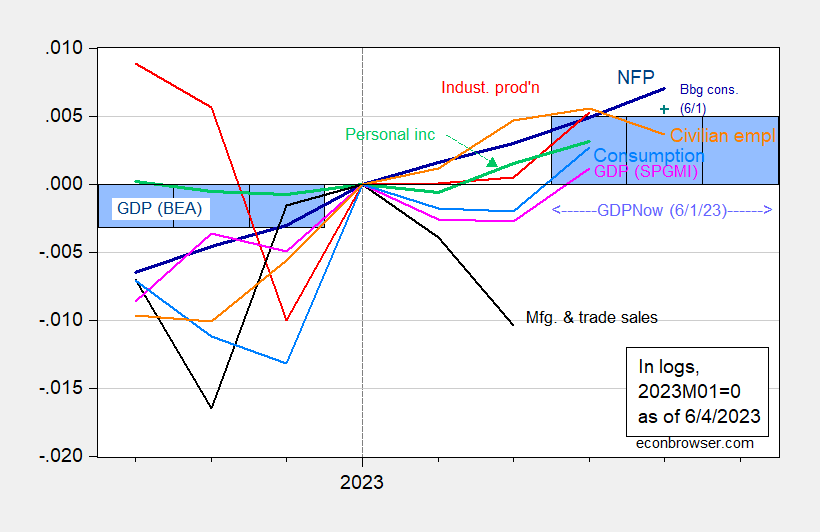

New Deal Democrat suggests normalizing on 2023M01 as a substitute of to 2022M11. Right here’re the NBER BCDC indicators, plus month-to-month GDP, in addition to a slew of others, since then.

Determine 1: Nonfarm payroll employment, NFP (darkish blue), Bloomberg consensus of 6/1 (blue +), civilian employment (orange), industrial manufacturing (crimson), private earnings excluding transfers in Ch.2012$ (inexperienced), manufacturing and commerce gross sales in Ch.2012$ (black), consumption in Ch.2012$ (gentle blue), and month-to-month GDP in Ch.2012$ (pink), GDP (blue bars), 2023Q1 is GDPNow of 6/1, all log normalized to 2023M01=0. Bloomberg consensus stage calculated by including forecasted change to earlier unrevised stage of employment obtainable at time of forecast. Supply: BLS, Federal Reserve, BEA 2023Q1 2nd launch by way of FRED, Atlanta Fed, S&P Global/IHS Markit (nee Macroeconomic Advisers, IHS Markit) (6/1/2023 launch), and writer’s calculations.

As New Deal Democrat factors out, NFP and private earnings aren’t as clearly rising as when normalized to 2022M01. They’re, nonetheless, nonetheless rising (CPS collection civilian employment is falling Could, however as famous elsewhere, one shouldn’t put an excessive amount of weight on this collection given its volatility). Notice GDPNow development as of 6/1 (so utilizing information from 2/3 of quarter 2) is constructive, at 2% q/q SAAR.

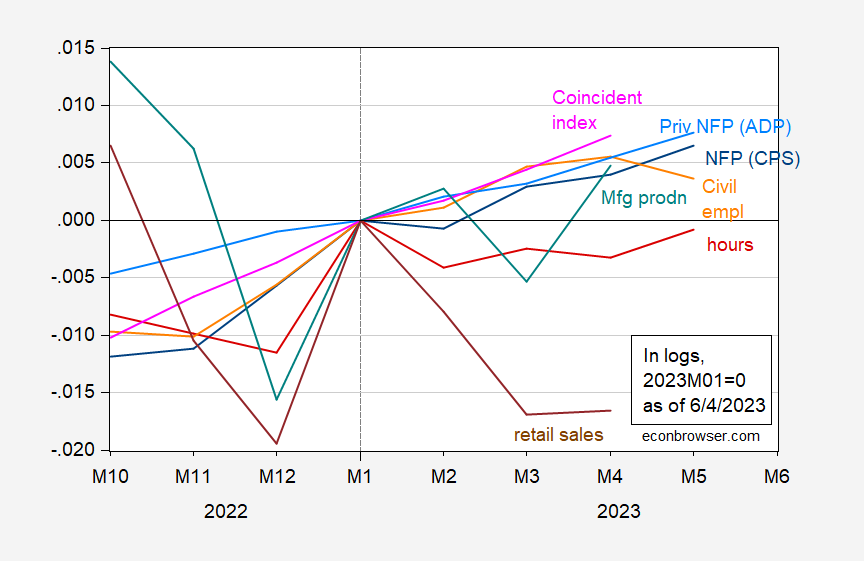

And various collection.

Determine 2: Civilian employment adjusted to nonfarm payroll employment idea (darkish blue), non-public nonfarm payroll employment from ADP (sky blue), civilian employment (orange), combination weekly hours for manufacturing and nonsupervisory employees (crimson), manufacturing manufacturing (teal), coincident index (teal), retail gross sales ex-food companies deflated by CPI (brown), all log normalized to 2023M01=0. Bloomberg consensus stage calculated by including forecasted change to earlier unrevised stage of employment obtainable at time of forecast. Supply: BLS, Federal Reserve, and Philadelphia Fed by way of FRED, and writer’s calculations.

Combination hours are certainly down barely. Retail gross sales too, though that collection is kind of risky. This collection has been trending downward since 2022M04.

So, taking a look at a shorter interval, one would possibly be capable of infer a deceleration extra clearly.

New Deal Democrat suggests normalizing on 2023M01 as a substitute of to 2022M11. Right here’re the NBER BCDC indicators, plus month-to-month GDP, in addition to a slew of others, since then.

Determine 1: Nonfarm payroll employment, NFP (darkish blue), Bloomberg consensus of 6/1 (blue +), civilian employment (orange), industrial manufacturing (crimson), private earnings excluding transfers in Ch.2012$ (inexperienced), manufacturing and commerce gross sales in Ch.2012$ (black), consumption in Ch.2012$ (gentle blue), and month-to-month GDP in Ch.2012$ (pink), GDP (blue bars), 2023Q1 is GDPNow of 6/1, all log normalized to 2023M01=0. Bloomberg consensus stage calculated by including forecasted change to earlier unrevised stage of employment obtainable at time of forecast. Supply: BLS, Federal Reserve, BEA 2023Q1 2nd launch by way of FRED, Atlanta Fed, S&P Global/IHS Markit (nee Macroeconomic Advisers, IHS Markit) (6/1/2023 launch), and writer’s calculations.

As New Deal Democrat factors out, NFP and private earnings aren’t as clearly rising as when normalized to 2022M01. They’re, nonetheless, nonetheless rising (CPS collection civilian employment is falling Could, however as famous elsewhere, one shouldn’t put an excessive amount of weight on this collection given its volatility). Notice GDPNow development as of 6/1 (so utilizing information from 2/3 of quarter 2) is constructive, at 2% q/q SAAR.

And various collection.

Determine 2: Civilian employment adjusted to nonfarm payroll employment idea (darkish blue), non-public nonfarm payroll employment from ADP (sky blue), civilian employment (orange), combination weekly hours for manufacturing and nonsupervisory employees (crimson), manufacturing manufacturing (teal), coincident index (teal), retail gross sales ex-food companies deflated by CPI (brown), all log normalized to 2023M01=0. Bloomberg consensus stage calculated by including forecasted change to earlier unrevised stage of employment obtainable at time of forecast. Supply: BLS, Federal Reserve, and Philadelphia Fed by way of FRED, and writer’s calculations.

Combination hours are certainly down barely. Retail gross sales too, though that collection is kind of risky. This collection has been trending downward since 2022M04.

So, taking a look at a shorter interval, one would possibly be capable of infer a deceleration extra clearly.

{kind=link}