wildpixel

By Breakingviews

For the largest U.S. banks, the nerves this 12 months come after the examination. Giant lenders simply breezed through annual stress exams administered by their primary regulator, the Federal Reserve. Now companies like JPMorgan (JPM), State Avenue (STT), Goldman Sachs (GS) and Citigroup (C) are bracing for brand spanking new guidelines that fortify them in opposition to future catastrophes, at a punishingly excessive value.

Judging by Wednesday’s check outcomes, U.S. banks are robust sufficient to face up to a pointy recession with out their capital ratios – primarily fairness as a proportion of risk-weighted property – dipping into the hazard zone.

This 12 months’s checkup, the primary overseen by the Fed’s new supervisory chief Michael Barr, modeled what would occur if U.S. unemployment hit 10% and home costs plunged almost 40%, amongst different issues. The consequence: $541 billion of losses, however still-sufficient capital in any respect 23 lenders.

Stress exams are onerous, however they’re a trifle in contrast with the snowball of crimson tape rolling within the business’s path. Within the subsequent few weeks, the Fed and different regulators are attributable to unveil reforms that align U.S. lenders with worldwide requirements set by the Basel Committee on Banking Supervision.

These are a part of a bundle of reforms generally known as Basel III, however hefty sufficient that executives dub them Basel IV. JPMorgan boss Jamie Dimon has described rising capital necessities as “bad for America.”

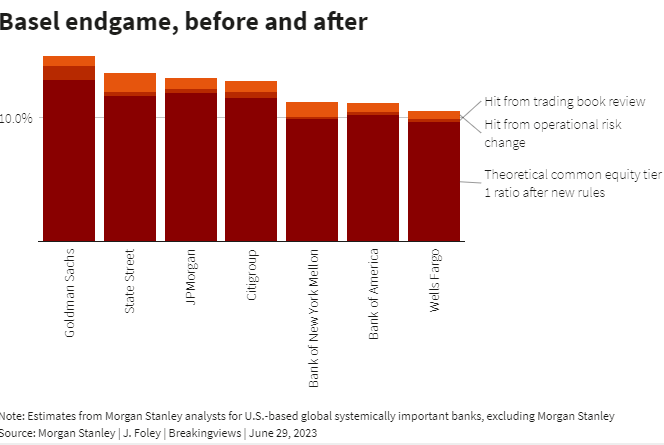

One motive executives are anxious is that the brand new guidelines – assuming they cleave to the Basel ideas – will zoom in on actions U.S. banks are good at. Take securities buying and selling.

Banks following the brand new method would tot up the exposures of every particular person desk, a extra granular method than at present, and will lose the potential profit from totally different models operating dangers that cancel one another out.

At Goldman Sachs, this shift alone might knock 1.1% off the agency’s capital ratio, Morgan Stanley analysts estimate. That’s equal to shrinking the Wall Street giant’s fairness by $7 billion.

One other huge change is the measurement of operational danger – regulator-speak for messing up. The Basel calculations dimension up this danger by closely weighting income from areas aside from lending and buying and selling, penalizing charges from funding banking recommendation or custodial providers.

Mixed with the buying and selling revamp, the Morgan Stanley evaluation suggests risk-weighted property – the denominator within the capital ratio – at Goldman, State Avenue and Financial institution of New York Mellon (BK) might rise by nearly 15%.

These are simply two examples of what’s coming. As well as, regulators have a lot discretion. Large U.S. banks can anticipate a 20% enhance of their required capital by 2027 when the foundations kick in, Fed Chair Jay Powell informed Congress final week. For U.S. establishments that regulators deem globally vital, that a lot additional padding could be round $180 billion, primarily based on capital figures cited by PwC.

Such shifts have real-world penalties. Extra capital on the stability sheet means there’s much less obtainable to pay dividends and fund share buybacks. It could possibly additionally make the enterprise of banking costlier.

Financial institution buyers sometimes demand a return on fairness of round 10% – greater than depositors or bondholders. Extra capital subsequently implies increased earnings. That sways banks’ choices on when to lend, and to whom.

The Basel tweaks have advantage. For instance, earlier incarnations of the laws didn’t successfully seize the chance of an unlikely occasion rattling a financial institution’s buying and selling operations. However U.S. watchdogs had already added their very own home-grown guidelines to fill among the gaps.

Fed stress exams topic banks to a theoretical market shock and incorporate parts of operational danger, after which spit out a “stress capital buffer” requirement tailor-made to every agency. That should be at the least as giant as Basel’s static “capital conservation buffer” of two.5% of risk-weighted property, and could be a lot greater. Goldman’s is presently 6.3%.

The danger for banks is that new guidelines get piled on high of current laws in a course of generally known as gold-plating. Fed Governor Michelle Bowman warned last week this could create aggressive dislocations.

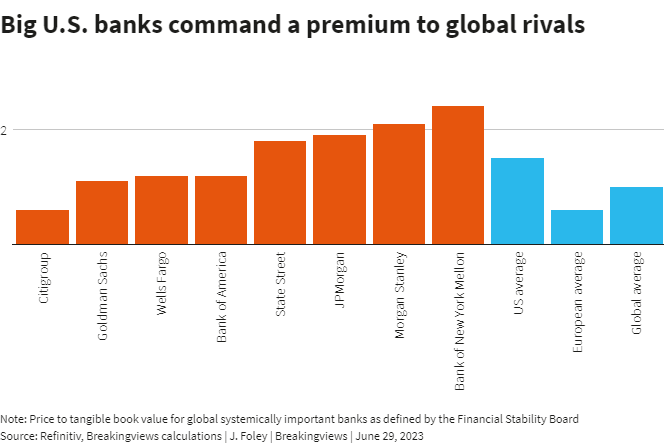

Nonetheless, the U.S. watchdog and its friends might even see regulatory overkill as a function, somewhat than a bug. Strong enforcement of guidelines can also be one motive U.S. financial institution shares are likely to commerce at a premium to European friends.

In addition to, regulators have been by means of a traumatic stress check of their very own. The implosion of mid-sized lenders SVB Monetary (OTCPK:SIVBQ), Signature Financial institution (OTCPK:SBNY) and First Republic (OTCPK:FRCB) earlier this 12 months left the Fed and Federal Deposit Insurance coverage Company with egg on their faces.

This helps clarify why FDIC chief Martin Gruenberg mentioned final week the brand new Basel guidelines may apply to all lenders with greater than $100 billion of property, dramatically widening the variety of banks caught within the web. The regulatory burden will make midsized banks much less aggressive. It’s additionally not clear the extra guidelines would have saved SVB.

One other caveat is that laws are solely pretty much as good because the individuals who implement them. Holding lashings of capital may give buyers and a few depositors larger consolation, however security and soundness is determined by financial institution examiners and displays doing their jobs successfully.

Latest financial institution failures confirmed that’s not occurring. The Fed and FDIC are stricken by tech shortfalls, fractured reporting lines and stodgy processes that meant apparent issues at susceptible banks didn’t set off well timed motion.

Step again, and it’s value asking whether or not international concord in banking guidelines is well worth the appreciable effort and paperwork. Positive, it’s useful if cross-border rivals are required to calculate the riskiness of their property in comparable methods.

However their security is determined by different elements, similar to whether or not the central financial institution props up markets when issues get powerful, because the Fed does, or governments share losses when banks fail, because the Swiss authorities did recently with Credit score Suisse (CS). The very fact is, although, that regulators are likely to need extra regulation. No surprise every check simply brings extra stress.

Context Information

The most important U.S. banks all handed annual stress exams administered by the Federal Reserve, the central financial institution mentioned on June 28. In a simulation of a “severely hostile” state of affairs of worldwide recession, the 23 lenders would have misplaced $541 billion, however all of their capital ratios would have nonetheless remained above the regulatory minimal.

U.S. banks are awaiting a proposal from their regulators to revamp capital guidelines, anticipated in July. A part of the reforms agreed by the Basel Committee in December 2017, the brand new guidelines are also known as “Basel IV” or the “Basel endgame.”

The foundations could be unlikely to be finalized till mid-2024, Federal Deposit Insurance coverage Company Chairman Martin Gruenberg mentioned on June 22. Gruenberg mentioned regulators have been contemplating increasing the attain of a stricter set of capital guidelines to incorporate banks with over $100 billion in property.

Federal Reserve Chair Jay Powell gave an identical message to Congress later that day, although he mentioned the majority of the capital reforms would apply to the largest companies.

Editor’s Word: The abstract bullets for this text have been chosen by In search of Alpha editors.

{kind=link}