming quarters. Within the final quarter, the corporate has been chosen as a lighting partner for an Electrical Automobile (EV) battery manufacturing facility in Kentucky, and the corporate’s LED lighting answer can be utilized in illuminating the manufacturing facility and workplace house of the multi-billion greenback EV battery Advanced, which ought to enhance the corporate’s sale within the coming quarters.

Whereas the corporate has historically held a powerful place in out of doors functions, it has been actively strengthening its capabilities in indoor functions as effectively. This strategic concentrate on indoor options has confirmed useful for the corporate’s income in latest quarters, additional solidifying its total place with prospects. As the combination between indoor and out of doors functions reaches a 50-50 split, the rising share of indoor functions, coupled with robust momentum on this enterprise, is predicted to offer important help in driving gross sales for the corporate.

The corporate has skilled a notable improve in its order backlog, primarily as a consequence of provide chain constraints in particular finish markets, resulting in a protracted quote-to-order conversion interval. Nonetheless, the continuing provide chain stabilization is predicted to assist the corporate scale back this conversion interval, in the end benefiting the corporate’s income by way of improved backlog-to-sales conversion within the upcoming quarters.

Total, I imagine that the wholesome citation exercise for the lighting options of the corporate together with the strong momentum within the indoor software ought to proceed to help the corporate income within the close to time period. This together with robust order backlog ranges and a latest win with a big EV battery manufacturing plant ought to additional drive the corporate’s prime line within the close to to mid-term.

Danger

As of the top of the fiscal 12 months 2022, the corporate reported a considerable order backlog totaling $112.4 million. This backlog was initially scheduled for cargo throughout the upcoming 12-month interval. Nonetheless, the corporate confronted challenges with its provide chain, resulting in a protracted conversion interval from backlog to precise gross sales which resulted in an additional rise in backlog ranges within the subsequent quarters.

In my thesis, I emphasize the significance of the backlog-to-sales conversion price on income progress, as the continuing stabilization within the provide chain ought to positively affect this conversion interval, leading to improved gross sales efficiency. Nonetheless, if the provision chain constraints persist within the upcoming quarters, the corporate could encounter important headwinds, primarily attributed to delayed backlog conversion. This, in flip, may have an antagonistic influence on the corporate’s income within the coming quarters.

Valuation and Conclusion

LYTS is presently buying and selling at 16.47x FY2023 consensus EPS estimates of $0.76 and 13.71x FY2024 consensus EPS estimates of $0.92, which represents a major low cost in direction of its 5-year common P/E of 42.33x. The continued citation exercise within the Lighting section and the introduction of recent merchandise ought to proceed to profit the corporate’s income. Whereas the robust backlog ranges, challenge wins and robust rising indoor software enterprise ought to additional gasoline the corporate’s prime line within the coming quarters. The corporate’s progress prospects look promising to me and contemplating the discounted valuation of the inventory, I’ve a purchase ranking on this inventory.

{kind=link}