simonkr

Funding Abstract

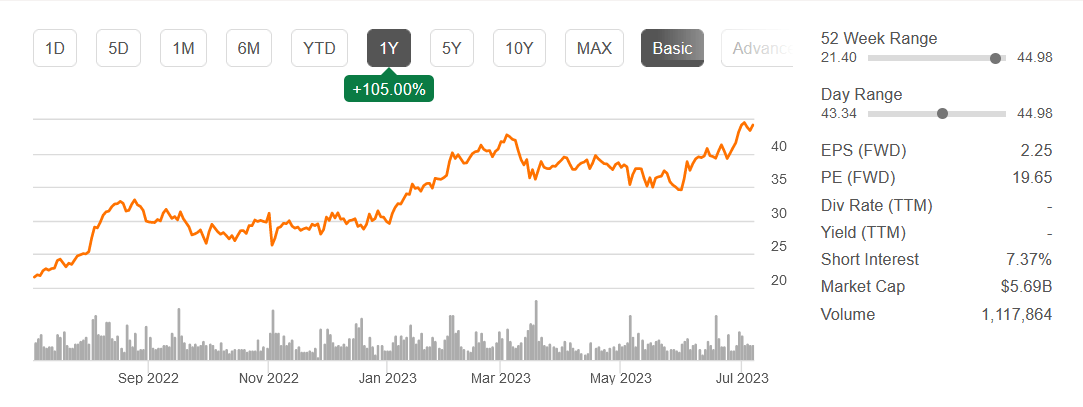

ATI Inc. (NYSE:ATI) is an organization that focuses on the manufacturing and promoting of specialty supplies and parts. The enterprise has been aligned in two completely different segments that make up the corporate, these being: Excessive-Efficiency Supplies & Parts (HPMC) and Superior Alloys & Options (AA&S). The market for supplies that ATI makes use of has been fairly risky and created a tough surroundings for a lot of corporations to function in. However the newest earnings report from them confirmed each resilience and development for the highest and backside strains. An EPS development of 109% YoY appears to have helped set off a rally for the inventory worth because it’s up over 100% within the final 12 months.

The place I’m barely nervous is that we are going to see a pullback within the worth as ATI is buying and selling a good bit above its historic common multiples just like the p/e, 31% above that. This presents extra draw back dangers for the share worth. In the long run, I’m moderately bullish on ATI because the reshoring of loads of manufacturing again to the US will probably be a key driver for development over the approaching many years. However I believe we may even see higher entry factors within the brief time period. Score ATI a maintain for now.

Manufacturing Returning And Bringing Demand With It

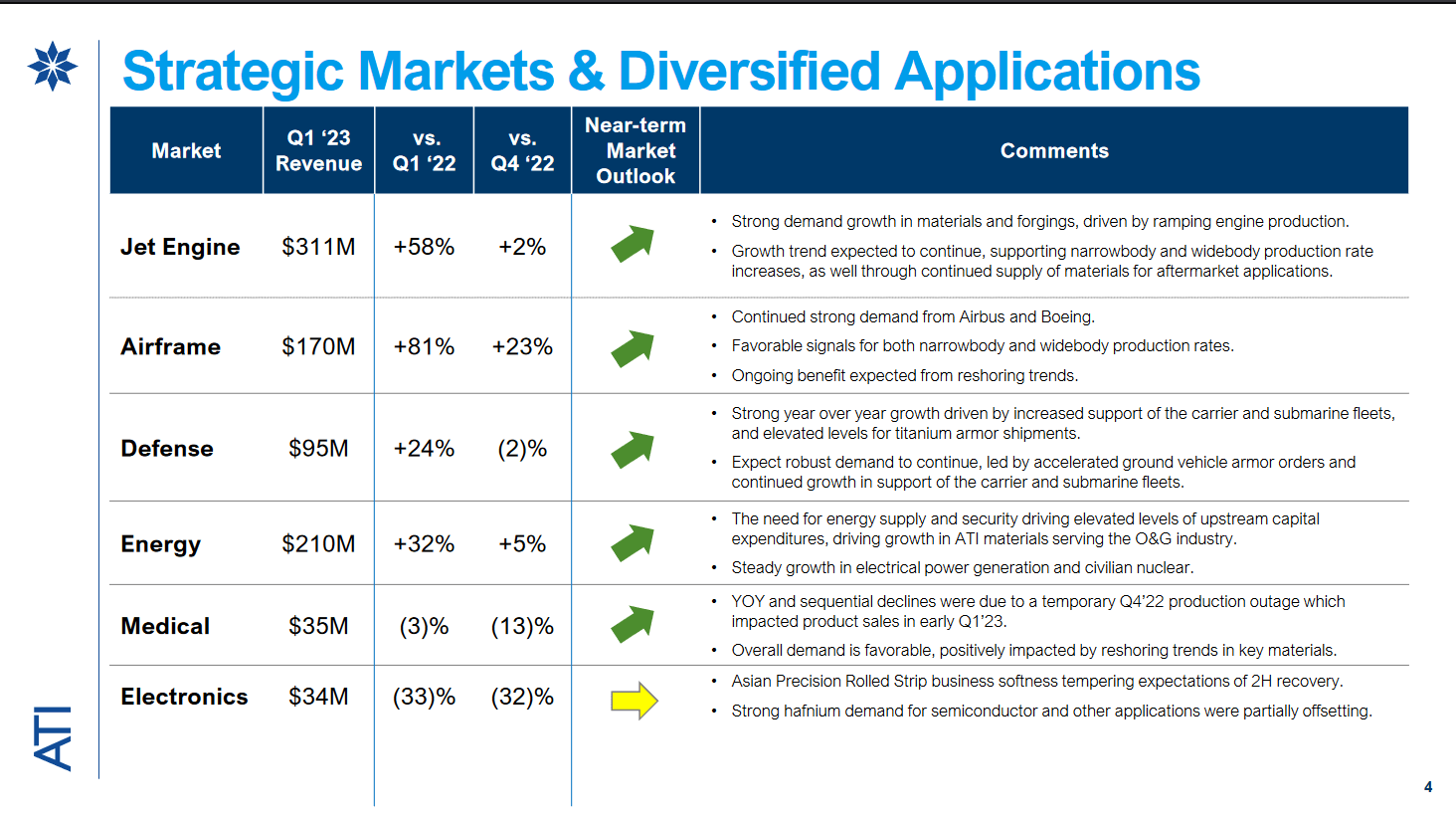

Among the key drivers for development within the coming years I believe would be the reshoring of loads of manufacturing to the US. As political tensions rise with China the Asia Pacific area as a complete turns into tough to function effectively for lots of companies. The enchantment to have manufacturing within the US turns into a lot larger and it nearly has a snowball impact with an increasing number of corporations establishing store there. However the US authorities can be creating incentives for this, just like the CHIPS Act in 2022, geared toward boosting the semiconductor capabilities of the nation and growing manufacturing. This can be a market that ATI has publicity to, but it surely would not make up a majority of its revenues, $34 million within the final quarter. It has additionally declined by 30 – 34% YoY however I believe tailwinds like these acts are going to show it round.

Key Markets (Earnings Presentation)

The first market that ATI serves is the aerospace market appears with $310 million in revenues generated from the “Jet Engine” market. Plainly the manufacturing of airplanes is growing in 2023 as touring is rebounding and corporations need to get forward of rising demand. I believe this will probably be a medium-term influence on the revenues generated right here, however the focus should be on different key markets which can be rising too. This can assist make sure that ATI has a really diversified set of income streams and hedge towards downturns, like a recession.

Quarterly Consequence

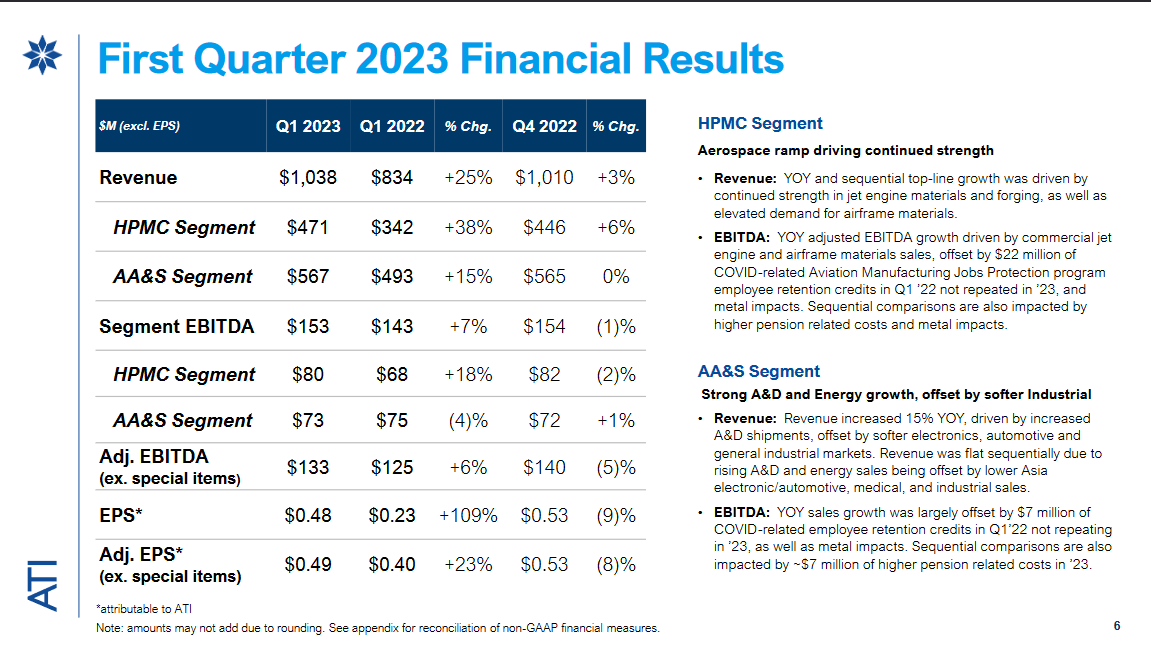

As I stated to start with a part of this text, the latest report from ATI was in my view a showcase of resilience and energy in a tough surroundings. The worth of many supplies has not come again to highs within the final 12 months, which had a optimistic influence on most of the revenues for corporations within the sector.

Q1 Outcomes (Earnings Presentation)

The primary quarter of 2023 had revenues develop 25% YoY advert the EPS grew by 109% YoY as nicely. The CEO Robert S. Wetherbee had some optimistic remarks on the quarter and stated the next: “Our transformation is optimizing the differentiated capabilities our clients worth. We’re well-positioned to seize development in our key markets”. I believe this highlights the significance that’s having a diversified set of markets that you simply serve. When one is struggling maybe one other one is doing very nicely. Over time this brings constant development for the corporate and that has in my view been seen right here with ATI.

2023 Steering (Earnings Presentation)

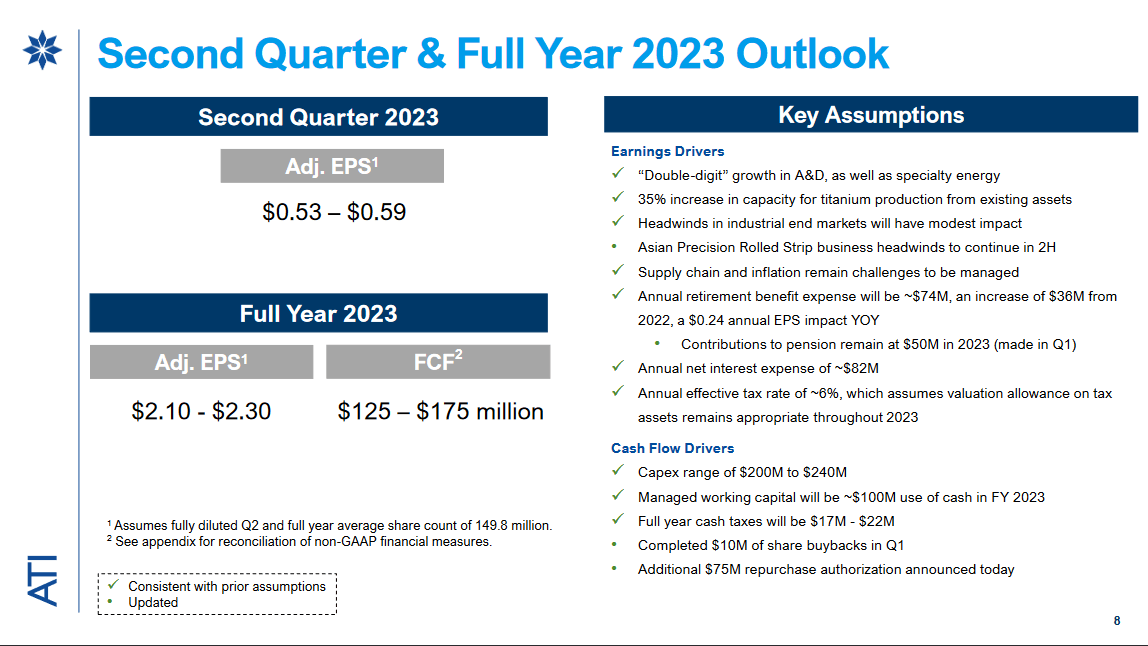

As for the outlook that ATI has for the remaining a part of 2023 it appears fairly optimistic. The adjusted EPS for Q2 is anticipated to land between $0.53 – $0.59, representing a QoQ development of 20% in the event that they obtain the upper finish of the steering. By way of 2023 as a complete, the adjusted EPS is estimated to be between $2.1 – $2.3 per share. This may worth at a 19x FWD earnings a number of. One thing which is a good bit above the sector’s common of 13 and in addition the historic a number of that ATI has been buying and selling at, 16. I believe this highlights among the dangers related to investing in ATI proper now. The corporate is rising at a robust fee, however above what may be thought-about honest worth. That interprets to ATI being just a little overvalued right here in my view. The approaching quarters might want to present margin growth and in my view extra development from markets which have in Q1 seen yearly decreases in revenues, like Medical and Electronics.

Dangers

The first threat proper now with ATI in my view is the excessive a number of its buying and selling at. I’m assured that the corporate will proceed to develop effectively as they’re experiencing stable demand from a number of key markets. However that does not mitigate the danger {that a} pullback in valuation to extra historic numbers would possibly occur.

Inventory Worth (Looking for Alpha)

Aside from that, I’m just a little nervous concerning the dilution that ATI is performing. Now, it must be stated it is not a major quantity every year, it is barely even 1%. However when the corporate is anticipated to generate between $125 – $175 million in FCF for 2023 I need to see a few of that capital used for purchasing again shares. The business that they’re in is crammed with corporations that carry out important buybacks, like United States Metal Company (X). The enchantment of investing in ATI I believe can be larger if they begin a program equivalent to this.

Wrap-Up

Proper now ATI is buying and selling above the sector’s multiples because the share worth has risen shortly within the final 12 months. The very optimistic development that was skilled in Q1 of 2023 for ATI appears to have been a key driver for this development. However I believe we’re more likely to see a pullback all the way down to extra cheap ranges like a 16 – 17 p/e. With extra draw back threat than I’m comfy with, I’m ranking ATI a maintain at these costs.

{kind=link}