primeimages

A visitor publish by D Coyne

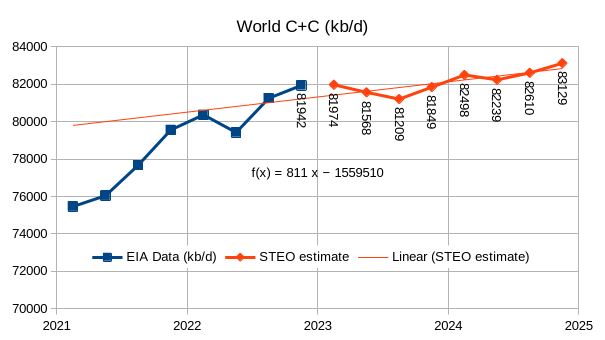

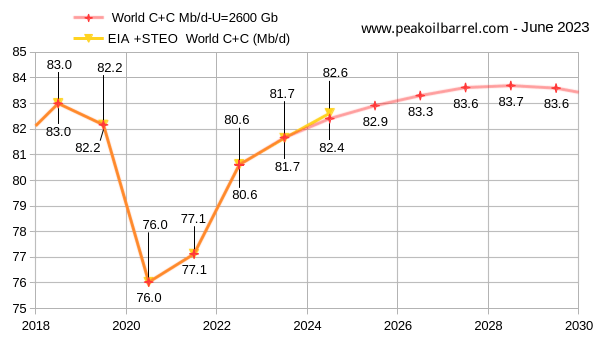

The EIA’s Short Term Energy Outlook (STEO) was printed in early June. The chart beneath estimates World C+C by utilizing the STEO forecast mixed with previous knowledge from the EIA on World Output.

Determine 1

Output rises to 81849 kb/d within the last quarter of 2023 and to 83129 kb/d in 2024Q4. Annual common World C+C output was 80752 kb/d in 2022 and rises to 81650 kb/d in 2023 and to 82619 kb/d in 2024.

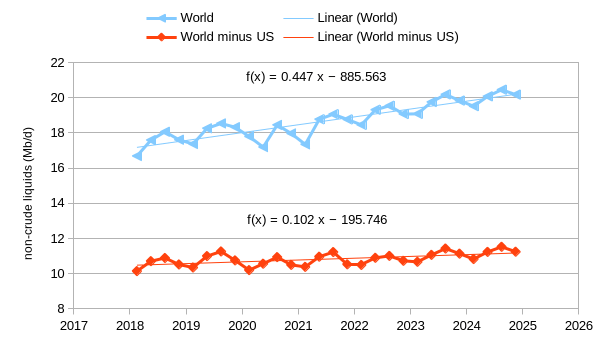

Determine 2

The chart above considers World non-crude liquids output (observe that “crude” on this case is C+C) and compares with non-crude liquids output for the World minus US (excludes non-crude liquids produced within the US). About 77% of the rise in World non-crude liquids output over the 2018 to 2024 interval will come from the US if the STEO forecast for 2023 and 2024 is correct (it normally shouldn’t be.)

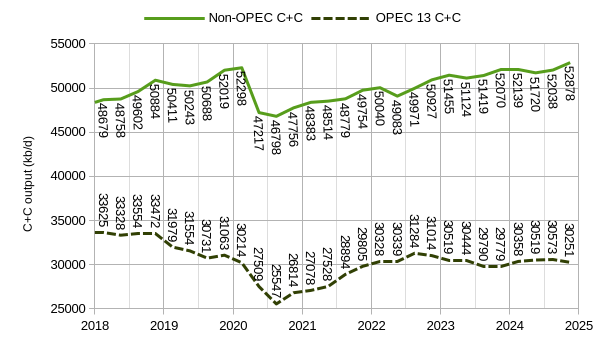

Determine 3

Chart above exhibits OPEC 13 and Non-OPEC output with STEO estimate after 2022Q4 (final 8 factors on every sequence).

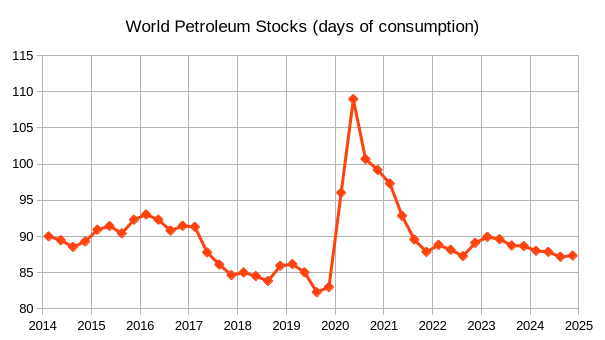

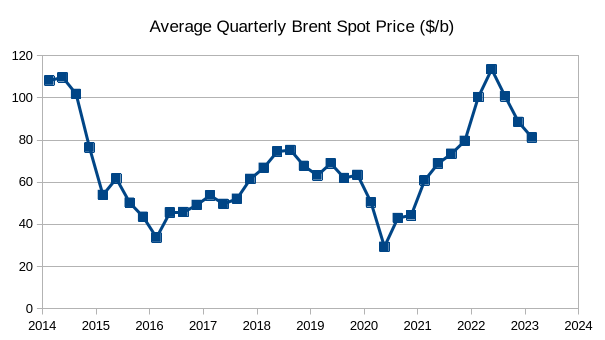

The chart above makes use of the EIA World liquids provide and demand steadiness from 2014Q1 to 2024Q4 from the STEO and assumes that in 2014Q1 the World Petroleum Shares have been 90 days of 2014Q1 consumption. Typically, nations intention for about 90 days of petroleum shares and I’ve assumed this intention was met within the first quarter of 2014. This alternative was arbitrary. Oil costs will normally rise as inventory ranges fall beneath 90 days of consumption, although poor visibility of World inventory ranges makes this a tough estimate (in actuality, it tends to be within the vary of 88 to 92 days of consumption). Chart beneath exhibits common quarterly Brent Spot costs over the 2014 to 2023 interval.

Determine 5

I anticipate that oil costs could rise as inventory ranges fall beneath 90 days of consumption by 2023Q3 if the EIA STEO provide and demand estimates are correct.

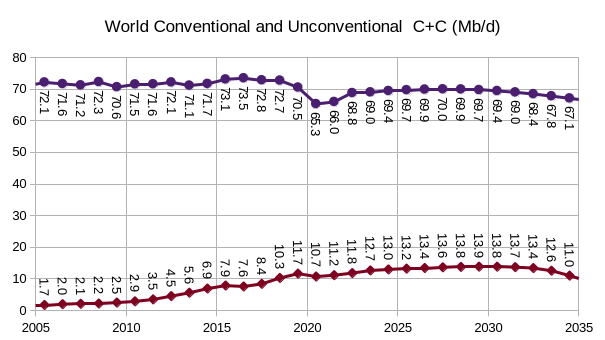

The chart above makes use of Paul Pukite’s Oil Shock Mannequin to estimate future output with the idea {that a} transition to electrical transport reduces oil demand to lower than provide by 2032 (+/- 2 years). The information above the road is EIA knowledge as much as 2022 and 2023 and 2024 are the STEO estimates, the information beneath the road is the mannequin output. The 2018 peak is exceeded in 2025 for my finest guess mannequin (100% chance this can be fallacious) and the height is in 2028 at 83.7 Mb/d.

The determine above exhibits typical and unconventional C+C output for the Oil Shock mannequin in Determine 6. Unconventional C+C is outlined as US Tight Oil (LTO) and additional heavy oil (API Gravity of 10 levels or much less) produced from Canadian Oil Sands or Venezuela’s Orinoco belt, typical C+C is all C+C that can not be categorized as unconventional as outlined above. From 2018 to 2028, unconventional output will increase by 3.5 Mb/d whereas typical output decreases by 2.8 Mb/d, there’s a internet enhance in World C+C output of 0.7 Mb/d in 2028 above the earlier 2018 peak. The unconventional C+C URR for this situation is 170 Gb.

The tight oil mannequin utilized in my most up-to-date shock mannequin has a decrease URR than the mannequin introduced final month (72 Gb vs 81 Gb), there’s a shorter plateau (2028-2030) and a thinner tail with completion charge assumed to fall after 2029 as a consequence of a mixture of fewer worthwhile areas to drill new wells and decrease oil costs as extra land transport strikes to electrical energy. Extra particulars on this situation beneath.

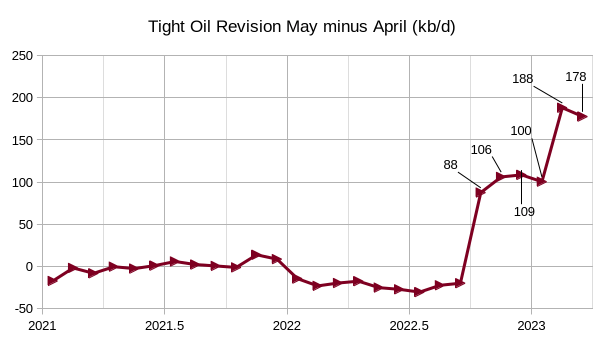

There was a big revision in final month’s EIA official tight oil estimate, particularly for the months of October 2022 to March 2023 (the revisions for these months are indicated in determine 9) with the revisions for February and March at 188 and 178 kb/d, greater than the Could report. There have been additionally revisions decrease by roughly 25 kb/d for Feb 2022 to Sept 2022.

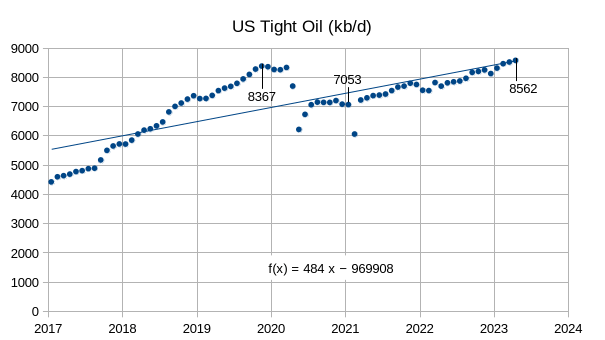

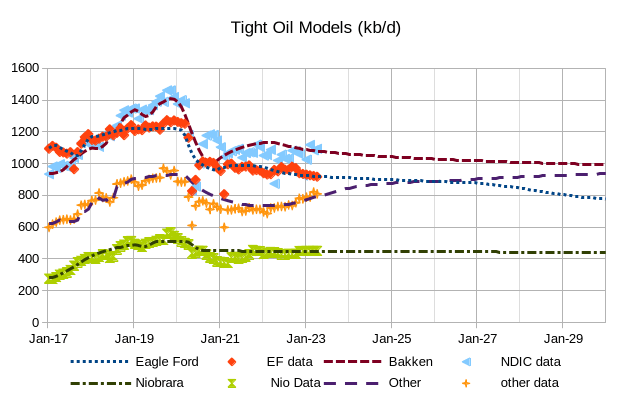

The chart above offers an outline of US tight oil output from Jan 2017 to April 2023 with the long-term OLS pattern at an annual charge of enhance of 484 kb/d utilizing all knowledge from Jan 2017 to April 2023 (no knowledge is dropped from the regression). For the previous 24 months, US tight oil has elevated at an annual charge of 580 kb/d or a month-to-month charge of about 48 kb/d every month primarily based on a linear regression utilizing abnormal least squares (OLS). An endpoint estimate utilizing a line via April 2021 and April 2022 offers an annual charge of enhance of 640 kb/d over that interval (barely greater than the OLS estimate) with a month-to-month charge of enhance of about 53 kb/d.

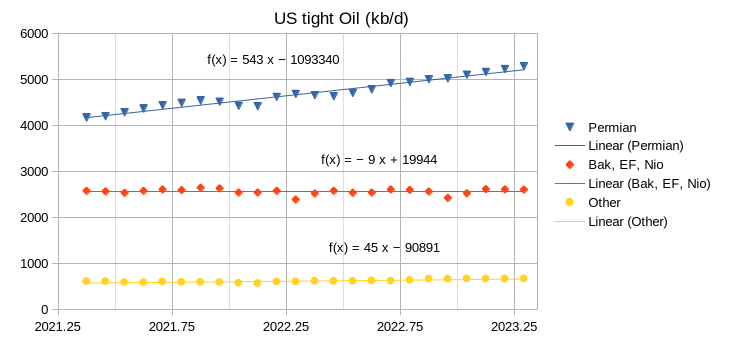

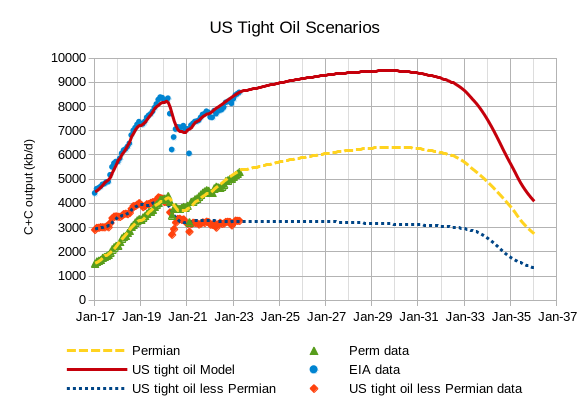

Many of the enhance in US tight oil output over the previous 24 months has come from the Permian basin with a small contribution from ”different” tight oil performs such because the Anadarko, Powder River, and a few contribution from shale gasoline performs which yield some lease condensate. Tight oil output from the Bakken, Eagle Ford, and Niobrara performs as a bunch was trending down at an annual charge of 9 kb/d over the previous 29 months. Output from all non-Permian tight oil performs was barely rising at an annual charge of 36 kb/d or a month-to-month charge of three kb/d over the previous 24 months. Final month’s estimate for the previous 24 months (April 2021 to March 2023) for non-Permian tight oil output was a lower of 45 kb/d. The revisions within the knowledge and a shift within the interval lined by one month resulted in a internet enhance of 81 kb/d for non-Permian output in comparison with final month’s estimate. The change within the Permian annual charge of enhance in output was comparatively minor by comparability at a rise of 8 kb/d from 535 kb/d final month to 543 kb/d for the latest estimate.

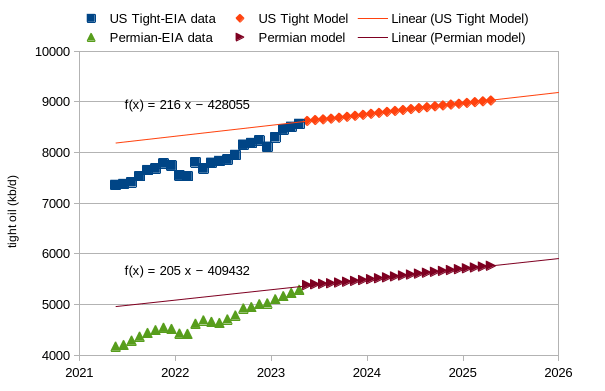

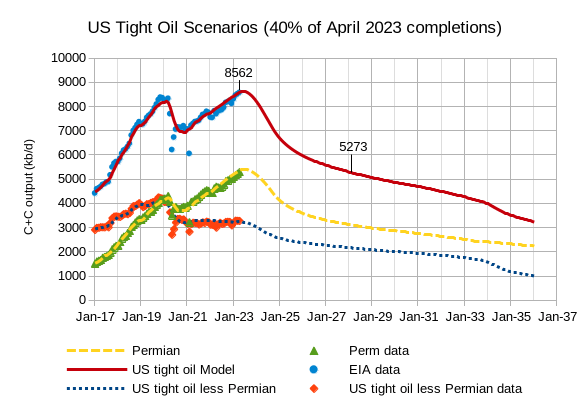

The chart above exhibits projected output for a situation the place the completion charge for US tight oil wells stays fixed at 15 wells lower than the April 2023 degree from Sept 2023 till April 2025. US tight oil will increase at an annual charge of 216 kb/d from Could 2023 to April 2025 and Permian output will increase at an annual charge of 205 kb/d over the identical interval. These charges are about 67% of the charges of enhance reported final month (about 315 kb/d) because the eventualities have been revised.

Observe that the eventualities above assume no enhance within the new nicely completion charge after Sept 2023 which is 15 wells beneath the April 2023 charge of completion, it stays fixed from September 2023 to February 2029. There was a slight revision to the “Different” tight oil mannequin the place different performs are these that aren’t Permian, Bakken, Eagle Ford, or Niobrara performs. Bakken URR is 9.5 Gb, Eagle Ford URR is 8.5 Gb, Niobrara URR is 3.5 Gb, and Different tight oil URR is 8.5 Gb, with a complete URR for non-Permian tight oil performs at 31 Gb.

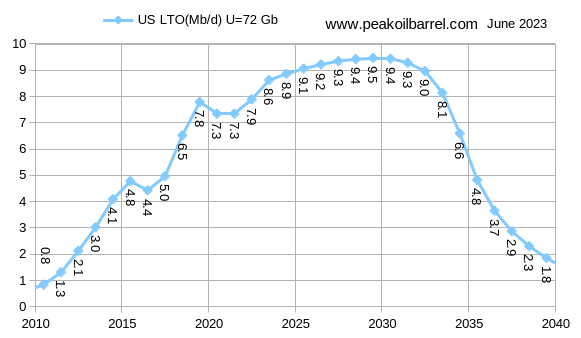

The chart above merely is the sum of the eventualities introduced in Determine 13 (US tight oil much less Permian) plus the Permian situation proven in Determine 14. I prolong the chart out to 2036 to point out the anticipated output decline, which falls by half in 3.33 years from 9000 kb/d in June 2032 to 4480 kb/d in Sept 2035. The URR of the tight oil situation is about 72 Gb (9 Gb smaller than the situation introduced final month). The common annual charge of enhance from Could 2023 to April 2029 is about 1.6% per 12 months for this situation. The Permian situation has a URR of 40 Gb with a peak of 6.32 Mb/d in Jan 2030, and the US tight oil situation peaks in November 2029 at 9.47 Mb/d.

The situation above reduces April 2023 tight oil completions by half in every non-Permian basin over a 12-month interval from Could 2023 to April 2023 and Permian completions are diminished to one-third of the April 2023 degree by April 2024. General, the completion charge is diminished from 955 wells monthly accomplished in April 2023 to 380 wells monthly in April 2024. US and Canada have refinery capability to deal with about 4600 kb/d of tight oil. In an effort to keep away from US crude exports exterior of North America, we have to intention for 4600 kb/d of tight oil output. The situation in determine 15 would scale back US tight oil output to about 4600 kb/d by July 2031, in Feb 2028, crude exports exterior North America are diminished to about 700 kb/d. The URR of the situation in determine 15 above is 58.5 Gb and observe that the completion charge may very well be elevated after July 2031 to maintain tight oil output flat if desired. Observe that in 2019, about 5290 kb/d of tight oil was refined within the US (or was produced and never exported exterior North America), it’s unclear why there’s such a big distinction between 2019 and 2022. Maybe LTO is being produced within the Canadian Bakken and has diminished Canadian demand for LTO (this might clarify about 200 kb/d of decrease exports to Canada in 2022 in comparison with 2019); additionally, some refinery capability for tight oil could have been shut down within the US through the pandemic. It appears seemingly that the estimate primarily based on 2022 knowledge is extra correct.

Editor’s Observe: The abstract bullets for this text have been chosen by In search of Alpha editors.

{kind=link}