Smederevac

That is my second Eiger BioPharmaceuticals (NASDAQ:EIGR) article following 02/2023’s “Eiger BioPharmaceuticals: The Results Are In – The CEO And The CFO Are Out” (“Outcomes”). For the reason that publication of Outcomes, wherein I characterised Eiger as a “dealer’s delight”, Eiger shares have dropped >50% from $2.22 to <$1.00.

On this article I focus on its prospects going ahead.

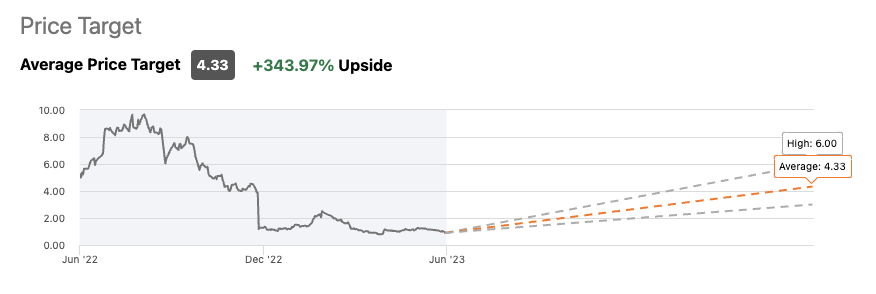

Wall Road Analysts have pegged Eiger as having >300% upside.

The three Looking for Alpha Wall Road Analysts overlaying Eiger have lined up with sturdy constructive expectations for it. As proven beneath they’ve common value targets of $4.33 for a +343.97% Upside:

seekingalpha.com

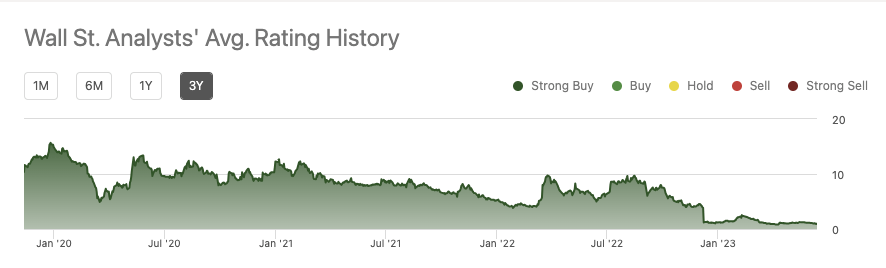

This bullish perspective has held constant for the complete three 12 months interval tracked on Looking for Alpha:

seekingalpha.com

The Wall Road Journal’s and Barron’s monitoring of Eiger analysts is analogous, albeit barely extra nuanced.

Counterbalancing this bullish perspective think about Looking for Alpha’s 06/15/2023 quant score of sturdy promote. This has been holding steady for the complete 12 months of 2023 ever since its 12/08/2022 70% drubbing following announcement of topline knowledge from its Part 3 D-LIVR research for lonafarnib.

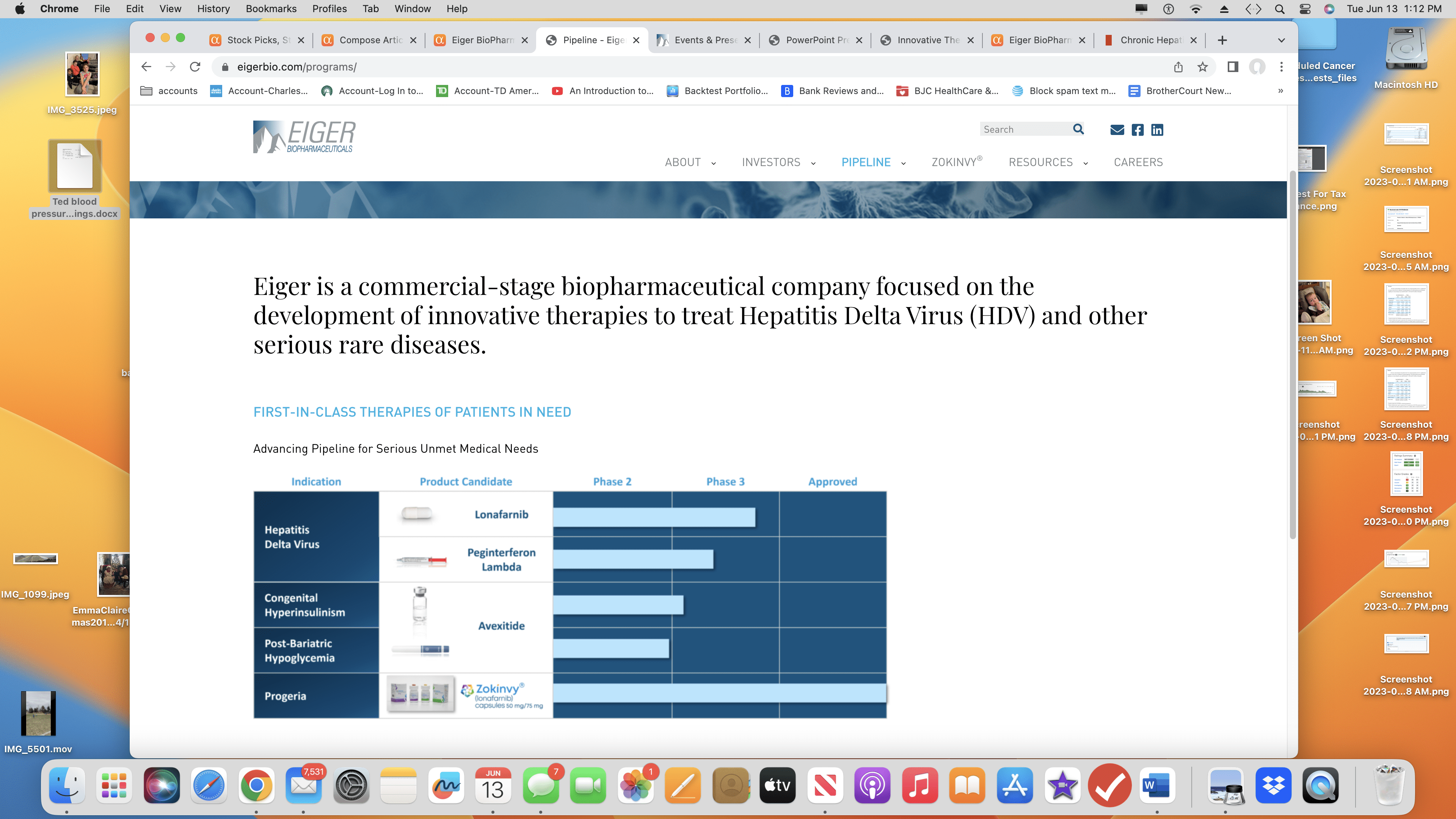

Eiger’s pipeline of marketed (1) and medical (3) therapies is unremarkable.

Basic

Eiger’s pipeline graphic from its web site lists a single marketed remedy and three medical stage property that it’s growing:

eigerbio.com

Marketed remedy — Zokinvy

As mentioned in Outcomes, Zokinvy® (lonafarnib) is decidedly small beer. Probably due to administration upheaval mentioned in Outcomes, Eiger issued no earnings name for This fall, 2022 or for Q1, 2023 as had been its earlier practice.

For each quarters it issued earnings and enterprise replace press releases (for Q1, 2023, the “Release“). The discharge suggested that Zokinvy had advertising and marketing approval within the EU and UK in remedy of Progeria and Processing-Poor Progeroid Laminopathies. It achieved internet income of $4.1 million in Q1 2023.

It additionally suggested:

Product income, internet was $4.1 million for the primary quarter of 2023, as in comparison with $2.7 million for a similar interval in 2022. The rise in product income was primarily resulting from increased gross sales in Germany, France ATU, and U.S throughout the quarter.

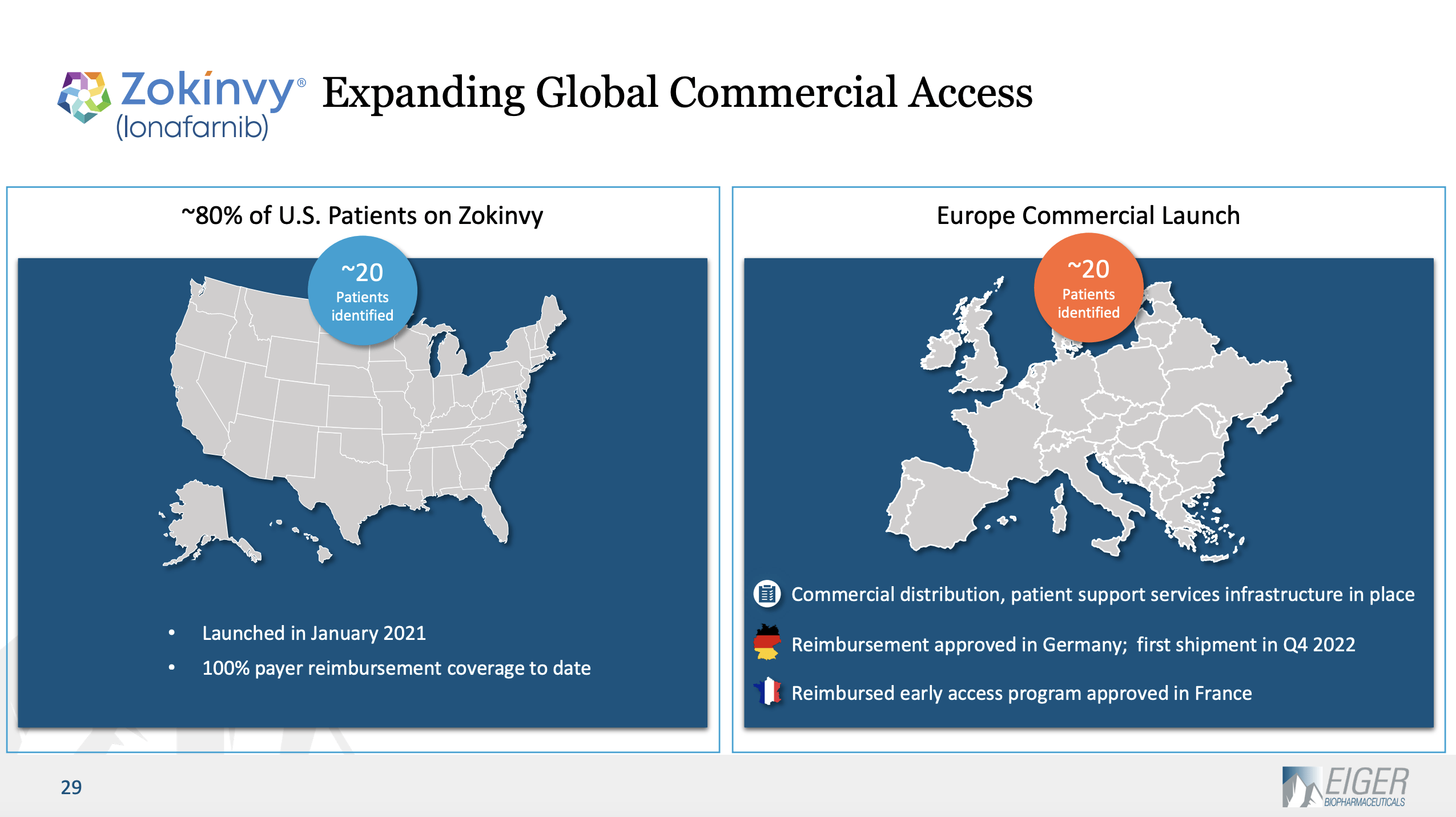

Past this revenues recommendation, the Launch gives nothing else on Zokinvy. Eiger’s newest presentation from its web site is its 04/2023 slide deck the (“Deck”). The Deck features a slide offering useful Zokinvy data. Slide 29 describes the extent of Zokinvy’s recognized sufferers as 20 within the US (the FDA approved it in 11/2020) and 20 in Europe:

eigerbio.com

Eiger doesn’t assist us to grasp the prospects for increasing past these 40 recognized sufferers. One article means that the market might embody as many as 600 sufferers.

I’ve been unable to find any firm recommendation on the seemingly peak revenues for Zokinvy. Actually it has issued nothing to counsel that there are a whole lot of potential sufferers.

Medical remedy — Lonafarnib/Ritonavir

Eiger’s lead pipeline remedy is its lonafarnib/ritonavir mixture remedy in remedy of hepatitis delta virus [HDV]. Slide 8 describes key attributes for this as follows:

- Solely oral agent in improvement;

- Orphan Designation in U.S. and EU;

- FDA Breakthrough Remedy Designation;

- patent safety via late-2030s.

Clinicaltrialls.gov lists two part 3 trials evaluating Lonafarnib/Ritonavirin remedy of HDV. Considered one of these, NCT03719313, is full with no outcomes posted. The second, NCT05229991, remains to be recruiting. Its temporary abstract describes it as:

Open label, single arm, multi-center medical trial of lonafarnib 50 mg QD plus ritonavir 200 mg QD, administered orally, over a 48-week remedy interval, with a 24-week post-treatment follow-up interval, in sufferers with persistent Hepatitis D Virus an infection.

Targets: To guage the security and tolerability of as soon as day by day dosing of lonafarnib 50 mg with ritonavir 200 mg over a 48-week remedy interval.

To guage the impact of as soon as day by day dosing of lonafarnib 50 mg with ritonavir 200 mg over a 48-week remedy interval with a 24-week post-treatment follow-up on HDV viral ranges.

Trial inhabitants: As much as 30 sufferers with persistent HDV an infection with detectable HDV RNA and compensated liver illness.

Medical remedy — Peginterferon lamda

Eiger’s second lead remedy can be directed at HDV. There are two clinicaltrialls.gov listed trials evaluating peginterferon lamda in remedy of HDV. Considered one of these, NCT02765802, is full with outcomes. The second, NCT05070364, remains to be recruiting. Its temporary abstract describes it as a:

…Part 3 LIMT-2 research will consider the security and efficacy of Peginterferon Lambda remedy for 48 weeks with 24 weeks follow-up in comparison with no remedy for 12 weeks in sufferers chronically contaminated with HDV. The first evaluation will evaluate the proportion of sufferers with HDV RNA < LLOQ on the 24-week post-treatment go to within the Peginterferon Lambda remedy group vs the proportion of sufferers with HDV RNA < LLOQ on the Week 12 go to within the no-treatment comparator group.

Its estimated major completion date is 06/15/2024 with an estimated research completion date of 01/15/2024.

Medical remedy —Avexitide

Avexitide is Eiger’s third and final pipeline medical remedy. Clinicaltrialls.gov lists three accomplished part 2 trials with outcomes evaluating avexitide. One, NCT04652479, evaluates it in remedy of acquired hyperinsulinemic hypoglycemia [HI]. The opposite two, NCT02771574 and NCT03373435 in remedy of postbariatric hypoglycemia [PBH].

The PBH trials had been each accomplished a number of years again. The HI trial was accomplished on 06/2022. For a motive unknown, Eiger appears to be slow-walking avexitide within the PBH indication.

The discharge signifies that it’s planning to reaccelerate HI advising “part 3 readiness actions initiated in HI program”. This reasonably cryptic recommendation falls effectively in need of offering a timeline. It does present consolation that avexitide in remedy of HI has not been completely forgotten. The identical cannot be mentioned for its PBH indication.

Conclusion

Eiger’s monetary scenario as disclosed by the Launch is dismal. It has its paltry Zokinvy revenues matched up in opposition to Q1, 2023 R&D bills of $16.7 million and SG&A bills of $9.5 million. It reported:

Money, money equivalents, and short-term debt securities as of March 31, 2023 totaled $75.3 million in comparison with $98.9 million as of December 31, 2022.

To ensure that Eiger to regain the >$2.00 value level that prevailed once I wrote Outcomes, administration goes to have get up. There are questions that demand solutions:

- does Zokinvy have potential to multiply its revenues to the purpose that they will contribute meaningfully to its hefty quarterly expense nut;

- was the market’s 12/2022 70% selloff in response to topline knowledge from its Part 3 D-LIVR research for lonafarnib in remedy of HDV an overreaction;

- in that case, why;

The Deck advises that Eiger plans a number of upcoming knowledge factors and a pre-NDA FDA assembly by finish of Q2. As I write on 06/15/2023, the top of Q2 is simply two weeks away. Count on massive value strikes on the close to horizon.

Optimistic value strikes will outcome from constructive information, significantly whether it is effectively delivered. Unhealthy information, or silence will seemingly see Eiger exploring new lows. Speculators line up. Make your bets. I can provide no handicap recommendation on this one.

One factor is for certain. Traders in Eiger ought to solely make investments cash that they’re ready to lose. Do not suppose for a minute that Wall Road Analysts’ consensus value goal is any sort of magnet. Regardless of how lengthy you’re ready to carry Eiger, it could by no means hit something near $4.00 and even the $2.00 it was once I wrote Outcomes.

Editor’s Observe: This text covers a number of microcap shares. Please concentrate on the dangers related to these shares.

{kind=link}