Liudmila Chernetska/iStock by way of Getty Photos

We’ve got beforehand coated AT&T Inc. (NYSE:T) in April 2023 here. At the moment, the inventory has been wrongfully sold-off, since its free money circulate technology has all the time been lumpy, relying on the timing of money distributions, capital expenditures, and money paid for vendor financing.

Given the optimistic indicators of working price optimization and improved profitability, we imagine the telecom might doubtlessly obtain its bold FCF technology of $16B in 2023. With the inventory already overly bought off as a result of Amazon (AMZN) rumor, we’re cautiously rerating the T inventory as a Purchase right here.

The Revenue Funding Thesis Appears to be like Extra Engaging Right here

T and Verizon Communications (VZ) have been not too long ago hammered by the rumors that AMZN could also be getting into the telecom area within the close to future. This growth is no surprise certainly, for the reason that latter has beforehand displayed bottomless ambitions in a number of markets.

This contains being a cloud provider by way of Amazon Internet Companies since 2000, groceries by way of Amazon Contemporary since 2007, unlimited streaming by way of Prime Instantaneous Video since 2011, primary healthcare by way of Amazon Care since 2019, the pharmacy service since 2020, and most not too long ago, the movie industry by way of the acquisition of MGM in 2021.

Most notably, we suppose this piece of rumor could also be a continuation of these mentioned since 2019, with AMZN supposedly focused on shopping for pay as you go cellphone wi-fi service, Enhance Cell, from T-Cell (TMUS) then. Both manner, with AMZN and TMUS already debunking the rumors, the coast has been all cleared for the rebound of T and VZ’s inventory costs.

Nonetheless, it seems TMUS continues to be affected by the baseless market rumor, with the inventory nonetheless down by -6.1% since June 02, 2023. The pessimism embedded in its inventory costs is shocking certainly, given its outperformance to date.

Maybe this is because of Mr. Market’s conviction that AMZN might ultimately enter the telecom market, placing nice competitors in opposition to the present telecom gamers, due to its 148.6M Prime members within the US. Nonetheless, we suppose that speculative occasion might solely happen by the second half of the last decade. That is why.

AMZN has been struggling to trim its working bills and return to profitability, as a result of overly aggressive enlargement in its footprints and headcounts throughout the hyper-pandemic interval. Even within the newest quarter, the e-commerce big solely reported 3.9% in working revenue margins, dramatically impacted in comparison with the hyper-pandemic heights of 5.9% in FY2020 and 5.2% in FY2019.

We suppose there’s minimal chance that AMZN might enter the telecom market now, the place competitors is intense, margins are skinny, and capex is elevated. Nonetheless, in the long run, it’s not overly speculative to think about the large ultimately taking up the MVNO technique, shopping for the telecoms’ spare capability at wholesale costs, as soon as the macroeconomic outlook normalizes.

This technique has been employed by smaller telecom gamers as properly, comparable to Mint Cell providing month-to-month cell plans from $15 and Consumer Cellular from $20 onwards. Whereas it’s unsure if the latter two are worthwhile, the enterprise might doubtlessly enhance AMZN’s Prime memberships, as a result of extremely aggressive costs of $10.

It’s already well-known that the e-commerce enterprise operates at razor-thin margins, with the pure revenue play embedded in its Prime memberships, considerably aided by the AWS phase. This can be a comparable technique that we have now noticed with Costco (COST).

We suppose a part of the pessimism can be attributed to T’s lumpy free cash flow at $1B (-83.6% QoQ/ +42.8% YoY) and elevated long-term money owed of $137.5B (+1.1% QoQ and -33.7% YoY), regardless of the strong annualized adj. EBITDA of $42.32B (+3.8% YoY).

In the meantime, VZ isn’t any higher with a free money circulate of $2.33B (+37% QoQ/ +133% YoY) and long-term debts of $140.77B (inline QoQ/ +0.5% YoY), with stagnant FY2023 adj EBITDA steerage of $47.75B on the midpoint (inline YoY).

A lot of the impacted money circulate is attributed to T’s elevated capital expenditure of $19.39B (+17.7% sequentially) and sustained dividend payout of $15.05B (-46.04% sequentially) over the past twelve months, leaving little for debt reimbursement.

The identical has been reported by VZ at capital expenditures of $23.22B (+7.5% sequentially) and a dividend payout of $10.89B (+4% sequentially) over the past twelve months. Whereas TMUS doesn’t pay out dividends, it’s obvious that the telecom enterprise is capex intensive, with the latter equally reporting $13.59B (+8.6% sequentially) of capital expenditures over the past twelve months.

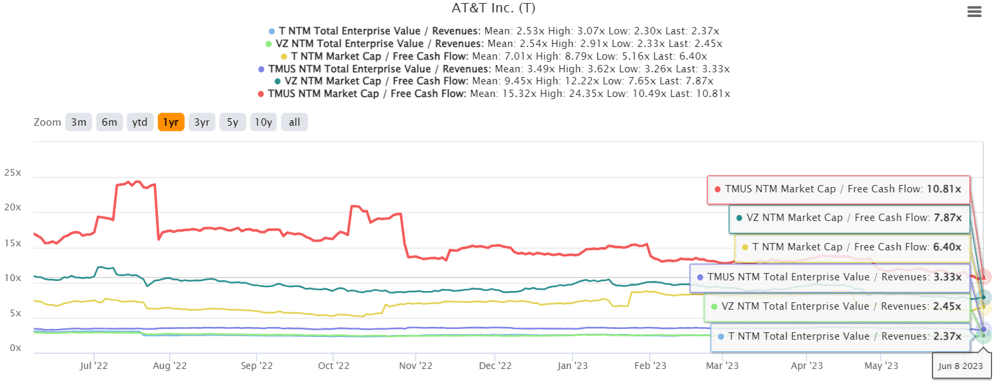

T, VZ, & TMUS 5Y EV/Income and NTM Market Cap/FCF

S&P Capital IQ

This cadence could also be why their shares’ valuations have been moderated to date, with T buying and selling at NTM Market Cap/ Free Money Circulate of 6.40x, VZ at 7.87x, and TMUS at 10.81x, in comparison with their 5Y imply of 8.44x, 11.87x, and 23.29x, respectively. Their NTM EV/ Revenues stays stagnant over the previous 5 years as properly, suggesting their sluggish top-line development forward.

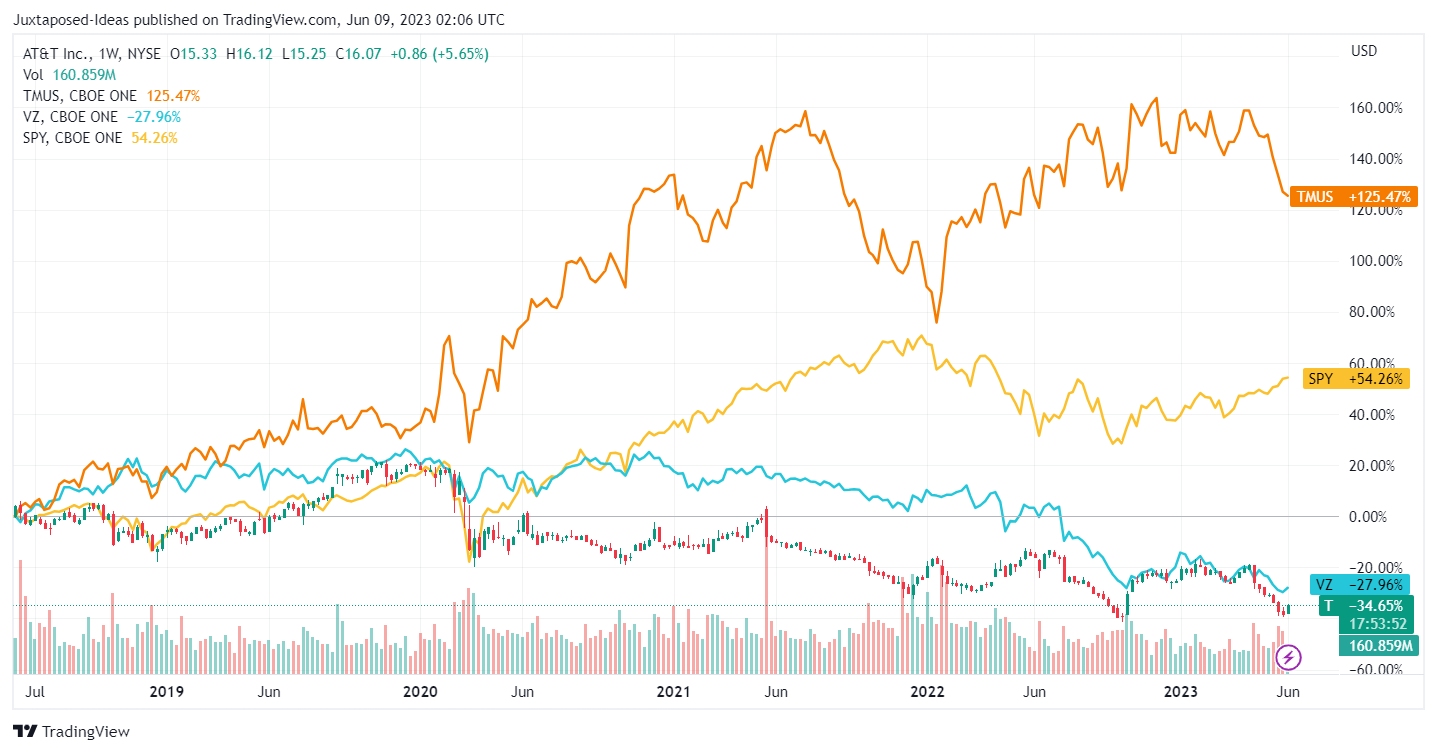

T, VZ, & TMUS 5Y Inventory Value

Buying and selling View

Nonetheless, if traders are searching for high-growth telecom inventory, they might have a look at TMUS as an alternative, as a result of spectacular 5Y returns at +125.47%. Whereas previous efficiency will not be indicative of ahead returns, the T and VZ inventory has additionally underperformed in opposition to the broader market, even when we’re to incorporate their dividends.

Then once more, we proceed to charge each T and VZ shares as buys right here, as a consequence of their oversold ranges, with T buying and selling at its 2008 lows and VZ equally at its 2011 lows.

The market rumor has triggered way more engaging entry factors for income-seeking traders, in our view, with T now providing a superb ahead dividend yield of 6.89% and VZ at 7.40%, in comparison with their 4Y common yields of 6.94% and 4.94%, respectively.

Naturally, traders should additionally modify their expectations accordingly, since these two shares might proceed their underperformance for the foreseeable future, with their solely benefit being the wealthy dividend yields. Even then, assuming that AMZN actually enters the foray, we might even see the legacy telecoms’ EBITDA negatively impacted, doubtlessly triggering a dividend reduce then.

Solely time might inform.

{kind=link}