Yesterday we pointed to a put up by Gary Smith, “Don’t worship math: Numbers don’t equal perception,” subtitled, “The unwarranted assumption that investing in shares is like rolling cube has led to some misguided conclusions and terribly conservative recommendation,” that included an exquisite story that makes the legendary economist Paul Samuelson seem like a pompous idiot. Right here’s Smith:

Mathematical comfort has typically trumped frequent sense in monetary fashions. For instance, it’s typically assumed — as a result of the idea is beneficial — that modifications in inventory costs will be modeled as impartial attracts from a likelihood distribution. Paul Samuelson supplied this analogy:

Write down these 1,800 share modifications in month-to-month inventory costs on as many slips of paper. Put them in a giant hat. Shake vigorously. Then draw at random a brand new couple of thousand tickets, every time changing the final draw and shaking vigorously. That manner we will generate new realistically consultant attainable histories of future fairness markets.

I [Smith] did Samuelson’s experiment. I put 100 years of month-to-month returns for the S&P 500 in a pc “hat” and had the pc randomly choose month-to-month returns (with alternative) till I had a attainable 25-year historical past. I repeated the experiment a million instances, giving a million “Samuelson simulations.”

I additionally checked out each attainable beginning month within the historic knowledge and decided the very worst and perfect precise 25-year funding durations. The worst interval started in September 1929, initially of the Nice Crash. An funding over the following 25 years would have had an annual return of 5.1%. The very best beginning month was January 1975, after the 1973-1974 crash. The annual charge of return over the following 25 years was 17.3%.

Within the a million Samuelson simulations, 9.6% of the simulations gave 25-year returns that had been worse than any 25-year interval within the historic knowledge and 4.9% of the simulations gave 25-year returns that had been higher than any precise 25-year historic interval. General, 14.5% of the Samuelson simulations gave 25-year returns that had been too excessive. Over a 50-year horizon, 24.5% of the Samuelson simulations gave 50-year returns that had been extra excessive than something that has ever been skilled.

You may say that Smith is being unfair, as Samuelson was solely providing a easy mathematical mannequin. But it surely was Samuelson, not Smith, who characterised his random drawing as “realistically consultant attainable histories of future fairness markets.” Samuelson was the one claiming realism.

My take is that Samuelson needed it each methods. He needed to indicate off his math, however he additionally needed relevance, therefore his “realistically.”

The status of economics comes partly from its mathematical sophistication however principally as a result of it’s imagined to relate to the actual world.

Smith’s instance of Samuelson’s error jogged my memory of this story from David Levy and Sandra Peart of this graph from the legendary textbook. That is from 1961:

Alex Tabarrok identified that it’s even worse than it appears to be like: “in subsequent editions Samuelson offered the identical evaluation time and again besides the overtaking time was at all times pushed additional into the long run so by 1980 the dates had been 2002 to 2012. In subsequent editions, Samuelson supplied no acknowledgment of his previous failure to foretell and little commentary past remarks about ‘unhealthy climate’ within the Soviet Union.”

The bit in regards to the unhealthy climate is humorous. If you happen to’ve had unhealthy climate prior to now, possibly the potential of future unhealthy climate needs to be included into the forecast, no?

Is there a connection?

Can we join Samuelson’s two errors?

Once more, the error with the Soviet financial system forecast is just not that he was improper within the frenzied post-Sputnik 12 months of 1961; the issue is that he saved making this error in his textbook for many years to come back. Here’s one other bit, from Larry White:

As late because the 1989 version [Samuelson] coauthor William Nordhaus wrote: ‘The Soviet financial system is proof that, opposite to what many skeptics had earlier believed, a socialist command financial system can perform and even thrive.’

I see three similarities between the stock-market error and the command-economy error:

1. Love of straightforward mathematical fashions: the random stroll in a single case and straight developments within the different. The mannequin’s so fairly, it’s too good to test.

2. Disregard of information. Smith did that experiment disproving Samuelson’s declare. Samuelson may’ve completed that experiment himself! However he didn’t. That didn’t cease him from making a assured declare about it. As for the Soviet Union, by the point 1980 had come alongside Samuelson had 20 years of information refuting his unique mannequin, however that didn’t cease him from simply shifting the rattling curve. No sense that, hey, possibly the mannequin has an issue!

3. Technocratic hubris. There’s this complete story about how Samuelson was so good. I don’t know how good he was—possibly requirements had been decrease again then?—however math and actuality don’t care how good you might be. I see a connection between Samuelson considering that he may describe the inventory market with a easy random stroll mannequin, and him considering that the Soviets may simply pull some levers and run a thriving financial system. Put the specialists in cost, what may go improper, huh?

Extra tales

Smith writes:

As a scholar, Samuelson reportedly terrorized his professors along with his withering criticisms.

Samuelson is after all the uncle of Larry Summers, one other never-admit-a-mistake man. There’s a story about Summers saying one thing silly to Samuelson every week earlier than Arthur Okun’s funeral. Samuelson reportedly mentioned to Summers, “In my eulogy for Okun, I’m going to say that I don’t bear in mind him ever saying something silly. Nicely, now I received’t have the ability to say that about you.”

There was a well-known feud between Samuelson and Harry Markowitz about whether or not traders ought to take into consideration arithmetic or geometric means. In a single Samuelson paper responding to Markowitz, each phrase (apart from creator names) was single syllable.

I as soon as gave a paper at a festschrift honoring Tobin. Markowitz started his speak by graciously saying to Samuelson, who was sitting arm-crossed within the entrance row, “Within the spirit of this joyous event, I wish to say to Paul that ‘Maybe there may be some benefit in your argument.’” Samuelson instantly responded, “I want I may say the identical.”

Here’s the words-of-one-syllable paper, and right here’s a put up that Smith discovered:

Possibly Samuelson and his coauthors ought to’ve spent much less time on dominance video games and “boss strikes” and extra time truly looking on the world that they had been purportedly describing.

Yesterday we pointed to a put up by Gary Smith, “Don’t worship math: Numbers don’t equal perception,” subtitled, “The unwarranted assumption that investing in shares is like rolling cube has led to some misguided conclusions and terribly conservative recommendation,” that included an exquisite story that makes the legendary economist Paul Samuelson seem like a pompous idiot. Right here’s Smith:

Mathematical comfort has typically trumped frequent sense in monetary fashions. For instance, it’s typically assumed — as a result of the idea is beneficial — that modifications in inventory costs will be modeled as impartial attracts from a likelihood distribution. Paul Samuelson supplied this analogy:

Write down these 1,800 share modifications in month-to-month inventory costs on as many slips of paper. Put them in a giant hat. Shake vigorously. Then draw at random a brand new couple of thousand tickets, every time changing the final draw and shaking vigorously. That manner we will generate new realistically consultant attainable histories of future fairness markets.

I [Smith] did Samuelson’s experiment. I put 100 years of month-to-month returns for the S&P 500 in a pc “hat” and had the pc randomly choose month-to-month returns (with alternative) till I had a attainable 25-year historical past. I repeated the experiment a million instances, giving a million “Samuelson simulations.”

I additionally checked out each attainable beginning month within the historic knowledge and decided the very worst and perfect precise 25-year funding durations. The worst interval started in September 1929, initially of the Nice Crash. An funding over the following 25 years would have had an annual return of 5.1%. The very best beginning month was January 1975, after the 1973-1974 crash. The annual charge of return over the following 25 years was 17.3%.

Within the a million Samuelson simulations, 9.6% of the simulations gave 25-year returns that had been worse than any 25-year interval within the historic knowledge and 4.9% of the simulations gave 25-year returns that had been higher than any precise 25-year historic interval. General, 14.5% of the Samuelson simulations gave 25-year returns that had been too excessive. Over a 50-year horizon, 24.5% of the Samuelson simulations gave 50-year returns that had been extra excessive than something that has ever been skilled.

You may say that Smith is being unfair, as Samuelson was solely providing a easy mathematical mannequin. But it surely was Samuelson, not Smith, who characterised his random drawing as “realistically consultant attainable histories of future fairness markets.” Samuelson was the one claiming realism.

My take is that Samuelson needed it each methods. He needed to indicate off his math, however he additionally needed relevance, therefore his “realistically.”

The status of economics comes partly from its mathematical sophistication however principally as a result of it’s imagined to relate to the actual world.

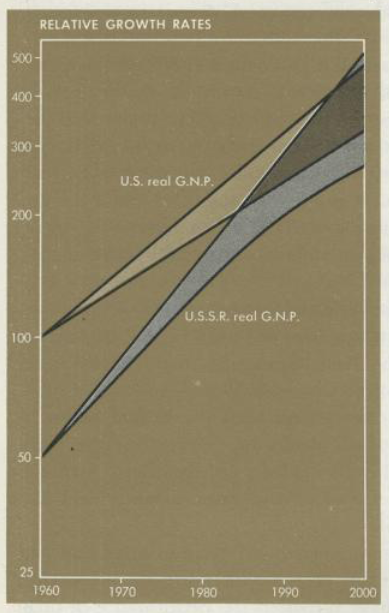

Smith’s instance of Samuelson’s error jogged my memory of this story from David Levy and Sandra Peart of this graph from the legendary textbook. That is from 1961:

Alex Tabarrok identified that it’s even worse than it appears to be like: “in subsequent editions Samuelson offered the identical evaluation time and again besides the overtaking time was at all times pushed additional into the long run so by 1980 the dates had been 2002 to 2012. In subsequent editions, Samuelson supplied no acknowledgment of his previous failure to foretell and little commentary past remarks about ‘unhealthy climate’ within the Soviet Union.”

The bit in regards to the unhealthy climate is humorous. If you happen to’ve had unhealthy climate prior to now, possibly the potential of future unhealthy climate needs to be included into the forecast, no?

Is there a connection?

Can we join Samuelson’s two errors?

Once more, the error with the Soviet financial system forecast is just not that he was improper within the frenzied post-Sputnik 12 months of 1961; the issue is that he saved making this error in his textbook for many years to come back. Here’s one other bit, from Larry White:

As late because the 1989 version [Samuelson] coauthor William Nordhaus wrote: ‘The Soviet financial system is proof that, opposite to what many skeptics had earlier believed, a socialist command financial system can perform and even thrive.’

I see three similarities between the stock-market error and the command-economy error:

1. Love of straightforward mathematical fashions: the random stroll in a single case and straight developments within the different. The mannequin’s so fairly, it’s too good to test.

2. Disregard of information. Smith did that experiment disproving Samuelson’s declare. Samuelson may’ve completed that experiment himself! However he didn’t. That didn’t cease him from making a assured declare about it. As for the Soviet Union, by the point 1980 had come alongside Samuelson had 20 years of information refuting his unique mannequin, however that didn’t cease him from simply shifting the rattling curve. No sense that, hey, possibly the mannequin has an issue!

3. Technocratic hubris. There’s this complete story about how Samuelson was so good. I don’t know how good he was—possibly requirements had been decrease again then?—however math and actuality don’t care how good you might be. I see a connection between Samuelson considering that he may describe the inventory market with a easy random stroll mannequin, and him considering that the Soviets may simply pull some levers and run a thriving financial system. Put the specialists in cost, what may go improper, huh?

Extra tales

Smith writes:

As a scholar, Samuelson reportedly terrorized his professors along with his withering criticisms.

Samuelson is after all the uncle of Larry Summers, one other never-admit-a-mistake man. There’s a story about Summers saying one thing silly to Samuelson every week earlier than Arthur Okun’s funeral. Samuelson reportedly mentioned to Summers, “In my eulogy for Okun, I’m going to say that I don’t bear in mind him ever saying something silly. Nicely, now I received’t have the ability to say that about you.”

There was a well-known feud between Samuelson and Harry Markowitz about whether or not traders ought to take into consideration arithmetic or geometric means. In a single Samuelson paper responding to Markowitz, each phrase (apart from creator names) was single syllable.

I as soon as gave a paper at a festschrift honoring Tobin. Markowitz started his speak by graciously saying to Samuelson, who was sitting arm-crossed within the entrance row, “Within the spirit of this joyous event, I wish to say to Paul that ‘Maybe there may be some benefit in your argument.’” Samuelson instantly responded, “I want I may say the identical.”

Here’s the words-of-one-syllable paper, and right here’s a put up that Smith discovered:

Possibly Samuelson and his coauthors ought to’ve spent much less time on dominance video games and “boss strikes” and extra time truly looking on the world that they had been purportedly describing.

{kind=link}