Right this moment’s jobs report contained two items of knowledge that recommend coverage could also be a bit too expansionary. First, payroll employment rose by a stronger than anticipated 272,000. (The family survey was weak, however that information is seen as much less dependable.) Second, nominal wages grew at 0.4% (an annual charge of almost 5%.) If you happen to assume when it comes to the Fed’s twin mandate, each information factors barely tilt issues towards the view that coverage is simply too expansionary. That doesn’t imply that we might be sure that coverage is simply too expansionary, simply that this declare is now a bit extra more likely to be true.

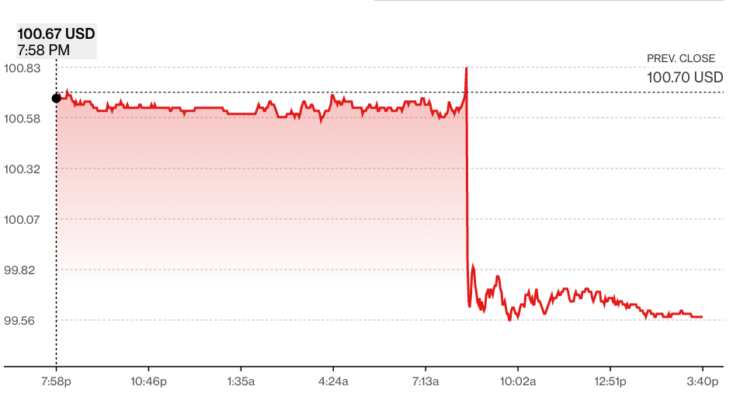

The ten-year T-bond market reacted with a sell-off, which signifies that longer-term rates of interest elevated:

Markets at present anticipate a Fed charge lower later this 12 months. This would possibly happen as a result of inflation declines, or as a result of the true financial system is at risk of sliding into recession. Right this moment’s information made each of these outcomes appear a bit much less doubtless. Wage inflation has averaged 4.1% over the previous 12 months, a charge that isn’t according to the Fed’s “value stability” targets, even when you outline value stability as 2% inflation. Over time, wage inflation tends to run about 1% to 1.5% above value inflation. Sadly, progress on lowering wage inflation appears to have stalled over the previous 10 months. The following two or three readings shall be crucial.

I would not have robust views on the place the Fed ought to set its rate of interest goal in the meanwhile. I do have robust views on previous financial coverage, which has been far too expansionary over the previous three years. The longer these coverage overshoots final, the stronger the case for switching to a degree focusing on coverage regime, the place the Fed would decide to make up for earlier coverage errors. I had thought they supposed to try this again in 2020, but it surely seems that “common inflation focusing on” was not an correct description of their new coverage regime.

This publish is entitled “double hassle”, though the payroll employment determine might be considered excellent news. The figures are hassle for a Fed that appears to be hoping that they may quickly be capable to decrease their goal rate of interest. For my part, it’s a mistake for the central financial institution to root for decrease rates of interest, simply because it was a mistake for the Fed to favor larger rates of interest again in 2015. They need to not favor both decrease or larger rates of interest; they need to favor macroeconomic (nominal) stability. Let the market resolve what kind of rates of interest are according to macro stability.

PS. This remark in the FT caught my eye:

Jason Furman, a former administration official now at Harvard College, stated the uptick in joblessness may very well be a very powerful a part of Friday’s information launch.

“If we get up subsequent month and the unemployment charge is 4.1 per cent, I believe that can get [the Fed’s] consideration,” Furman stated. “When you’ve got an unemployment that’s above 4, that might put a charge lower in play earlier.”

Within the Seventies, the Fed assumed {that a} rising unemployment charge was an indication that cash was too tight. That was not the case. The Fed ought to by no means goal the unemployment charge, as nobody is aware of precisely what the pure charge of unemployment is at any given second in time. The Fed ought to goal a nominal variable, preferable nominal GDP. It’s usually true that rising unemployment is a sign that simpler cash is required, however not if NGDP is rising at 5%.

Right this moment’s jobs report contained two items of knowledge that recommend coverage could also be a bit too expansionary. First, payroll employment rose by a stronger than anticipated 272,000. (The family survey was weak, however that information is seen as much less dependable.) Second, nominal wages grew at 0.4% (an annual charge of almost 5%.) If you happen to assume when it comes to the Fed’s twin mandate, each information factors barely tilt issues towards the view that coverage is simply too expansionary. That doesn’t imply that we might be sure that coverage is simply too expansionary, simply that this declare is now a bit extra more likely to be true.

The ten-year T-bond market reacted with a sell-off, which signifies that longer-term rates of interest elevated:

Markets at present anticipate a Fed charge lower later this 12 months. This would possibly happen as a result of inflation declines, or as a result of the true financial system is at risk of sliding into recession. Right this moment’s information made each of these outcomes appear a bit much less doubtless. Wage inflation has averaged 4.1% over the previous 12 months, a charge that isn’t according to the Fed’s “value stability” targets, even when you outline value stability as 2% inflation. Over time, wage inflation tends to run about 1% to 1.5% above value inflation. Sadly, progress on lowering wage inflation appears to have stalled over the previous 10 months. The following two or three readings shall be crucial.

I would not have robust views on the place the Fed ought to set its rate of interest goal in the meanwhile. I do have robust views on previous financial coverage, which has been far too expansionary over the previous three years. The longer these coverage overshoots final, the stronger the case for switching to a degree focusing on coverage regime, the place the Fed would decide to make up for earlier coverage errors. I had thought they supposed to try this again in 2020, but it surely seems that “common inflation focusing on” was not an correct description of their new coverage regime.

This publish is entitled “double hassle”, though the payroll employment determine might be considered excellent news. The figures are hassle for a Fed that appears to be hoping that they may quickly be capable to decrease their goal rate of interest. For my part, it’s a mistake for the central financial institution to root for decrease rates of interest, simply because it was a mistake for the Fed to favor larger rates of interest again in 2015. They need to not favor both decrease or larger rates of interest; they need to favor macroeconomic (nominal) stability. Let the market resolve what kind of rates of interest are according to macro stability.

PS. This remark in the FT caught my eye:

Jason Furman, a former administration official now at Harvard College, stated the uptick in joblessness may very well be a very powerful a part of Friday’s information launch.

“If we get up subsequent month and the unemployment charge is 4.1 per cent, I believe that can get [the Fed’s] consideration,” Furman stated. “When you’ve got an unemployment that’s above 4, that might put a charge lower in play earlier.”

Within the Seventies, the Fed assumed {that a} rising unemployment charge was an indication that cash was too tight. That was not the case. The Fed ought to by no means goal the unemployment charge, as nobody is aware of precisely what the pure charge of unemployment is at any given second in time. The Fed ought to goal a nominal variable, preferable nominal GDP. It’s usually true that rising unemployment is a sign that simpler cash is required, however not if NGDP is rising at 5%.

{kind=link}