Matteo Colombo

Introduction

It is time to dive into the State Avenue Company (NYSE:STT). Not solely did I get a variety of requests to evaluate this (considerably) high-yielding asset supervisor, however I additionally consider that taking a more in-depth have a look at this large tells us quite a bit concerning the present state of the business and potential funding alternatives down the street.

Whereas the inventory value efficiency has been fairly disappointing previously ten years, the inventory comes with a 3.4% dividend yield, constant dividend progress, and what appears to be a beautiful valuation.

On this article, we’ll have a look at the danger/reward via the lens of a dividend (progress) investor.

So, let’s get to it!

What Makes State Avenue So Particular

State Avenue is a big company. With a market cap of $25 billion, it’s one of many ten largest asset managers in North America.

Headquartered in Boston, Massachusetts, the corporate is a number one international supplier of economic providers to institutional traders. With subsidiaries working in over 100 markets worldwide, State Avenue provides a variety of economic services and products to institutional traders, together with asset managers and homeowners, insurance coverage corporations, official establishments, and central banks.

To present you some numbers, as of December 31, 2022, the corporate had $36.74 trillion in property below custody/administration (“AUC/A”) and $3.48 trillion in property below administration (“AUM”).

State Avenue Company had consolidated whole property of $301.45 billion, whole deposits of $235.46 billion, and greater than 42,000 staff to handle all of it.

The corporate has two main enterprise segments.

- Funding Servicing: This section provides options that allow purchasers to effectively carry out providers associated to the clearing, settlement, and execution of securities transactions and funds. These providers embrace custody, accounting, regulatory reporting, investor providers, efficiency and analytics, international trade, brokerage, and different main providers.

- Funding Administration: State Avenue World Advisors provides funding administration methods and merchandise. This section additionally gives providers and options associated to ESG investing, outlined profit and contribution merchandise, and World Fiduciary Options. Moreover, the corporate is a supplier of ETFs via the SPDR ETF model, which most readers will likely be aware of.

Earlier than we dive into the numbers, there are some things that give State Avenue an edge – not less than in line with the corporate.

Along with its international presence and broad portfolio of services and products, the corporate believes that its use of know-how and innovation is one thing that may give the corporate an edge.

For instance, State Avenue provides built-in platforms like:

- State Avenue Alpha, which mixes portfolio administration, buying and selling and execution, analytics, compliance instruments, and knowledge aggregation.

- State Avenue Digital, which focuses on creating providers associated to digital property and rising applied sciences like blockchain and cryptocurrency.

The corporate can also be a systemically necessary financial institution, which comes with intensive laws and supervision. This is likely one of the the explanation why main firms belief the corporate in the case of pension plans and so many different monetary points.

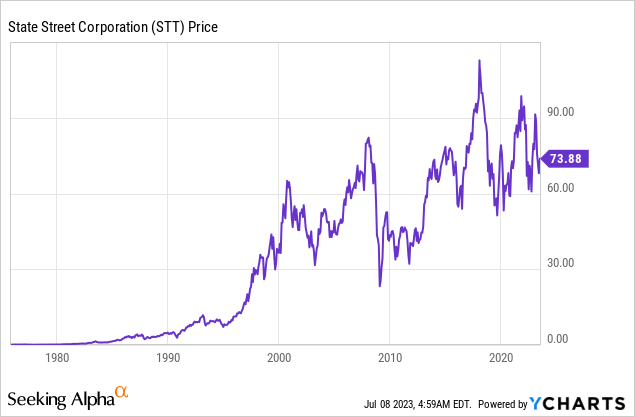

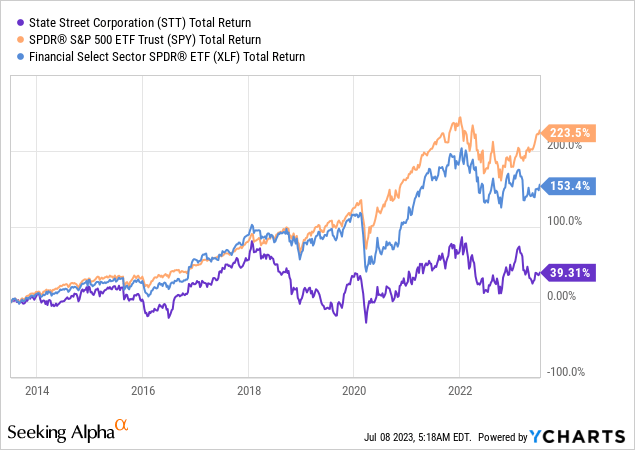

A Poor Whole Return However Regular Dividend Progress

Whereas State Avenue has typically popped up on my radar, I by no means cared about diving into its financials. The explanation was its lackluster efficiency. I simply could not be bothered by spending any time assessing an organization with a 10-year whole return of lower than 40% and a yield beneath 4%. In any case, a low whole return is not all the time a difficulty if a inventory seems to be a fantastic revenue play.

Talking of revenue, STT at present yields 3.4%, which is 20 foundation factors beneath the yield of the Schwab U.S. Dividend Fairness ETF (SCHD), which means it isn’t very removed from high-yield territory.

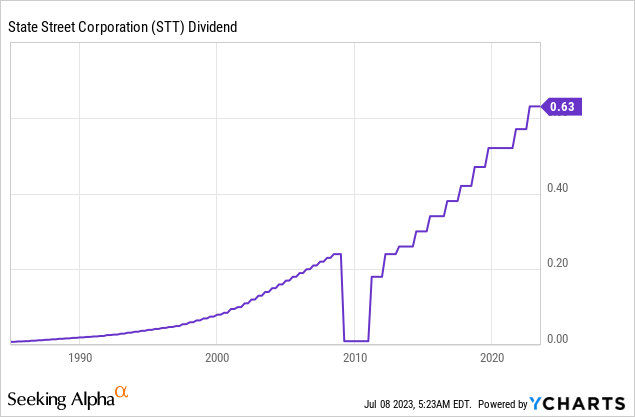

Trying on the chart beneath, we see that the corporate has a historical past of constant dividend progress – excluding a significant reduce throughout the Nice Monetary Disaster. Each previous to that recession and after, the corporate persistently hiked its dividend.

- Over the previous 5 years, the typical annual dividend progress was 8.5%, which could be very respectable for a inventory with a 3.4% yield.

- The payout ratio is 33%, which is wholesome and a sign of robust dividend protection.

Nonetheless, we’re not coping with a excessive yield.

So, to rapidly reiterate what we’ve thus far: the corporate has a persistently rising dividend with a considerably satisfying yield. Nonetheless, this yield is not juicy sufficient to fulfill the lackluster whole return of the previous ten years.

This implies we’d like a beautiful valuation. If that’s the case, STT out of the blue turns into a way more enticing inventory.

Discovering Progress In A Difficult Surroundings

Throughout this 12 months’s annual Bernstein Strategic Choices Convention in Might, the corporate mentioned the present atmosphere of uncertainty and stress on bills confronted by purchasers.

Therefore, the first focus for servicing purchasers is on discovering progress alternatives and managing bills.

Conventional asset managers are shifting in direction of ETFs, whereas non-public markets, notably infrastructure and personal credit score, proceed to expertise important progress.

Shoppers have been additionally involved concerning the growing prices of distribution, delivering Alpha, and know-how and operational infrastructure.

In different phrases, the idea of future-proofing know-how and operations is essential for asset managers.

The corporate must take care of macroeconomic headwinds, associated uncertainty amongst purchasers, rising prices, and the rising risk of disruption.

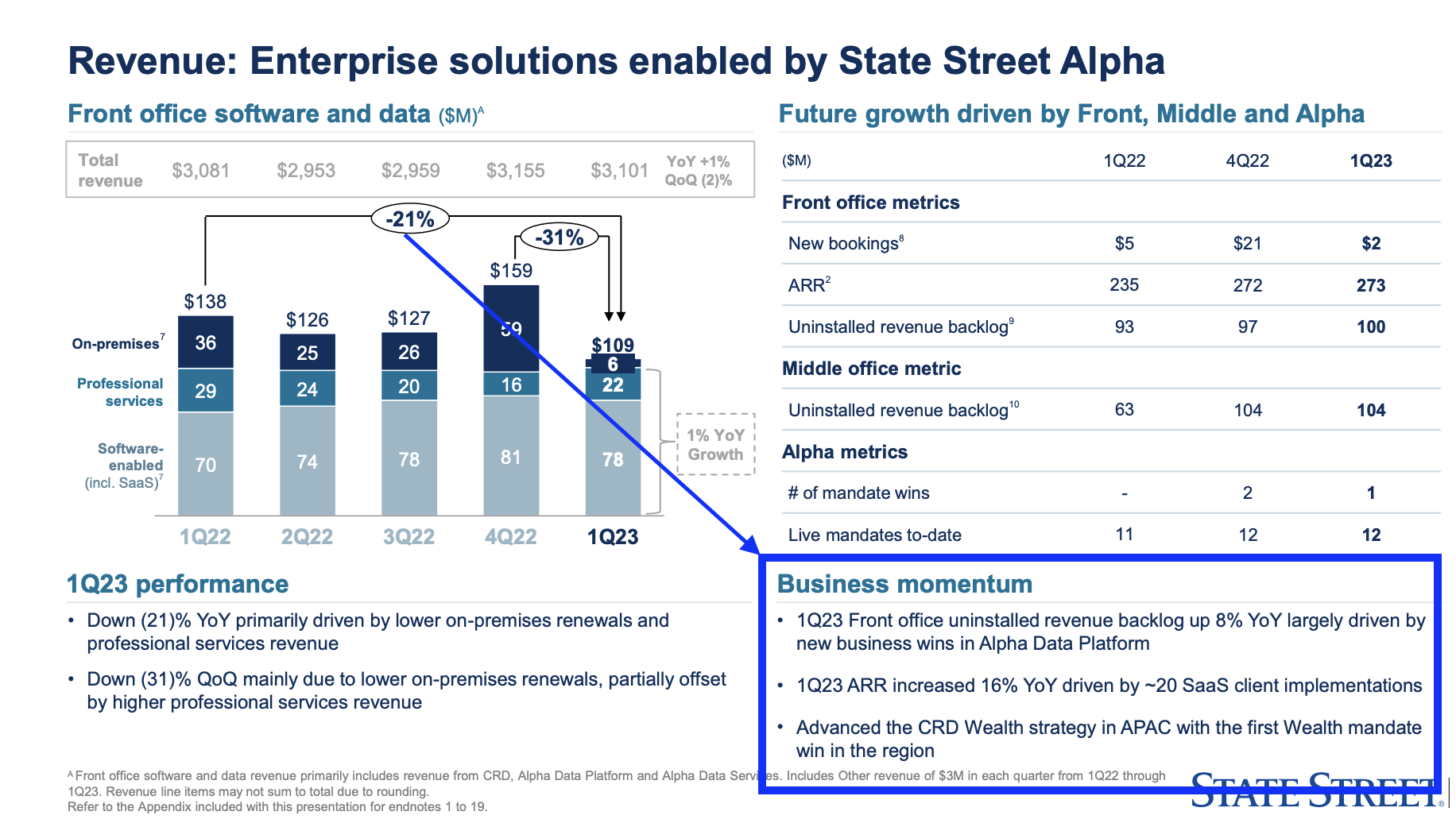

Through the aforementioned convention, the corporate additionally talked about that progress has been pushed by its Alpha front-to-back providing, which focuses on value discount, efficient knowledge administration, and know-how integration.

State Avenue

Primarily, State Avenue has been remodeled from a back-office service supplier to an enterprise outsourcer.

The corporate believes that whereas competitors is powerful, its true front-to-back capabilities give it a aggressive benefit.

Geographically, Europe and APAC current enticing alternatives, with the rise of personal fairness and the potential for deeper market penetration. The non-public markets section, notably in Latin America, nonetheless provides room for progress.

Moreover, State Avenue’s capital markets enterprise, particularly international trade, is a major space of focus and a chance for growing market share.

Moreover, the corporate is boosting its pricing technique. State Avenue has applied selective value will increase in areas equivalent to different servicing and hard-to-process segments to offset the impression of rising prices.

The inelasticity of purchasers’ responses to those value will increase may be attributed to the understanding that these advanced providers are important and require accuracy and reliability.

In different phrases, State Avenue’s differentiation technique has led to the introduction of value-adding providers with much less competitors. That is the place the corporate can acquire pricing benefits – particularly in occasions when it issues most.

This brings me to the subsequent a part of this text, which builds on these developments.

Present Developments & Valuation

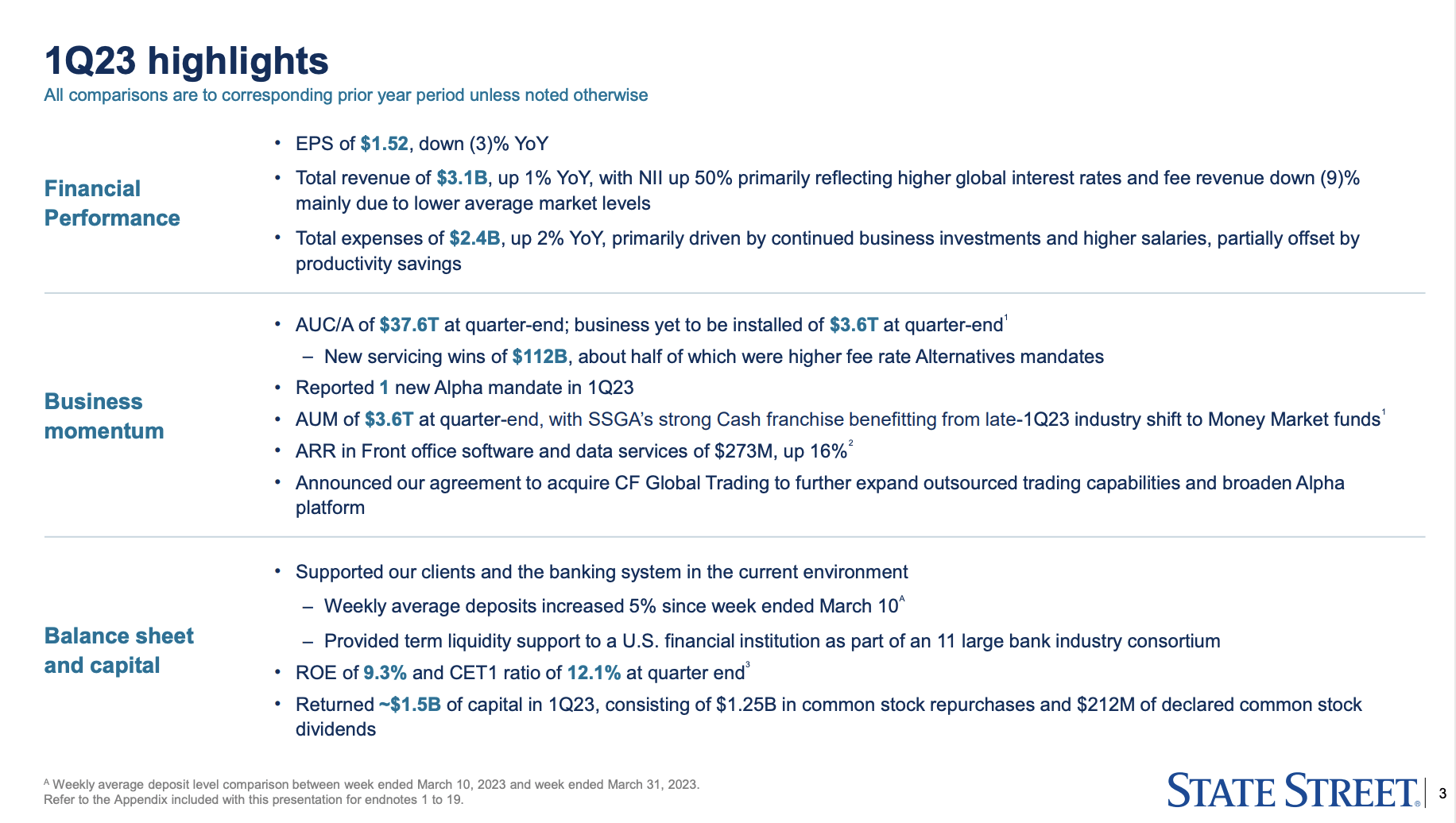

Whereas progress is gone – not less than on a short-term foundation – the corporate is holding up fairly nicely. Within the first quarter, the corporate reported earnings per share of $1.52, with a provision impression of $0.06 per share related to supporting the banking system.

Regardless of a decline in fairness and fixed-income markets, the corporate skilled power in internet curiosity revenue and securities finance enterprise, resulting in solely a 3% lower in EPS. The corporate additionally managed to regulate bills and continued investing in product and consumer progress initiatives.

State Avenue

Whereas outcomes have been negatively impacted by ongoing macro woes, the corporate remained centered on what issues most: increasing and specializing in new capabilities.

For instance, the acquisition of CF Global Trading introduced in March, will increase State Avenue’s outsourced buying and selling capabilities and liquidity-providing capabilities.

The transaction is anticipated to be accomplished by the top of 2023.

State Avenue recorded $112 billion in asset servicing wins within the first quarter, with roughly half from larger price charge different mandates.

The corporate additionally reported further Alpha mandates, which appears to show that its technology-focused enlargement goes easily.

State Avenue

State Avenue additionally maintains a top-tier steadiness sheet.

The Widespread Fairness Tier 1 (“CET1”) ratio was 12.1% at quarter-end, which is nicely above the regulatory minimal.

Going ahead, the corporate expects an enchancment in monetary metrics.

- State Avenue expects common US fairness and international bond markets to extend by about 1% to 2% quarter-on-quarter, with worldwide fairness markets remaining flat.

- General price income is anticipated to extend by 4% to five%, with servicing charges up 1% to 2% and administration charges roughly flat to up 1%.

- Entrance-office software program and knowledge revenues are anticipated to extend considerably, and the corporate plans to undertake new accounting steering for renewable vitality investments.

- Internet curiosity revenue is anticipated to lower by 5% to 10% sequentially, and bills are projected to stay flat. The corporate anticipates offsetting NII tendencies with larger price revenues and lively expense administration.

On a longer-term foundation, analysts (not the corporate) anticipate the corporate to proceed to generate annual internet revenue near $2.5 billion. After 2024, an upswing is anticipated.

- 2022: $2.7 billion.

- 2023E: $2.5 billion.

- 2024E: $2.5 billion.

- 2025E: $2.7 billion (8% implied year-on-year progress).

What this implies is that whereas the corporate is investing in areas that include respectable long-term progress potential, its dimension makes streamlining the enterprise a really sluggish endeavor.

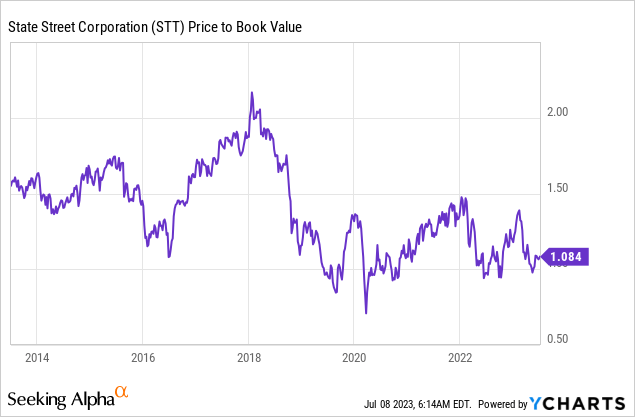

The corporate’s valuation confirms this. STT is buying and selling at 1.1x its e book worth. Analysts give the inventory a consensus value goal of $85, which is 15% above the present value. Nonetheless, I don’t anticipate the corporate to depart the extended and unstable sideways development and begin a significant uptrend anytime quickly.

Therefore, from a dividend investor’s perspective, I’d recommend two issues:

- When in search of revenue, purchase a monetary inventory with a better yield.

- If yield is not necessary, I’d recommend shopping for monetary corporations with extra progress and a better probability of robust long-term whole returns.

As a lot as I like STT as a enterprise and its capacity to ship top-tier providers, it is simply not a fantastic dividend play from my perspective. Evidently, everybody ought to be at liberty to disagree with me within the remark part.

Takeaway

State Avenue presents a blended image for dividend traders. Whereas it provides constant dividend progress and a beautiful valuation, its low whole return previously decade raises issues.

With a dividend yield of three.4%, it falls in need of higher-yielding choices available in the market. Nonetheless, the corporate’s international presence, broad portfolio, and modern use of know-how present it with a aggressive edge.

It has remodeled from a back-office service supplier to an enterprise outsourcer, specializing in value discount, knowledge administration, and know-how integration.

State Avenue’s differentiation technique and value-adding providers supply pricing benefits in a difficult atmosphere.

Regardless of ongoing macroeconomic woes, the corporate stays centered on increasing capabilities and investing in progress initiatives.

Nonetheless, attributable to its sluggish streamlining course of and extended sideways development, the corporate could not supply robust long-term whole returns for dividend traders, which is why I’ll go on the STT ticker – not less than in the intervening time.

{kind=link}