andreswd/E+ through Getty Photographs

Writer’s Notice: This text was printed on iREIT on Alpha again in late Might of 2023.

Expensive subscribers,

KION AG (OTCPK:KNNGF) is an organization that has already been paying off fairly a bit as an funding for the previous few months. My final main purchase was made throughout later durations of 2022 – and my stance in September has produced a TSR of round 12.38% together with the dividend, in comparison with the three.82% of the S&P500 as of the time of writing this text.

Nonetheless, KION’s restoration is prone to stay considerably muted within the close to time period. The corporate has loads of hurdles to beat – that is why it is so low-cost. Nonetheless, I consider the corporate will overcome these and considerably outperform – which is the place I take my conviction from.

On this article, I will replace my thesis, and present you why I count on a non-trivial upside of 250% for KION – at the very least in the long run, as soon as issues actually normalize.

KION – Upside in supplies dealing with and automation

KION is the market chief in a number of essential applied sciences not solely essential for the present growth in industrial applied sciences and supplies in addition to logistics, however essential.

KION is the world chief in industrial truck options in EMEA, and the worldwide #2 in the identical phase. It is #1 in world provide chain options and might report an annual order consumption climbing towards the €13B on an annual foundation. This has seen some stress over the previous yr or so, however the issue with KION and what has induced it to fall just isn’t top-line progress or lack thereof. The corporate the truth is has a well-filled orderbook and glorious demand tendencies. Nonetheless, it is all the way down to round €11.1B in 2022, with a brand new consumption of barely above that.

The problem is absolutely discovered within the firm’s margins. On a pre-tax, or EBIT foundation, the corporate made solely 2.6% for FY22, and that is actually fairly horrible for a market chief in provide chain options and 1-2nd place in industrial vans.

The corporate’s income cut up and footprint stay interesting…

KION IR (KION IR)

…and it is the primary firm to supply the type of fully-automated large-scale warehousing and logistics options to automated warehouses with a full life cycle product providing, together with providers. Toyota could at the moment be the chief in Industrial Vans, however KION leads the cost, by far, in Automation and logistics.

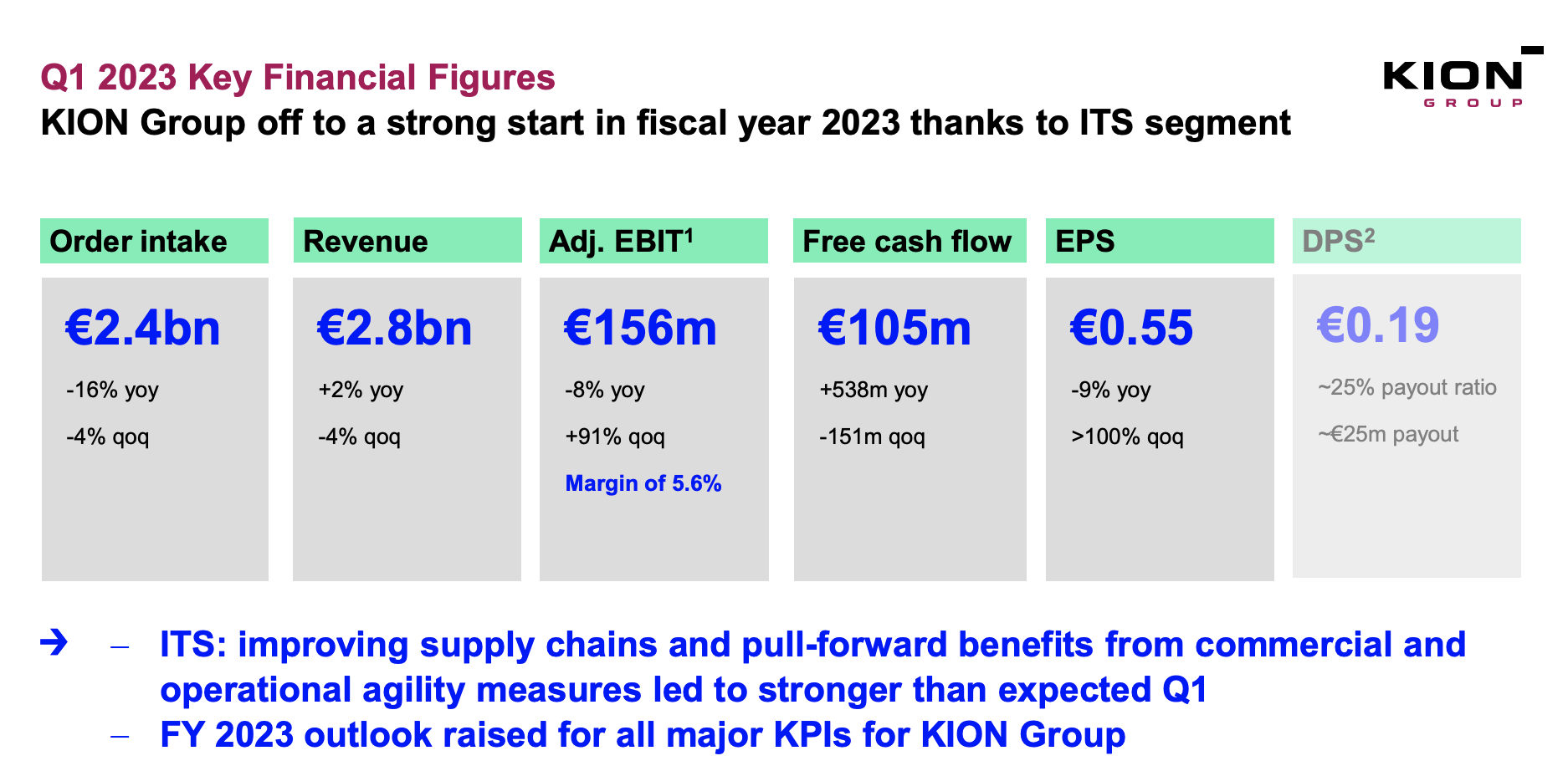

The troubles that KION faces are broad-based and never distinctive to KION as an organization. We noticed lots of these points reappear, or make clear throughout 1Q23. The corporate had a powerful begin to the yr, with a good-sized order consumption and a 2% income enhance, however margins are something however solved. With a -8% YoY adjusted EBIT, we’re not seeing 2.6% EBIT, however we’re seeing 5.6% in comparison with the same old double digits. Nonetheless, outcomes have been up considerably quarterly, so the restoration has on the very least begun.

KION IR (KION IR)

Additionally, the corporate has delivered important upside for its prospects throughout 1Q, together with new Li-ion partnerships, its personal gasoline cell system, and a brand new multi-brand world technique, with important concentrate on new export merchandise from China. The corporate’s ITS phase consequence have been higher than anticipated, with provide chain restoration driving income and margin restoration.

Postponements are actually the primary situation and motive as to why the corporate is not recovering quicker. The present financial uncertainty, with folks anticipating a recession to start and maybe final for a while, choices on new orders for logistics techniques and industrial vans are being postponed, resulting in order uncertainty for KION. There may be good visibility within the near-term order ebook, however many of the motive why KION noticed a great 1Q23 is as a result of particular ITS phase.

Merely put, the corporate’s margin growth and restoration can be aided by recoveries and tendencies within the general macro, which is at the moment unsure. One of many main drivers of the corporate at the moment being down is buyers and prospects being unsure of when this can be.

Nonetheless, it is clearly essential to not mistake this for it by no means recovering. And that could be a widespread mistake I see buyers making, value-oriented or not. When an organization is buying and selling down as KION as soon as did, it’s as if buyers don’t count on the corporate to ever get better. Whereas this can be true for some companies, which then do find yourself going bankrupt, a market chief like KION is extremely unlikely to go to zero in as quick a time as that.

For that motive, I view the present tendencies as very favorable when it comes to valuation, which we’ll look nearer at in a short time.

For now, I need to spotlight the next:

- KION is in a restoration type of mode – the corporate’s margins are as little as they have been for a number of years. The final time it was this dangerous was in related, recession-type environments. Don’t count on a fast turnaround.

- On the similar time, the corporate is displaying early indicators of elementary restoration. In 1Q23, we noticed the EBIT margin get better to above 5% as singular firm segments went again towards normalization.

- As a result of the corporate’s fundamentals stay extraordinarily stable, that is the proper time for value-conscious long-term buyers that may settle for a 2-5 yr time interval to get better. Should you’re keen to do that, you may see these 250%+ returns that I’m speaking about right here.

- I view restoration as extraordinarily possible over time. The corporate has a historical past of being unstable. Even earlier than the pandemic, it went as much as virtually €80/share earlier than tumbling to €38 within the COVID-19 mania. Which means the corporate is now cheaper than throughout COVID-19.

The corporate’s margins have declined to sector common, or beneath the sector common, relying in your comps. Nonetheless, that is as a result of large decline within the final 2 years, which is prone to be non-permanent, as I see it.

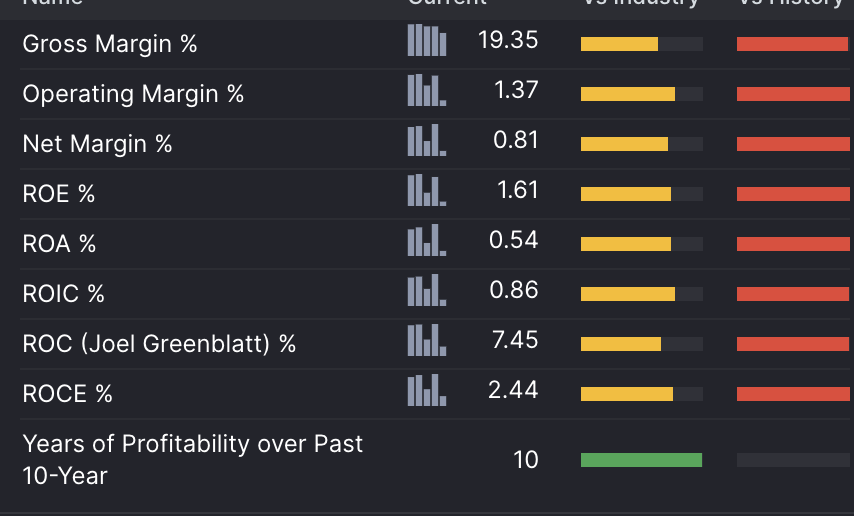

KION Profitability (GuruFocus)

And, as you’ll be able to see, firm profitability continues to be glorious over a 10-year time period. I additionally need to level out that regardless of a web margin of lower than a p.c at the moment on a 2022 foundation, the corporate nonetheless is not even near “worst” in its phase.

This isn’t an excuse – however a highlighting of how badly the pandemic and the most recent yr impacted firm margins sector-wide. KION just isn’t alone, and it’s definitely not distinctive.

The corporate’s dividend is lower to the bone. Do not buy KION for the 2022-2023 dividend – it is at the moment lower than 0.6%. Nonetheless, the corporate has lower than 35% LT debt/cap, it is BBB-rated and investment-safe (on a ranking foundation), and regardless of all of the negatives, stays worthwhile.

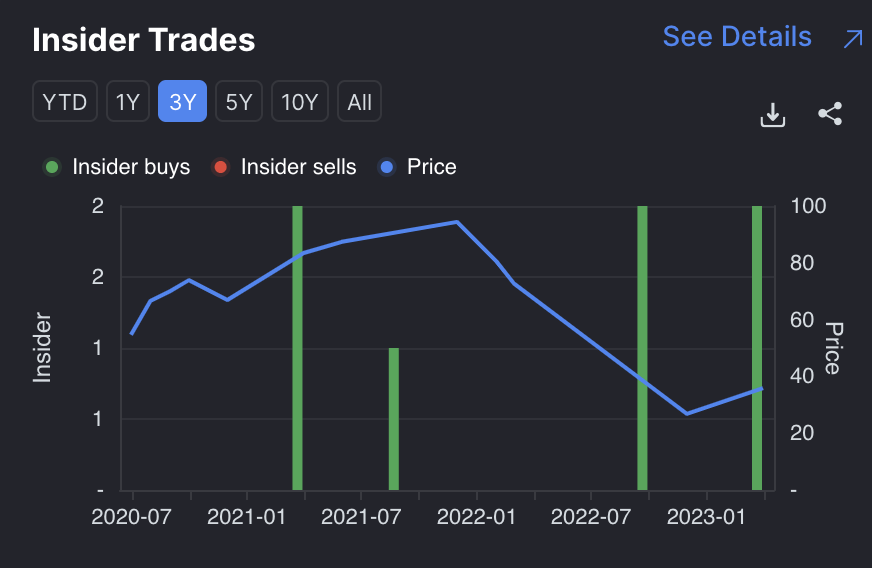

I additionally need to spotlight that KION has seen a good quantity of current insider shopping for, which is usually a great piece of stories in an setting like this or for a inventory like this. And people insider buys have truly been rising, about throughout the identical time that I’ve been shopping for as effectively. In actual fact, not a single insider has been promoting inventory regardless of the rollercoaster the corporate has been doing.

KION insider shopping for (GuruFocus)

Based mostly on this, and every thing I’ve mentioned above, I am constructive concerning the prospects of KION, and offer you my valuation assumption for the corporate presently.

KION’s valuation – Stays constructive, and I see a large upside

As typical, I like contemplating probably the most lifelike attainable outcomes, or at the very least a spread of them, when investing in an organization. There are a lot of attainable outcomes for investing in KION, however the widespread thread I see in every of them comes all the way down to the online outcomes being fairly constructive general.

The explanation for that’s easy. I do not forecast – and any analyst I observe or have listened to, nor subscribe to does both – the corporate’s margin-related troubles to remain round for that lengthy. In actual fact, we count on normalization to happen to some extent this yr.

What I imply by normalization is that this.

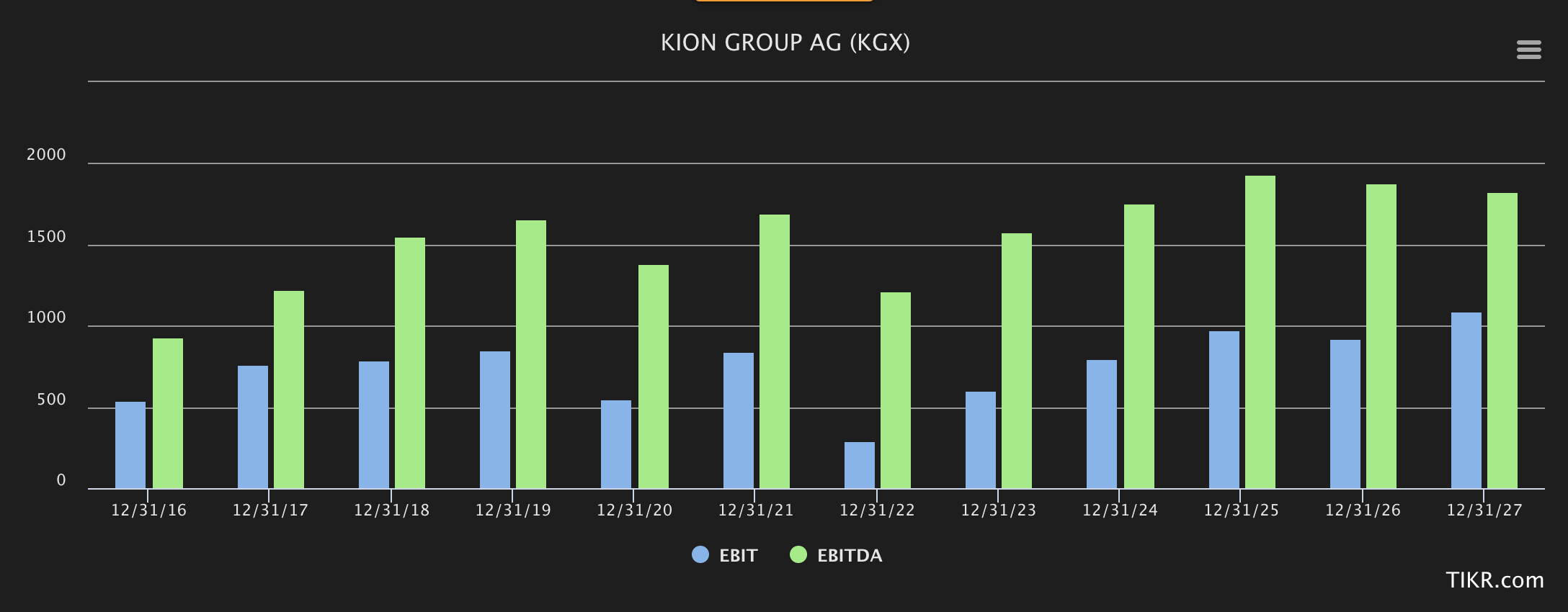

KION forecasts (S&P International/TIKR.com)

That 2022 was a foul yr, little doubt. Nonetheless, that issues are going to get better looks as if a foregone conclusion at this level. With 1Q23 within the bag, the fear that is still just isn’t “if” the corporate will get better because the order books begin filling up once more and prospects transfer “again on observe” with their investments, it is “when”.

And since I make investments inside a 2-5 yr timeframe, and I consider it can occur throughout that timeframe, the precise “when” of it does probably not matter. What I consider is that when it does happen, this firm will advance considerably. We have already seen double-digit market outperformance since September – however that may appear pale compared to what a normalized honest worth for the corporate as soon as it goes again to progress can be.

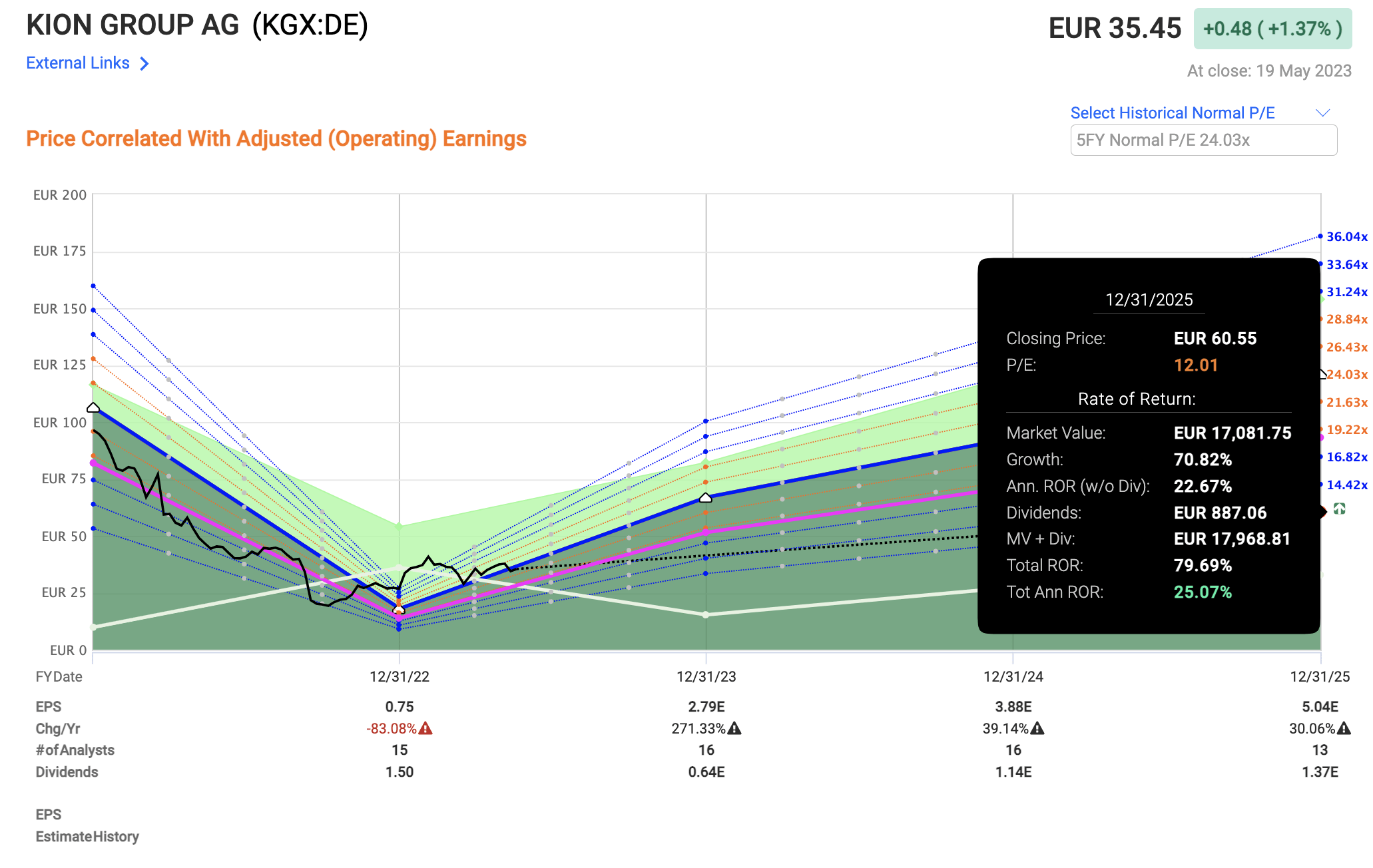

Should you needed to, you can forecast KION at a 12.01x P/E on a ahead foundation. That is conservative – and effectively beneath the place the corporate often is. It is the lowest I’d go for – and what does that offer you?

F.A.S.T graphs KION Upside (F.A.S.T graphs)

Market-beating RoR of 25% per yr.

That is the bearish case, to be completely clear with you. As you begin adjusting upward, your upside solely grows. A good-value 15x is nearer to 35% per yr, or 114% till 2025E, and a 20-24x P/E which is a historic 5-year common for this specific firm is available in at 61% yearly, or 250.51% TSR till 2025E.

Now, thoughts you that that is predicated on the corporate truly hitting its targets. I do consider it can do precisely this although, even when the analyst accuracy is barely about 75% on a 2-year foundation with a 20% margin of error. There may additionally be that the margin restoration does not go as shortly or as “deeply” as analysts count on. Nonetheless, even based mostly on this I see that large 12-24x P/E upside as sufficient to be market-beating in any doubtlessly lifelike situation presently.

That makes KION, along with investments like Teleperformance (OTCPK:TLPFY), one of many highest, most secure total-return performs that I at the moment have interaction in. Each of those firms share many similarities, although KION is the extra unstable of the 2 and is within the industrial, moderately than the communications phase.

Nonetheless, each companies are massively underappreciated for what they’re, and I consider this may result in large returns and restoration for these buyers keen to take a position, and for the corporate to get better.

As that is my M.O., I shouldn’t have a difficulty with this.

The present S&P International targets, as a enjoyable train, come to a spread of €20 on the low facet and €63 on the excessive facet to a median of €44. A couple of yr in the past, this was €64 on the low facet and €140 on the excessive facet, with a median of virtually €100/share.

Do you consider that the corporate has misplaced greater than 50% of its elementary worth in lower than a yr?

I don’t – and that’s what I spend money on right here.

Thesis

My thesis on KION is as follows:

- KION Group is a horny capital items play with an emphasis on intralogistics options, automation, and warehouse applied sciences – issues like forklifts, to place it merely.

- The corporate is undervalued and forecasts suggest a big upside over the approaching 5 years, with an upside of over 100%.

- KION is a “BUY” with a value goal of €78/share, however I’m not shifting it additional.

Bear in mind, I am all about:

Shopping for undervalued – even when that undervaluation is slight, and never mind-numbingly large – firms at a reduction, permitting them to normalize over time and harvesting capital positive factors and dividends within the meantime.

If the corporate goes effectively past normalization and goes into overvaluation, I harvest positive factors and rotate my place into different undervalued shares, repeating #1.

If the corporate does not go into overvaluation, however hovers inside a good worth, or goes again all the way down to undervaluation, I purchase extra as time permits.

I reinvest proceeds from dividends, financial savings from work, or different money inflows as laid out in #1.

Listed below are my standards and the way the corporate fulfills them (Italicized).

This firm is general qualitative.

This firm is essentially secure/conservative & well-run.

This firm pays a well-covered dividend.

This firm is at the moment low-cost.

This firm has a practical upside based mostly on earnings progress or a number of growth/reversion.

That implies that the corporate nonetheless fulfills all of my standards for engaging valuation-oriented investing. I am nonetheless at a “BUY”.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a significant U.S. trade. Please concentrate on the dangers related to these shares.

{kind=link}