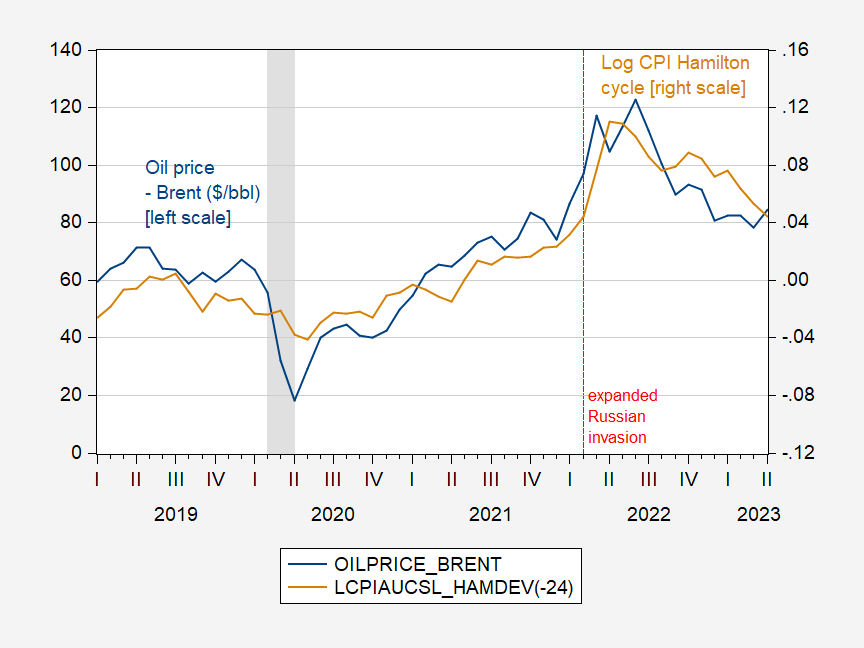

Reader Erik Poole suggests utilizing the Hamilton filter as an alternative of the Hodrick-Prescott filter, in assessing how a lot the CPI deviated from pattern (recall, i noted that the CPI rose 2% vs trend at the same time as oil prices were elevated, before and after the expanded Russian invasion of Ukraine). I’m (greater than) pleased to oblige.

Determine 1: Oil value (Brent), $/bbl (blue, left scale), and CPI deviation from pattern (Hamilton filter) (tan, proper scale). NBER outlined peak-to-trough recession dates shaded grey. Supply: EIA, BLS by way of FRED, NBER, and writer’s calculations.

I applied the Hamilton filter with h=24, p=12. The HP cyclical part rose 2.1% from November 2011 to June 2022, whereas the Hamilton filter signifies a 7.7% enhance. That is in step with my conjecture that generally, estimated cyclical parts had been bigger for most common US macro sequence.

Clearly, correlation shouldn’t be causation; specifically, a joint issue is that elevated oil costs are related to elevated mixture demand, which itself (within the context of fastened or depressed mixture provide) would elevate costs by way of the straightforward Phillips Curve. Nevertheless, I feel all would agree not less than a big share of the power part of CPI-all is related to cost-push inflationary pressures.

{kind=link}