Sean Gallup/Getty Photographs Information

Introduction

In 2022, the power market confronted quite a few challenges. The battle in Ukraine, coupled with a scarcity of funding within the power sector since 2014, led to a big improve in power costs. Consequently, governments intensified their efforts to prioritize power safety. One notable consequence was the scarcity of gasoline provides in Europe on account of decreased imports from Russia, which resulted in a shift in the direction of coal utilization and subsequently larger coal costs. Moreover, there was a considerable surge in demand for liquefied pure gasoline (LNG) from Europe, with roughly 60% larger demand in comparison with earlier years. This elevated demand is anticipated to proceed all through 2023.Golar LNG (NASDAQ:GLNG), recognizing the altering dynamics of the LNG transport market, made strategic strikes to adapt. They exited the LNG transport market and subsequently bought their remaining Floating Storage and Regas Models (FSRU) to SNAM, an Italian infrastructure firm. Because of this, Golar LNG shifted its focus in the direction of FLNG operations. By being concerned in delivering floating options that produce LNG, Golar LNG has positioned itself to capitalize on alternatives that come up as a everlasting resolution for European power safety is wanted.

Golar enterprise construction

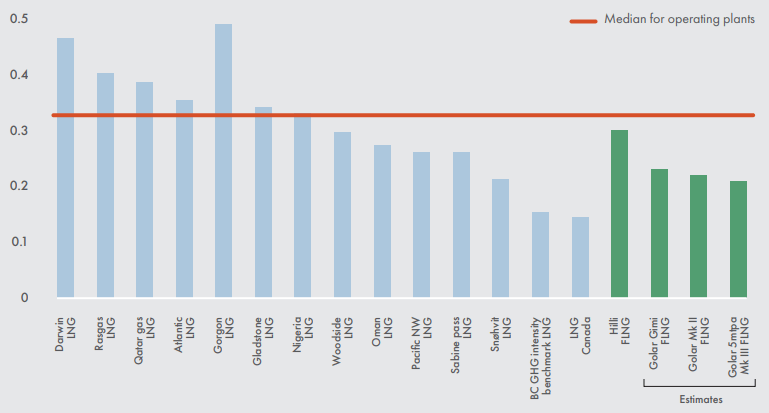

By the top of 2022, Golar FLNG Hilli skilled a big improve in LNG manufacturing, with 50% of its cargoes being delivered to Europe. Moreover, the FLNG Golar Gimi challenge is about to contribute extra LNG to the market, which is focused to sail within the third quarter of 2023. Golar has achieved notable milestones, together with the event of the world’s first Floating Storage Regasification Unit (FSRU) and Floating Liquefied Pure Gasoline unit (FLNG). These improvements have allowed new markets to entry cleaner power sources by means of FSRUs and enabled the seize and monetization of related gasoline assets by means of FLNGs. It’s value mentioning that these options have resulted in one of many lowest carbon footprints relative to their dimension. Figure 1 illustrates that Golar Hilli FLNG, Gimi, Mk II, and Mk III are estimated to have considerably decrease carbon footprints in comparison with working vegetation’ median values, whereas Darwin LNG and Gorgon LNG exhibit the best carbon footprints.

Determine 1 – Golar’s options have the bottom carbon footprints for his or her dimension

2022 ESG report

Throughout the first quarter of 2023, Golar efficiently repurchased New Fortress Vitality’s (NFE) curiosity within the FLNG Hilli, leading to an annual improve of $70 million in Distributable Adjusted EBITDA till 2026. Nonetheless, Golar skilled a decline in Distributable Adjusted EBITDA from FLNG Hilli, dropping from $114 million on the finish of 2022 to $94 million in 1Q 2023 on account of decrease Brent oil and Dutch Title Switch Facility (TTF). Along with this, Golar has entered right into a Memorandum of Understanding (MOU) with NNPC, the most important oil producer in Nigeria. NNPC has a strategic plan to develop Nigeria’s gasoline exports and is presently a big participant in Africa’s gasoline and LNG market. Nigeria is producing 33 million tons of LNG, whereas exporting 23.3 million tons. Because of this, collaborating with NNPC on a challenge might deliver quite a few monetary advantages for Golar. Moreover, Golar has made a sale and acquisition that can contribute to value effectivity. The corporate bought the older vessel Gandria from 1977 and bought the newer vessel Fuji from 2004. This acquisition not solely reduces re-conditioning prices but in addition gives elevated capability and bigger deck area on Fuji, resulting in improved effectivity and suppleness for Golar.

Golar’s financials

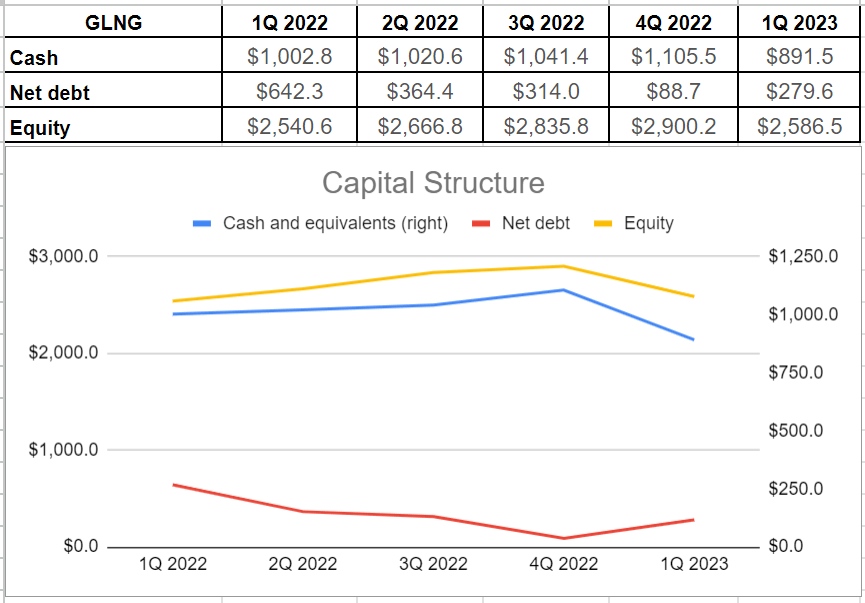

Golar’s money era within the first quarter was roughly $891.5 million, which was decrease than the $1 billion recorded in the identical quarter of 2022. Albeit if we embrace $113 million of restricted money, it could be roughly $1 billion. This decline could be attributed to decrease commodity costs in comparison with the earlier yr. Nonetheless, the corporate managed to cut back its internet debt stage by round 56%, reaching $279.6 million in 1Q yr over yr, in comparison with $642.3 million in 1Q 2022. It’s value noting that Golar’s debt stage is considerably decrease than its fairness stage of over $2.5 billion. Moreover, Golar achieved different notable milestones similar to acquiring credit score approval for paying off their current Hilli deb facility and repurchasing $20 million value of Unsecured Bonds maturing in 2025. These accomplishments will strengthen the corporate’s stability sheet and improve their monetary flexibility (see Determine 3).

Determine 3 – GLNG’s capital construction (in hundreds of thousands)

Writer

Moreover, Golar’s money situation has considerably improved in comparison with the identical quarter of 2022. The corporate achieved roughly $59.8 million in working money movement, whereas incurring $26 million in capital expenditures. Consequently, they have been capable of generate $33.6 million in free money movement, which is a exceptional accomplishment when in comparison with the adverse free money outflow of $40 million in 1Q 2022. The generated free money movement is ample to cowl their dividend cost of $0.25 per share for the excellent variety of 107,400,000 widespread shares, leading to a complete dividend cost of $26.85 million (see Determine 4).

Determine 4 – GLNG’s money construction (in hundreds of thousands)

Writer

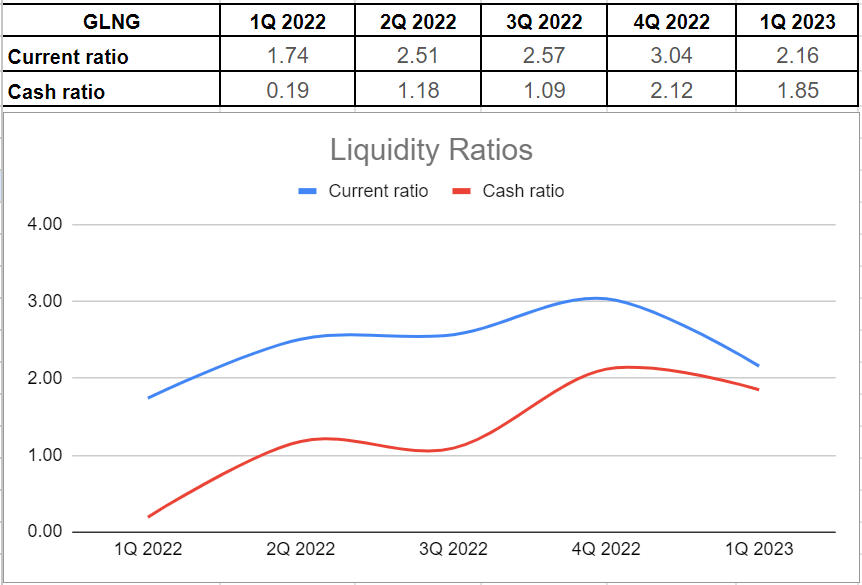

In my earlier article on Golar LNG, I analyzed the corporate’s leverage situation and demonstrated that its low leverage ratios point out robust solvency and the power to satisfy present and future obligations. On this article, I’ve examined the corporate’s liquidity situation throughout the board of its present and money ratios. Determine 5 illustrates that Golar LNG has achieved a strong and improved liquidity place within the latest quarter in comparison with the identical interval in 2022. The present ratio for GLNG has elevated by 24%, rising from 1.74x in 1Q 2022 to 2.16x in 1Q 2023. Moreover, GLNG’s money ratio has proven a formidable surge, reaching 1.85x yr over yr, in comparison with simply 0.19x within the first quarter of 2022.

Determine 5 – GLNG’s liquidity situation

Writer

Market outlook

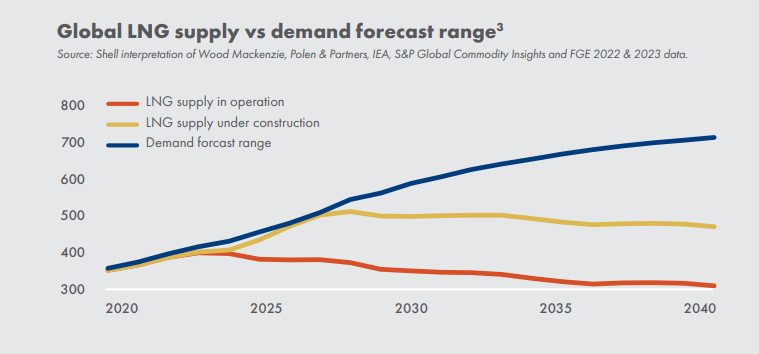

Whereas attaining the Paris Settlement purpose stays the final word goal, transitioning straight from coal and oil to renewables with out incorporating gasoline poses a number of challenges. These embrace the excessive value of vital supplies, restricted provide, manufacturing capability constraints, and storage points. Regardless of the rising demand for renewable energies, you will need to acknowledge that gasoline and LNG will proceed to play an important function within the power transition as roughly 81% of world power wants are met by hydrocarbons. It’s value mentioning that Golar has developed a platform that’s anticipated to supply business options for reworking diesel into gasoline/EV throughout the subsequent yr. If investments in clear power don’t speed up consistent with established insurance policies, an extra funding of practically $650 billion per yr till 2030 can be required in oil and gasoline to forestall additional value volatility. It represents over 50% improve versus latest years. The implementation of sturdy insurance policies selling pure gasoline utilization to mitigate air pollution and meet rising power calls for pushed by rising populations signifies that rising and creating markets in Asia are projected to import extra pure gasoline. Moreover, Europe goals to interchange Russian pipeline gasoline with LNG imports. S&P World estimates that international LNG demand will surge by 362 mtpa by 2040, surpassing current or presently beneath building provide capacities (see Determine 6).

Determine 6 –

2022 ESG report

Why I may be improper

The corporate’s outcomes of operations and monetary situation rely upon the demand for LNG and FLNGs. The demand for LNG and FLNGs could be negatively affected by varied components similar to geopolitical unrest, value, and availability of pure gasoline, crude oil, and petroleum merchandise, adjustments in the price of pure gasoline derived from LNG relative to the price of pure gasoline, inadequate or oversupply of pure gasoline liquefaction, and will increase within the manufacturing of pure gasoline in areas linked by pipelines to consuming areas. Thus, Golar LNG’s money era potential might lower in vital manner if the demand for LNG and FLNGs decreases as a result of talked about components. In such a situation, the corporate might not have the ability to get hold of new financing, meet its debt obligations, or pay dividends. You will need to know that even when Golar LNG might handle to flee from the adverse impact of the beforehand talked about political, macroeconomic, and microeconomic components, the power of sure events to fulfill their obligations to Golar LNG might lower, affecting the corporate’s monetary situation and outcomes of operations in a big manner.

Conclusion

Golar LNG has demonstrated robust efficiency within the first quarter of 2023. The corporate’s capital and money constructions are sturdy, and the administration’s efforts to boost their enterprise operations will present elevated monetary flexibility within the upcoming quarters. Moreover, GLNG’s liquidity situation is strong, supported by a good LNG market and profitable FLNG operations. Consequently, there may be potential for vital enhancements within the firm’s monetary outcomes over the subsequent few years. Based mostly on these components, I like to recommend a purchase score for GLNG inventory. I welcome your opinions.

{kind=link}