Maddie Meyer

Funding thesis

Our present funding thesis is:

- CAKE is a well-positioned enterprise as a result of its enticing business profile, providing customers a singular eating expertise that’s resilient in opposition to altering business dynamics.

- Progress has been robust, with the expectation for this to proceed as new places are opened and customers proceed to take pleasure in its service.

- Margins are problematic however enchancment seems to be probably. CAKE is at the moment underperforming its friends and based mostly on its relative valuation, doesn’t recommend upside.

Firm description

The Cheesecake Manufacturing facility (NASDAQ:CAKE) is a famend American restaurant firm identified for its in depth menu, together with all kinds of appetizers, entrees, and, after all, delectable cheesecakes. The corporate operates over 200 eating places throughout america and internationally.

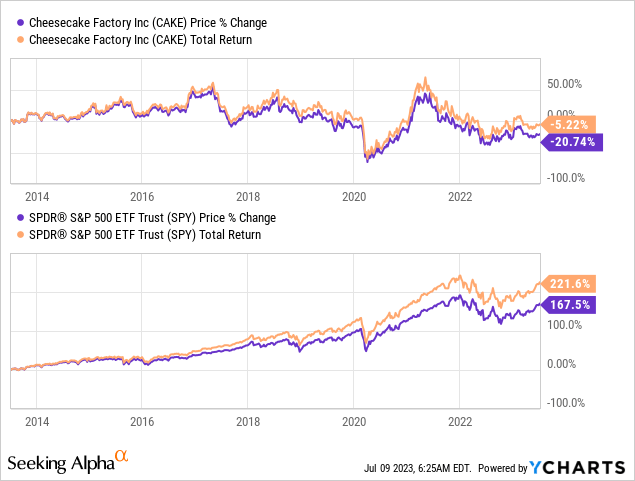

Share worth

CAKE’s share worth has considerably underperformed the market, partially because of the affect of Covid-19 but additionally because of its delicate efficiency so far. The corporate has struggled to realize constant enchancment regardless of rising scale.

Monetary evaluation

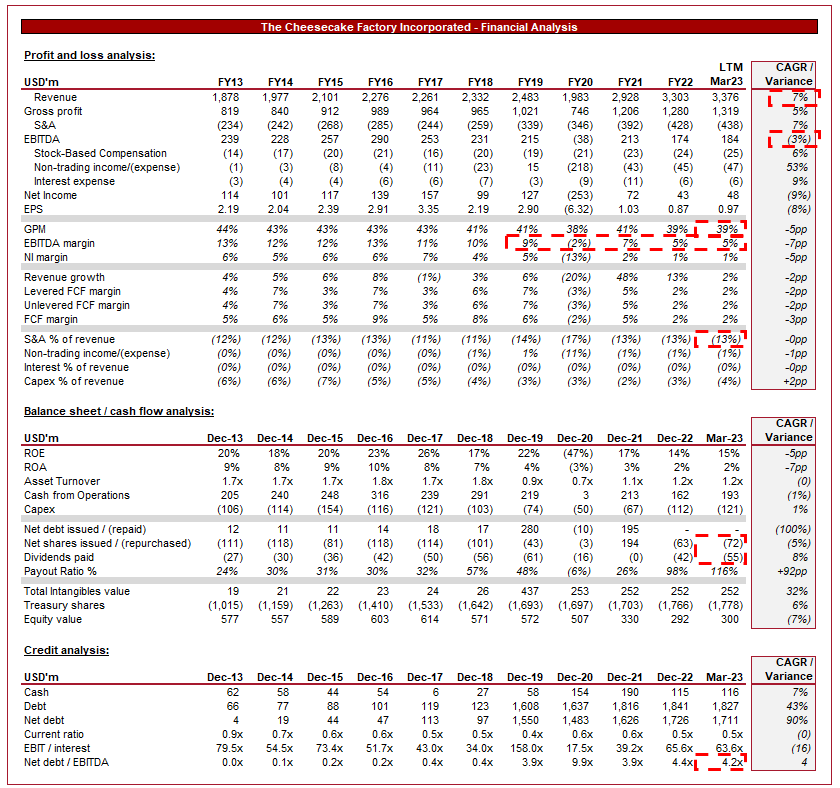

CAKE’s financials (Capital IQ)

Introduced above is CAKE’s monetary efficiency for the final decade.

Income & Industrial Components

CAKE’s income has grown at a CAGR of seven% within the final 10 years, a decent achievement given the extent of competitors available in the market. In the course of the historic interval, progress has been comparatively constant, with solely a single interval of adverse progress (excl. Covid-19), reflecting this optimistic trajectory.

Enterprise Mannequin

CAKE presents an expansive menu with a deal with high-quality elements, scratch-made recipes, and culinary creativity. That is a part of the corporate’s goal to offer visitors with a memorable eating expertise, at the side of its distinctive restaurant ambiance, attentive service, and a spotlight to element. This differentiates the enterprise from lots of its friends at an identical worth level, who primarily deal with delicacies fairly than environment and setting. CAKE is ready to effectively present customers with each, representing a lovely eating expertise.

CAKE usually introduces new menu gadgets and seasonal choices to cater to evolving shopper tastes and preferences. It is a rising pattern amongst different eating places as they lastly notice the advantage of such a technique. This encourages recurring attendance whereas additionally broadening its attain to informal customers purchasing round.

Given the scale of its menu and places, the corporate emphasizes environment friendly restaurant operations, together with standardized processes, stock administration, and workers coaching. This enables the enterprise to take care of constant high quality and management prices, permitting it to maximise the expertise supplied to customers.

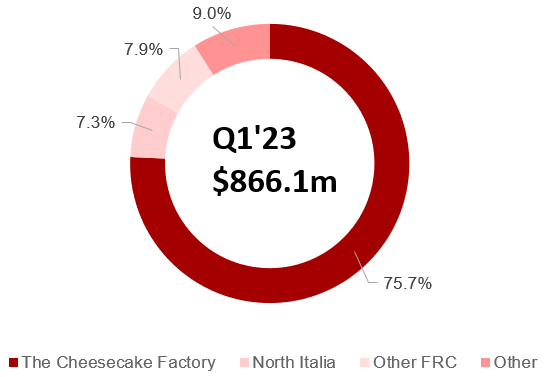

Along with The Cheesecake Manufacturing facility, CAKE has diversified its model portfolio by way of the acquisition of North Italia and Fox Restaurant Ideas, in addition to working different ideas equivalent to Grand Lux Cafe, RockSugar Southeast Asian Kitchen, and Social Monk Asian Kitchen. Income is primarily generated from The Cheesecake Manufacturing facility, however this supplies some diversification advantages.

Income cut up (CAKE)

Footprint enlargement represents a key alternative of driving progress within the coming years. Administration is planning to open 20-22 eating places in FY23, with 2-3 abroad. Given the comparatively small variety of places, particularly abroad, we consider there’s adequate runway to proceed to drive progress by way of this technique.

Aggressive Positioning

We consider CAKE’s aggressive benefit stems from the expertise it supplies to customers. With an unlimited menu and culinary experience, the corporate is ready to set itself aside from opponents. Additional, its deal with offering an fulfilling and distinctive eating expertise contributes to buyer loyalty and repeat visits, because the expertise is taken into account fulfilling past simply good meals.

Restaurant Business

Rivals within the eating business differentiate themselves based mostly on menu choices (delicacies), worth factors, customer support, and restaurant ambiance. CAKE faces competitors from informal eating chains like Olive Backyard (DRI), Outback Steakhouse (BLMN), Chili’s (EAT), Texas Roadhouse (TXRH), Chipotle (CMG), and Shake Shack (SHAK), in addition to native and regional restaurant operators.

The restaurant business is extremely aggressive, with new entrants and present gamers vying for market share. This has contributed to a level of harmonization within the business, with companies working with an identical strategy across the few most profitable cuisines within the US. That is the place CAKE differentiates itself we consider, as it’s able to severing a number of cuisines at a high-quality, whereas additionally specializing in differentiating its restaurant expertise.

Rising shopper demand for more healthy meals decisions is forcing eating places to innovate, in search of the inclusion of high-quality and attractive meals choices which are lighter, plant-based, and gluten-free. This leans completely into CAKE’s giant menu strategy, permitting the enterprise to seamlessly adapt and proceed to enchantment to a big buyer base.

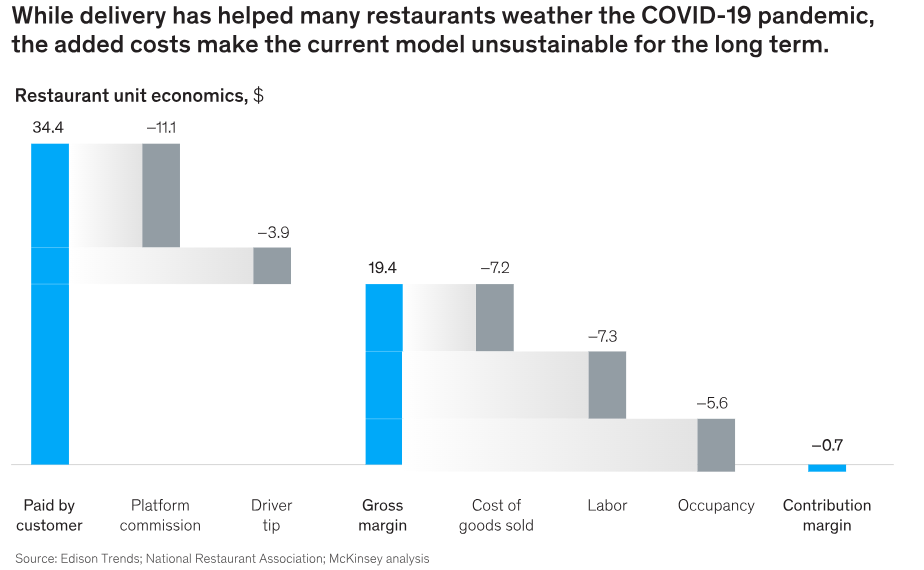

The rise of on-line meals supply platforms because of the worth supplied by comfort has materially disrupted the restaurant business. This has contributed to fewer customers in search of out eating places, as they don’t consider there’s adequate worth supplied to eat in-store. The priority with that is that the economics from supply gross sales are far decrease than in-store, destroying worth (as the next illustrates).

Restaurant economics (McKinsey / Edison Developments / Nationwide Restaurant Affiliation)

We consider CAKE is positioned properly to take care of robust attendance because of the expertise supplied, however it’s nonetheless dealing with points with responding to this improvement. We consider this may act as a downward strain on margins, whereas the elevated competitors as a result of extra choices may additionally affect demand.

Financial & Exterior Consideration

Present financial situations signify a short-term threat to the enterprise, as excessive inflation and elevated charges encourage customers to tighten funds, decreasing discretionary spending.

Based on a research analyst at Datassential, “I believe operators are nonetheless longing for a great summer time boon in foot site visitors and gross sales … however I believe on the patron aspect, they’re extra hesitant”

Up to now, CAKE has remained strong, with YoY progress of 9%, 6% of which was comparable progress. This suggests resiliency so far, though we proceed to stay hesitant.

Margins

CAKE’s margins are a transparent weak spot for the enterprise, with an EBITDA-M of 5% and a NIM of 1%. That is considerably under its pre-Covid degree, the place the enterprise boasted an EBITDA-M of 10-12%.

The margin discount is a mirrored image of inflationary pressures, with the price of meals and wage inflation materially impacting the enterprise. It is a reflection of why many giant restaurant chains select to franchise, as they will export the operational threat. Margins are bettering, with OPM rising by 0.3ppts YoY, nonetheless, the progress is sluggish. The priority is that CAKE can be unable to sufficiently win again margins as price pressures subside.

Steadiness sheet & money flows

CAKE’s ND/EBITDA ratio is at the moment 4.2x, a excessive degree however primarily regarding property leases. This degree has scope to extend with out concern, permitting the enterprise to fund the brand new places.

Though distributions have returned, they continue to be under the historic degree, reflecting weaker profitability.

Outlook

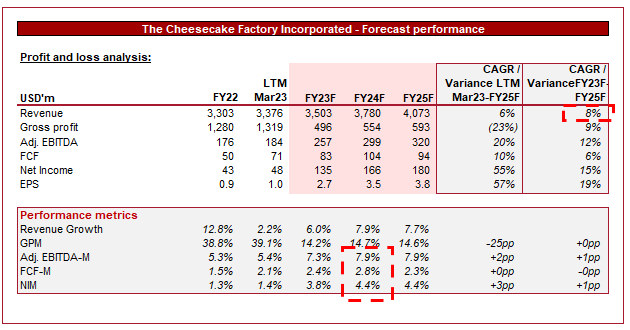

Outlook (Capital IQ)

Introduced above is Wall Avenue’s consensus view on the approaching 5 years.

Income is forecast to develop at an identical degree to traditionally achieved, with a mean charge of 8%. Given the business energy of the enterprise, this seems to be affordable.

Margins are forecast to enhance, though will seemingly normalize on the 7% degree. That is considerably under its prior degree. It is a affordable estimate given the developments so far.

Business evaluation

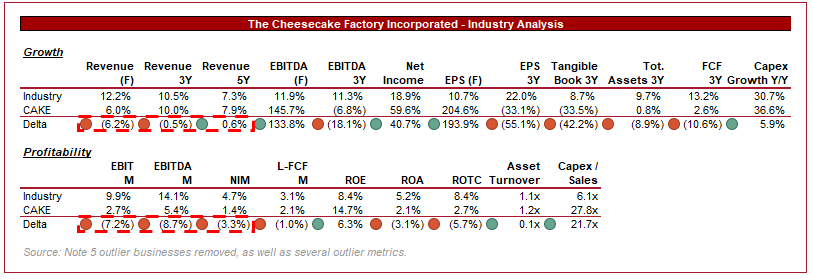

Restaurant business (Looking for Alpha)

Introduced above is a comparability of CAKE’s progress and profitability to the common of its business, as outlined by Looking for Alpha (38 firms).

CAKE’s income progress is akin to the business, implying it has responded to the Covid-19 pandemic in step with the business common. This mentioned, the expectation is for progress to materially underperform within the coming 12 months. That is probably a mirrored image of decreased restaurant attendance as financial situations chew.

Margins-wise, CAKE considerably underperforms. It is a reflection of the prevalence of its bigger franchising friends, who’re in a position to function with lean operations. This mentioned, the corporate is comparable on an effectivity foundation, assuming a great allocation of sources (and returns per restaurant).

Based mostly on this, we consider CAKE ought to commerce at a reduction to its peer group, not less than 20%, reflecting its considerably weaker money circulate conversion.

Valuation

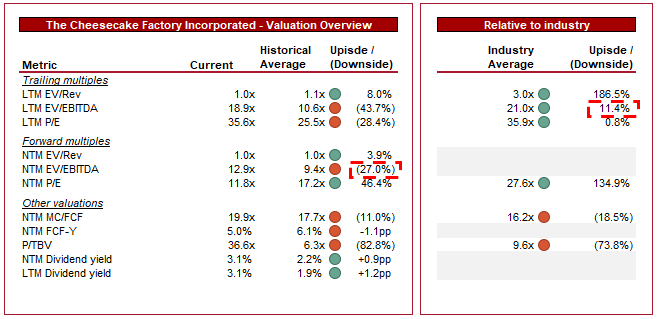

Valuation (Capital IQ)

CAKE is at the moment buying and selling at 19x LTM EBITDA and 13x NTM EBITDA. It is a premium to its historic common.

A premium to CAKE’s historic common seems to be fully unjustified as, regardless of its business energy, the corporate is financially weaker than its pre-pandemic place. This premium is probably going a mirrored image of traders pricing in margin enchancment within the coming years, probably past the extent forecast by Analysts.

Relative to its peer group, CAKE is buying and selling at an LTM low cost of 11% and a NTM FCF premium of 20%. This suggests its weak spot is considerably priced in, however traders are fairly bullish on the advance within the coming 18-36 months.

Total, we consider a lot of the upside is probably going priced in as CAKE is buying and selling at a slight premium to our anticipated honest worth vary.

Remaining ideas

CAKE is a commercially spectacular enterprise in our view. The corporate has achieved diversification from its comparable restaurant friends, providing customers a holistic restaurant expertise. The business is dealing with each tailwinds and headwinds, which we consider CAKE is positioned properly to navigate. The most important problem with the enterprise is margins and it is at the moment unsure the place these will land within the coming years.

CAKE’s valuation at the moment costs within the enchancment we predict and so we charge the inventory a maintain till we’ve additional visibility on margins.

{kind=link}