onurdongel

Earnings season amps into full swing this week with many large names issuing Q2 outcomes. Up to now, in line with FactSet, 80% of S&P 500 have topped analysts’ earnings expectations, although simply 6% of the SPX’s market cap has reported. One identify I used to be bullish on final yr points its Q1 2024 figures subsequent week.

After not analyzing the identify for a lot of months, I reiterate a purchase score on Flex Ltd. (NASDAQ:FLEX) for its still-strong valuation and sturdy technical developments.

Earnings Season In Full Swing

Wall Avenue Horizon

In keeping with Financial institution of America International Analysis, FLEX is a world supplier of vertically built-in provide chain companies ranging from PCB fabrication, design, engineering, and manufacturing companies via after-sales help. The core enterprise consists of the Reliability Options and Agility Options segments.

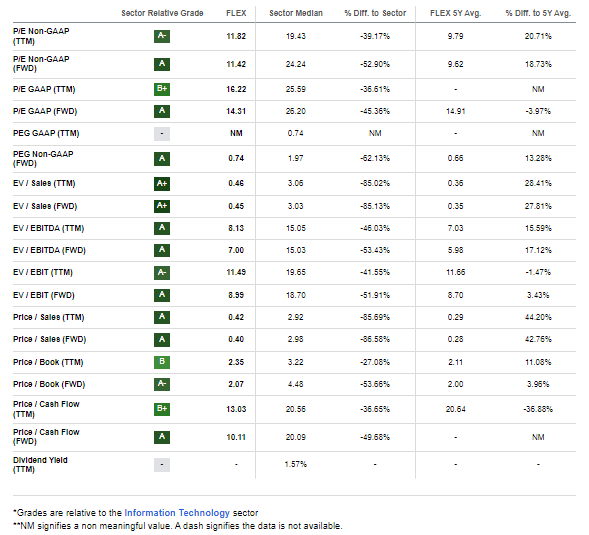

The Singapore-based $12.4 billion market cap Digital Manufacturing Companies business firm throughout the Info Expertise sector trades at a barely modest 16.2 trailing 12-month GAAP price-to-earnings ratio and doesn’t pay a dividend, in line with Looking for Alpha. Forward of earnings on the 26th, FLEX incorporates a reasonable implied volatility studying of 29% and the inventory has a low 1.7% brief curiosity share.

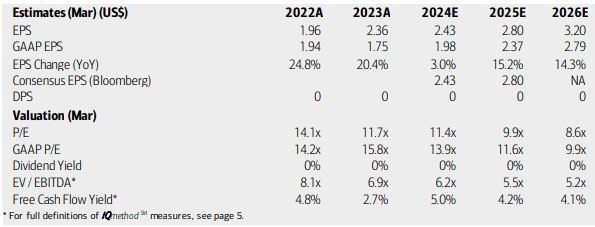

Again in Might, the corporate issued robust This fall 2023 results. EPS verified at $0.57 which topped estimates of $0.51. Income additionally got here in strong at $7.5 billion, a 9% bounce from the identical interval a yr earlier. The administration staff supplied steering for the quarter that simply completed – they anticipated Q1 2024 income within the $7 to $7.5 billion vary and adjusted EPS between $0.47 and $0.53.

Its full-year steering was notably spectacular, implying wholesome incremental margin enchancment pushed by secular development developments, although its way of life and shopper gadgets segments could hold experiencing headwinds. Extra broadly, the corporate’s transition to a better margin mixture of finish markets together with constant free money move era and profitability stay compelling options.

On valuation, analysts at BofA see earnings climbing at a slow rate this yr (FY 2024) however per-share income are anticipated to speed up within the out yr. Furthermore, EPS could high $3 on an working foundation come 2026. The Bloomberg consensus outlook is on par with the BofA tasks. Even with first rate and regular free money move, no dividends are anticipated to be paid on this tech inventory. Nonetheless, with low-teen non-GAAP P/E multiples and a PEG ratio properly under 1, I proceed to love the valuation state of affairs.

FLEX: Valuation, Earnings, Free Money Circulate Forecasts

BofA International Analysis

With an EV/EBITDA ratio that’s lower than half that of the broad market, if we merely apply a 16 P/E (barely lower than the sector median given modestly softer EPS development charges assumed), then the inventory needs to be close to $40 if we assume $2.50 of next-12-month per-share income. Thus, the inventory continues to sport worth.

FLEX: Spectacular Valuation Metrics, A Sturdy GARP Play

Looking for Alpha

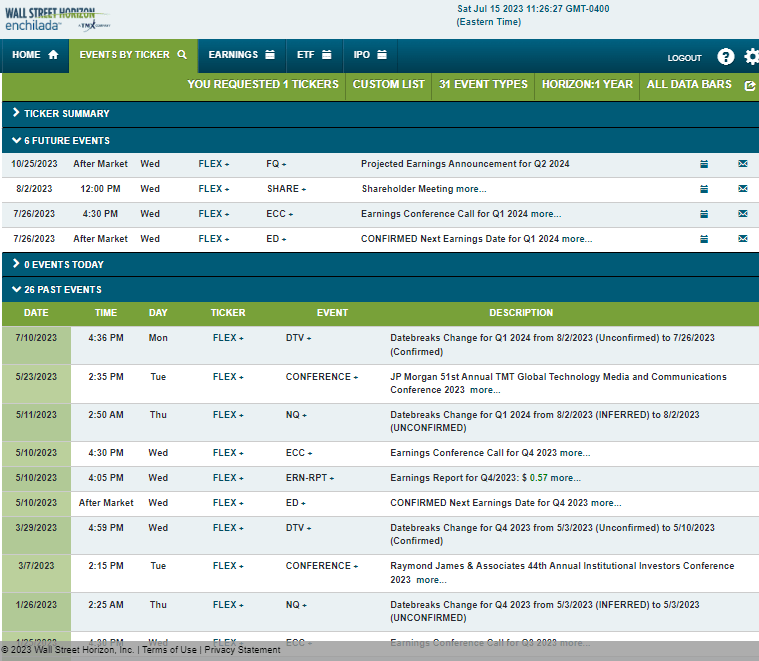

Trying forward, company occasion information from Wall Avenue Horizon reveals a confirmed Q1 2024 earnings date of Wednesday, July 26 AMC with a convention name instantly after outcomes hit the tape. You’ll be able to listen live here. Potential volatility doesn’t finish there, although. The agency holds its annual shareholders’ assembly on Wednesday, August 2.

Company Occasion Threat Calendar

Wall Avenue Horizon

The Technical Take

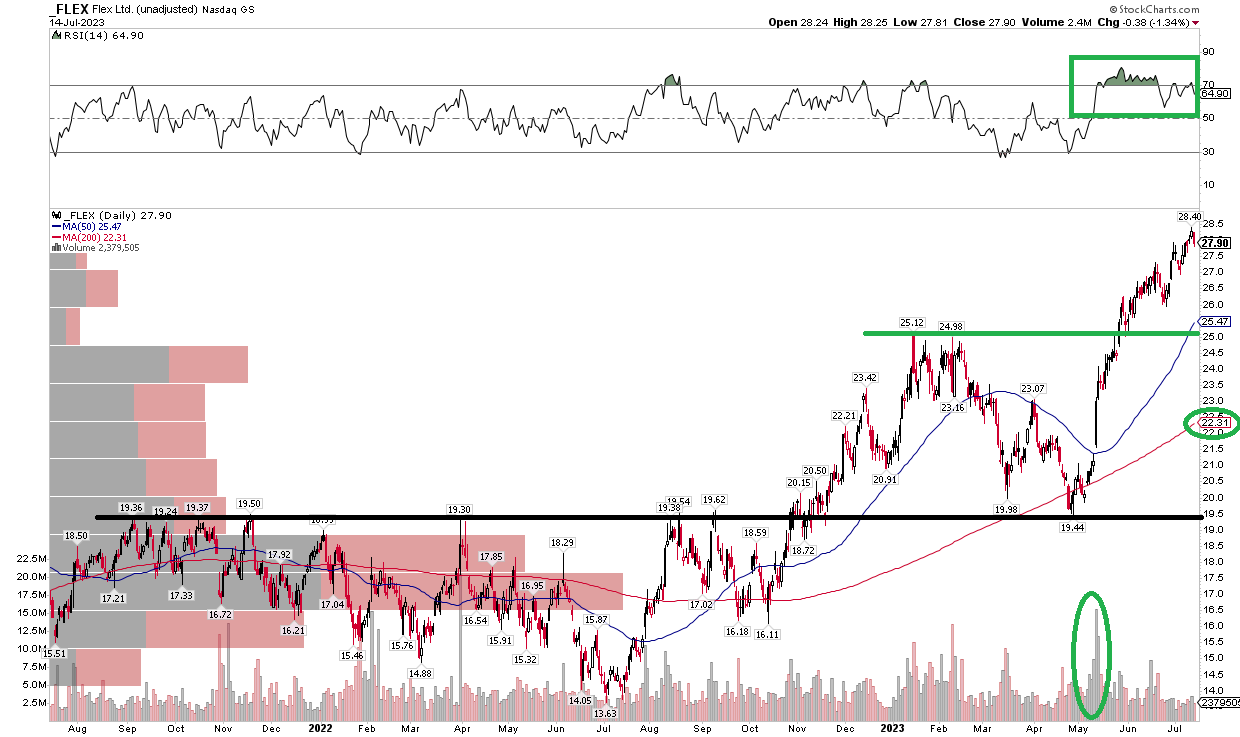

With a strong development trajectory past this yr, a compelling valuation, and earnings on faucet, how does the chart look? Discover within the graph under that FLEX has executed all the suitable issues in my opinion. Shares broke out from a consolidation vary in late 2022. The rally paused close to $25, nevertheless it was not trigger for panic as FLEX merely went on to retest noted support at $20.

After probing, however holding the 2021-22 vary highs, FLEX took off. Simply earlier this month, $28.40 was touched, marking a virtually 50% rally off the early Might nadir. At this time, the long-term 200-day transferring common is upward-sloping and the near-term pattern is clearly greater, as gauged by the 50-day transferring common. There may be some minor bearish divergence within the RSI momentum indicator on the high of the chart, however general, the RSI studying continues to hover within the bullish 40 to 90 zone.

Lengthy right here with a cease underneath the Q1 highs is sensible. Longer-term buyers might additionally think about putting a promote cease additional down, underneath the December 2022 and April 2023 peaks round $23.

FLEX: Bullish Uptrend, Eyeing $25 Assist

Stockcharts.com

The Backside Line

I reiterate my purchase score on FLEX inventory. I see truthful worth close to $40 whereas the technical pattern is bullish and momentum is powerful.

{kind=link}