NoDerog

In my December 2022 evaluation, I put a hold rating on the J.M. Smucker Firm (NYSE:SJM) and prompt promoting lined calls to generate additional revenue. The inventory has carried out as anticipated since that decision, down 2.4% on a complete return foundation in comparison with an 8.8% return for the S&P 500 Index (SP500). The corporate’s margins are enhancing, its stock prices are beneath management, and its CapEx must be decrease subsequent 12 months, resulting in improved money flows. In comparison with different client staples shares, lots of that are buying and selling at a stratospheric valuation, the inventory is just a tad overvalued however trades consistent with its friends, corresponding to Campbell Soup (CPB). Lengthy-term traders might think about shopping for the inventory near a 10x EV to EBITDA a number of, at or beneath $135.

Towards all odds, double-digit value will increase proceed driving gross sales development

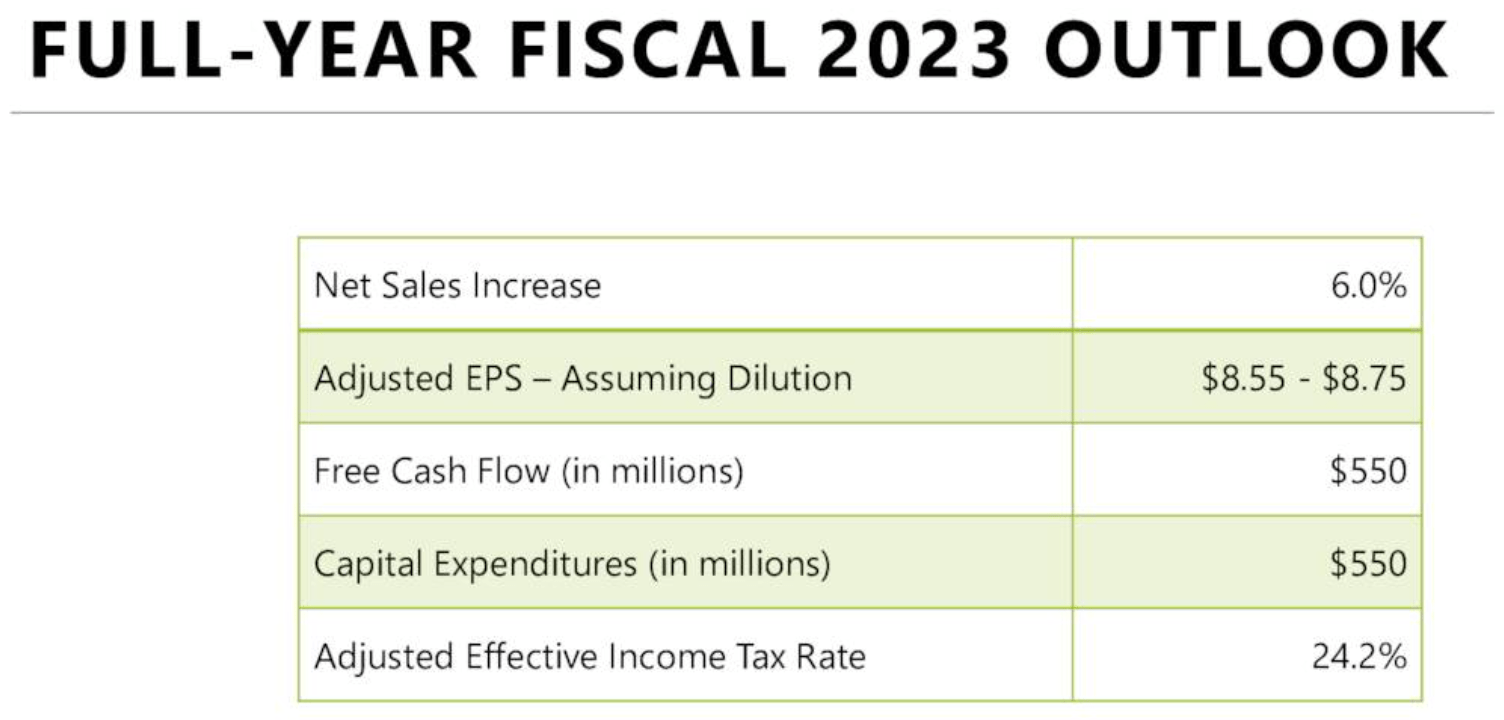

I’m stunned by the buyer’s resilience within the face of inflation. Many corporations within the Client Staples sector have seen lower cost elasticities, with double-digit value will increase leading to a decline in single-digit quantity, and the third quarter showcased one other instance of decrease elasticities. The corporate increased prices by 15% whereas volumes declined by 4%. Within the second quarter, the corporate raised costs by 17% whereas the quantity declined by 6%. The corporate noticed an analogous story within the first quarter, with a 14% value improve matched by a 9% quantity decline. The corporate expects a 6% development in gross sales in fiscal 12 months 2023 (Exhibit 1). Administration has considerably elevated its CapEx in 2023 and would spend its highest quantity ever with an funding of $550 million. This CapEx will support the manufacturing expansion of its Uncrustables model in Alabama. This substantial improve in CapEx has drastically reduce its working money movement in 2023.

Exhibit 1:

The J.M. Smucker Firm Fiscal 2023 Outlook (The J.M. Smucker Firm Investor Presentation)

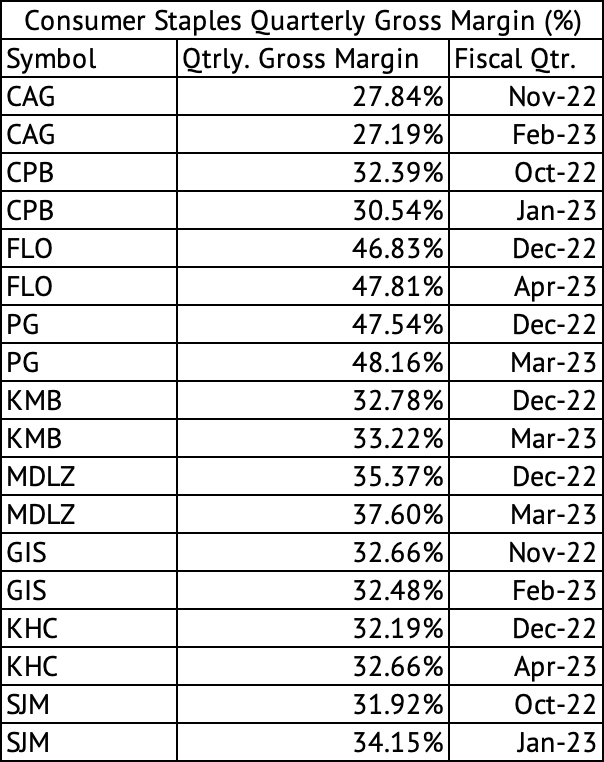

Customers have continued spending with restricted hits to gross sales volumes. Most corporations within the Client Staples sector have seen their gross margins enhance as inflation fades whereas value will increase stay sticky. Flowers Meals (FLO), Procter & Gamble (PG), Kimberly-Clark (KMB), Mondelez Worldwide (MDLZ), Kraft Heinz (KHC), and J.M. Smucker have improved their margins q/q (Exhibit 2).

Exhibit 2:

Quarterly Gross Margins for Client Staples Firms (Searching for Alpha, Creator Compilation)

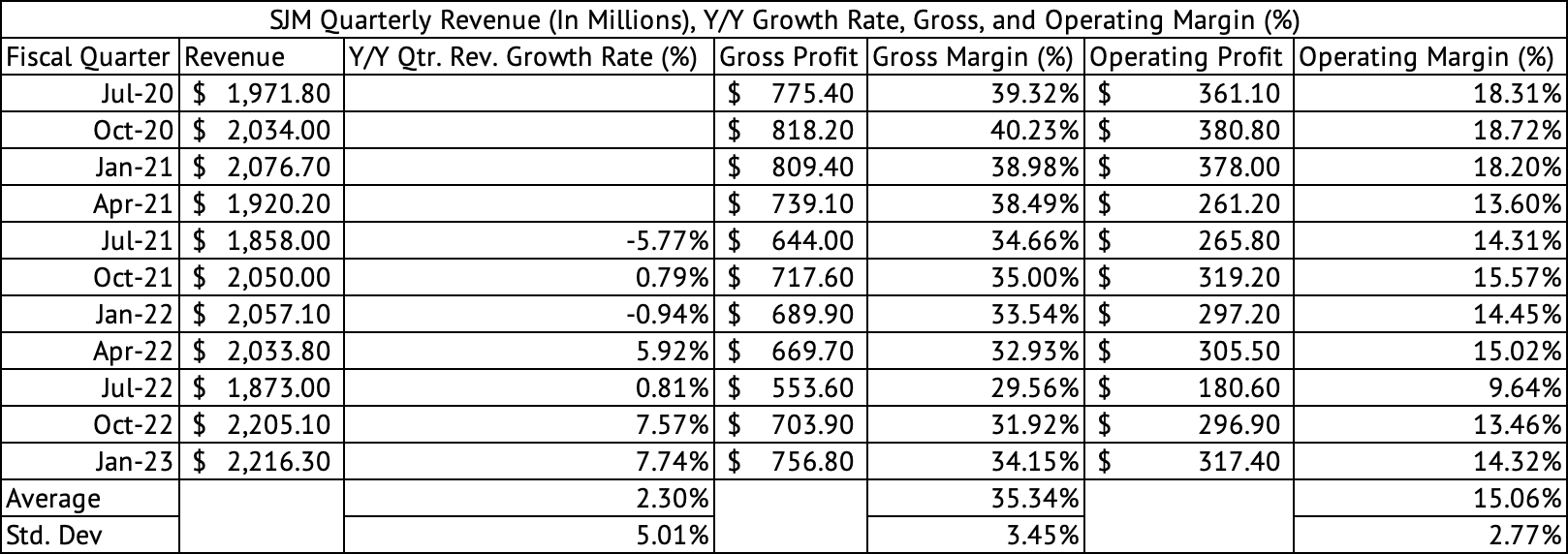

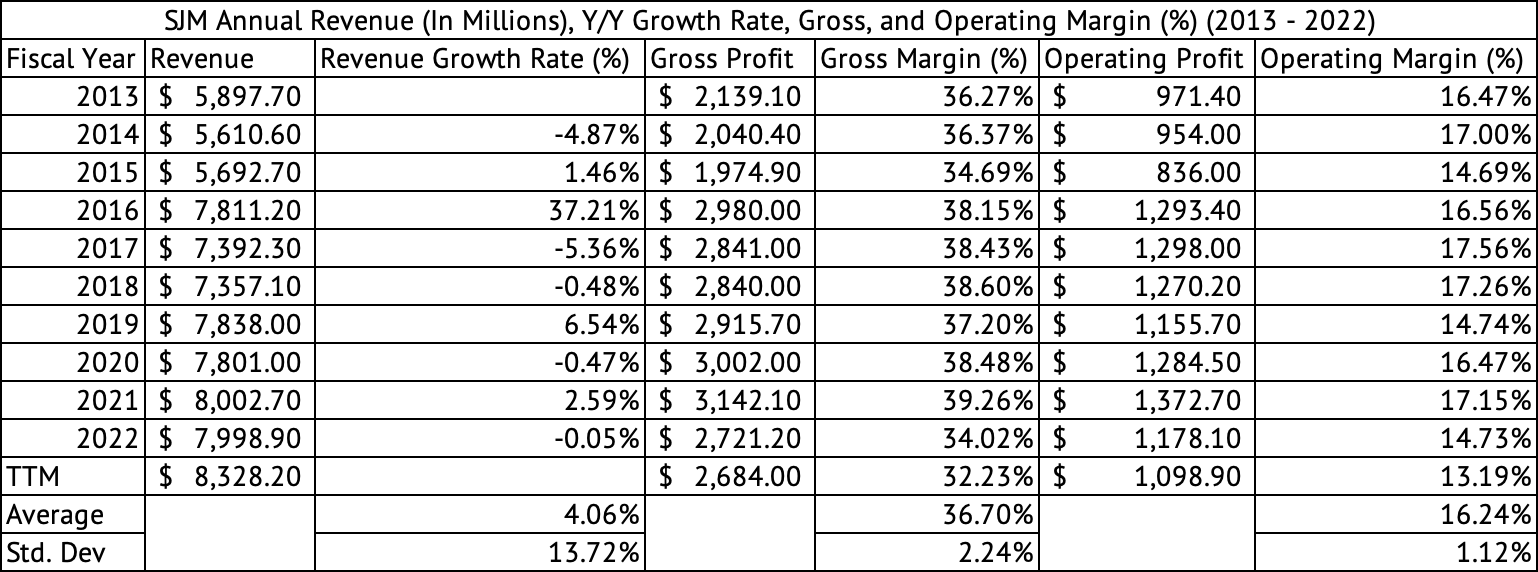

The J.M. Smucker Firm has averaged a quarterly gross margin of 35.3% since July 2020 and a mean annual gross margin of 36.7% (Displays 3 & 4). The corporate has some methods to go to attain its common gross margins. However, with provide chains returning to regular, enter value inflation is fading slowly; if the demand does not deteriorate additional, the corporate ought to return to its common gross margins within the coming quarters.

Exhibit 3:

The J.M. Smucker Firm Quarterly Income, Gross, Working Revenue, and Margins (%) (Searching for Alpha, Creator Compilation)

Exhibit 4:

The J.M. Smucker Firm Annual Income, Gross, Working Revenue, and Margins (%) (Searching for Alpha, Creator Compilation)

Inventories are beneath management

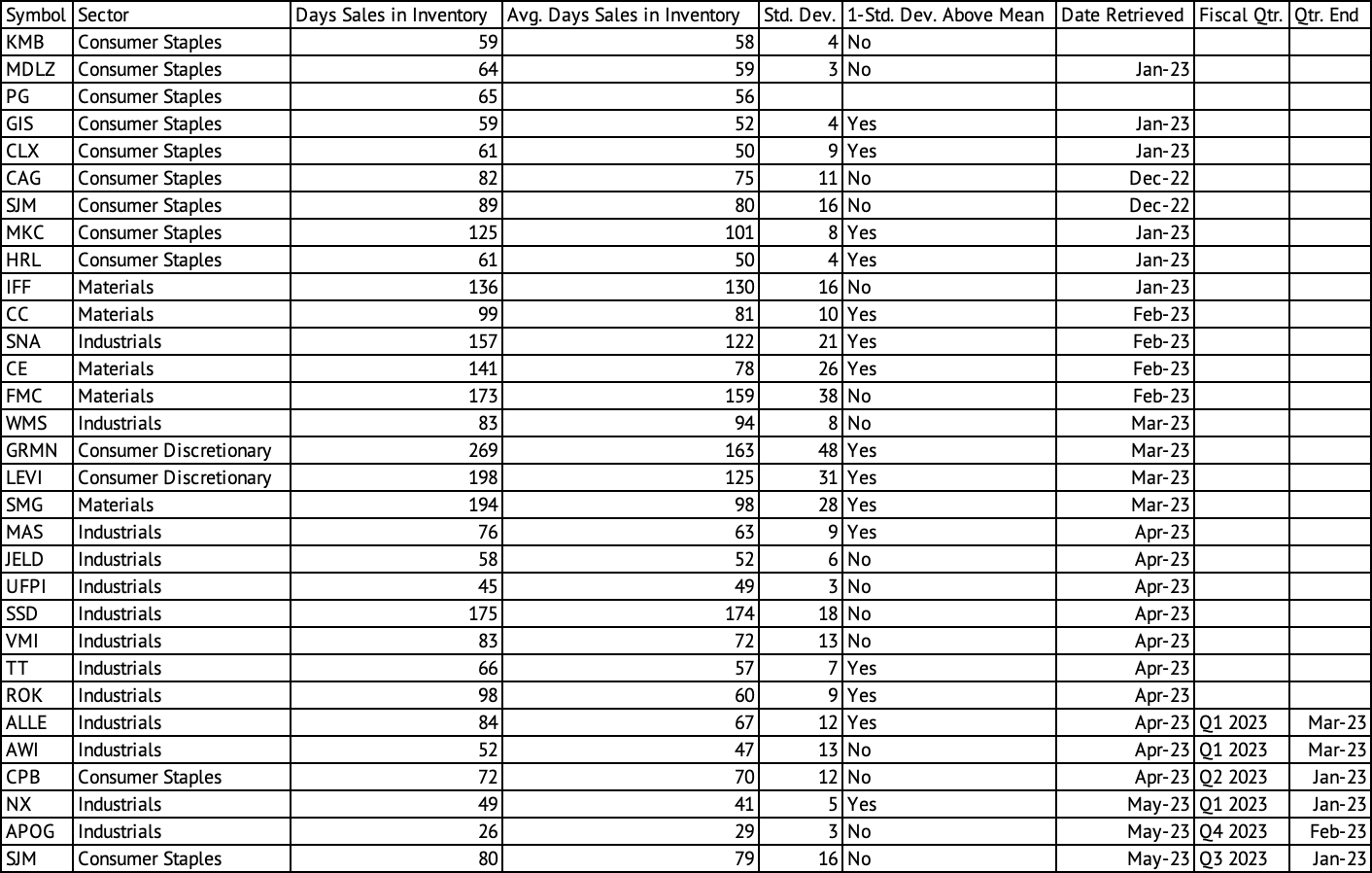

Excessive stock prices improve working capital necessities whereas lowering working money flows. Many corporations have discovered it difficult to handle their stock prices within the face of inflation and return to normalcy in demand because the economic system opened up after the pandemic-induced closure (Exhibit 5). However, J. M. Smucker Firm has managed its stock prices fantastically in comparison with the others within the trade. Basic Mills (GIS), Clorox (CLX), McCormick (MKC), and Hormel (HRL) carried one customary deviation above the imply stock final 12 months.

Exhibit 5:

Day’s Gross sales in Stock for Firms within the Client Staples and Industrials Sector (Searching for Alpha, Creator Compilation)

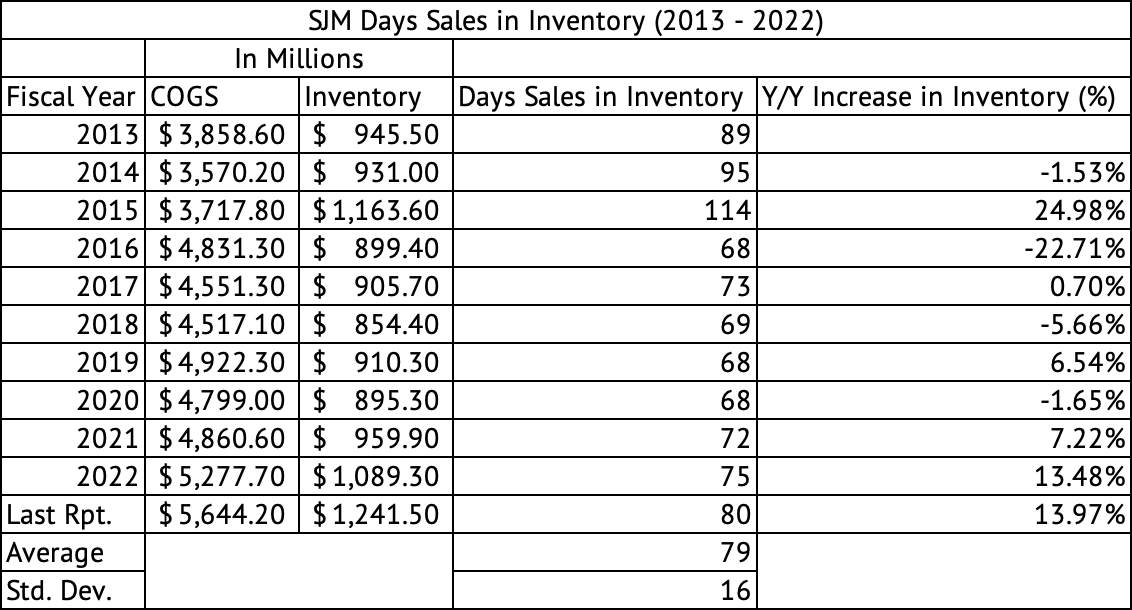

The J. M. Smucker Firm carried 80 days of gross sales in stock in comparison with its common over the previous decade of 79, with a regular deviation of 16 (Exhibit 6). The fiscal 12 months 2015 was an outlier in stock; if that 12 months is eliminated, the corporate averaged 75 days, and the usual deviation could be a lot decrease at 10. On the finish of the corporate’s October 2022 quarter (Q2 2023 fiscal quarter), it carried $1,358.4 million in stock, which can be its peak. At the moment, this stock amounted to 89 days of gross sales.

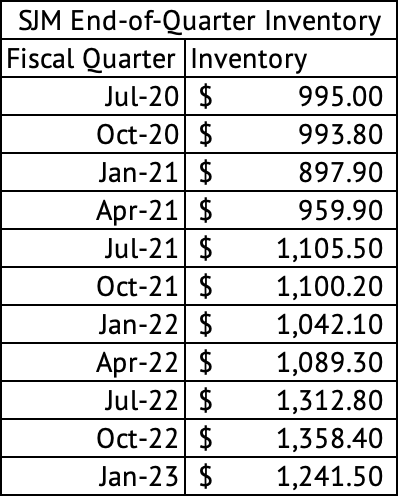

On the finish of the January 2023 quarter (Q3 2023 fiscal quarter), the corporate’s stock was decreased to $1,241.5 million. Based mostly on the corporate’s quarterly stock information, it sometimes carries near $1 billion (Exhibit 7); the corporate might scale back its stock carrying prices by one other $150 million to $200 million. This stock discount may result in one other enhance to working money movement. The stock discount and decrease CapEx within the subsequent fiscal 12 months may enhance money flows.

Exhibit 6:

The J.M. Smucker Firm Day’s Gross sales in Stock (Searching for Alpha, Creator Calculations)

Exhibit 7:

The J.M. Smucker Firm Quarterly Stock (Searching for Alpha, Creator Compilation)

Mildly overvalued

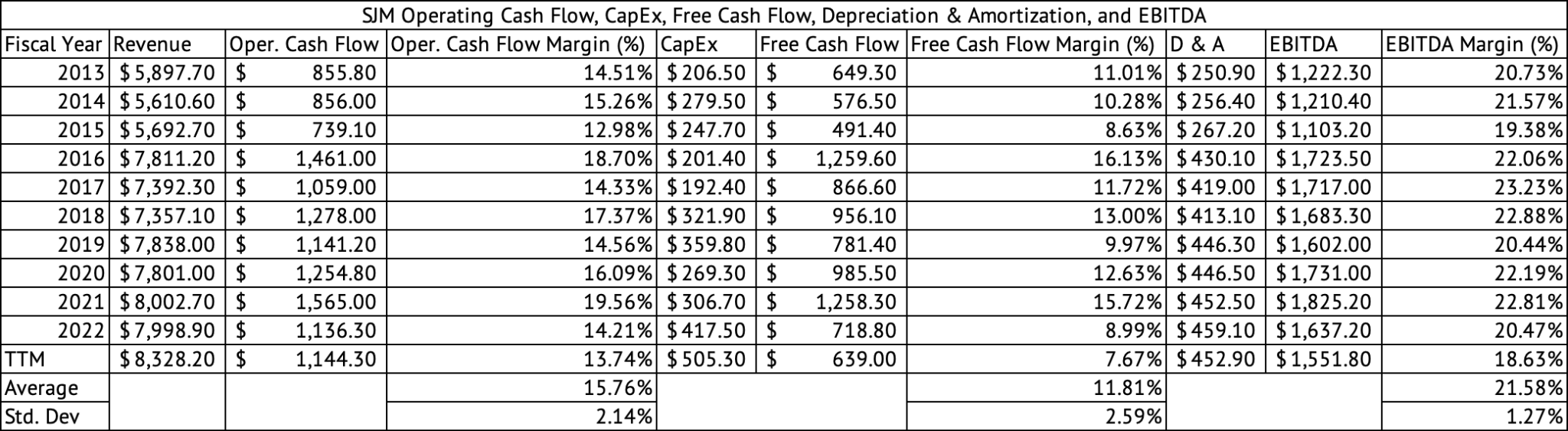

In 2019, the pre-pandemic 12 months, the corporate achieved a 20% EBITDA margin (Exhibit 8). If it reached an analogous margin in fiscal 2024, the corporate would generate over $1.6 billion in EBITDA. Based mostly on that EBITDA, the corporate could be valued at 12.8x EV to EBITDA a number of. The inventory traded at a 5-year common EV to EBITDA a number of of 11.2x.

Exhibit 8:

The J.M. Smucker Firm Working Money Circulate (Searching for Alpha, Creator Calculations.)

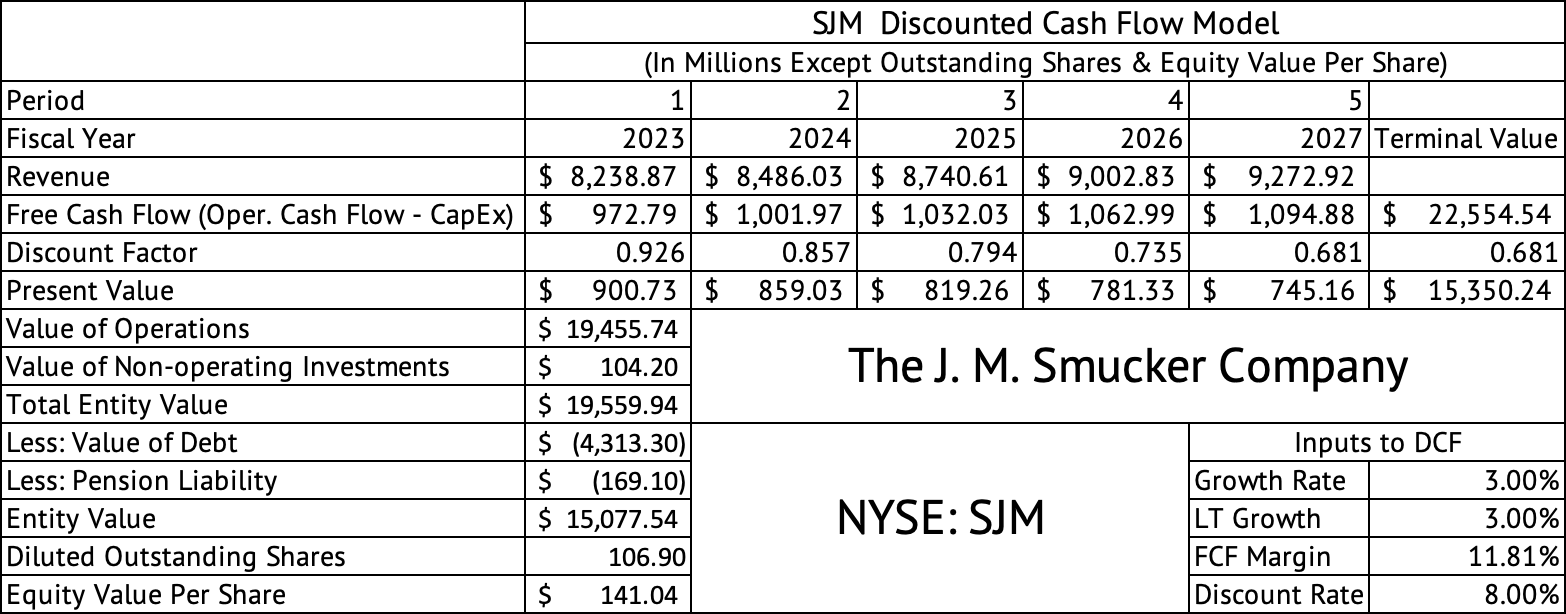

The corporate is just mildly overvalued in comparison with its historic common. A reduced money movement mannequin estimates a per-share fairness worth of the inventory at $141 (Exhibit 9). This mannequin assumes a income development fee of three%, a free money movement margin of 11.8%, and a reduction fee of 8%. The value estimated by this mannequin is near the truthful worth estimate of $135. The 8% low cost fee could also be too liberal. A extra acceptable fee is possibly 9%, nearer to its value of capital. When a 9% low cost fee is used, the per-share fairness worth drops to $110. I believe traders can think about shopping for the inventory when it dips beneath $135. Its 52-week low is 119.82.

Exhibit 9:

The J.M. Smucker Firm Discounted Money Circulate Mannequin (Searching for Alpha, Creator Calculations)

Cautious investor sentiment is behind the power within the client staples sector

This headline from Searching for Alpha captures the rationale behind the power within the client staples sector (Exhibit 10). Buyers wish to park their wealth in an trade much less affected by the market’s volatility; Client Staples shares match that invoice. These shares have a low beta of lower than 1, which means they’re much less dangerous, and their costs change lower than the market. For instance, J.M. Smucker Firm has a beta of 0.21, which means that for each 1% change available in the market, the corporate’s inventory is predicted to alter by 0.21% on common.

Exhibit 10:

Buyers Search the Security of the Client Staples Sector (Searching for Alpha)

Unlike this article on Searching for Alpha that claimed the rally in Client Staples might not be over, the rally is over, and the sector provides little upside on account of its excessive valuation in my opinion (Exhibit 11). The article highlighted the Client Staples Choose Sector SPDR Fund ETF (XLP). That ETF has gone sideways because the analyst’s name. After the analyst’s name on January 7, 2023, the ETF was at $74.94; on Might 19, 2023, the ETF closed at $75.92, a acquire of 1.3% over 5 months. Buyers may even see these shares soar by just a few proportion factors when volatility will increase however might quickly hand over their good points when it subsides. The excessive valuation of the shares within the Client Staples sector is the first purpose the returns could also be capped. The Client Staples Choose Sector SPDR Fund ETF trades at a weighted common PE of 20.6x and a price-to-book ratio of 5.5x. The weighted common PE ratio of shares within the Vanguard Client Staples ETF is 25.4x, with a price-to-book ratio of 4.8x.

Exhibit 11:

The Rally within the Client Staples Sector is Not Over. (Searching for Alpha)

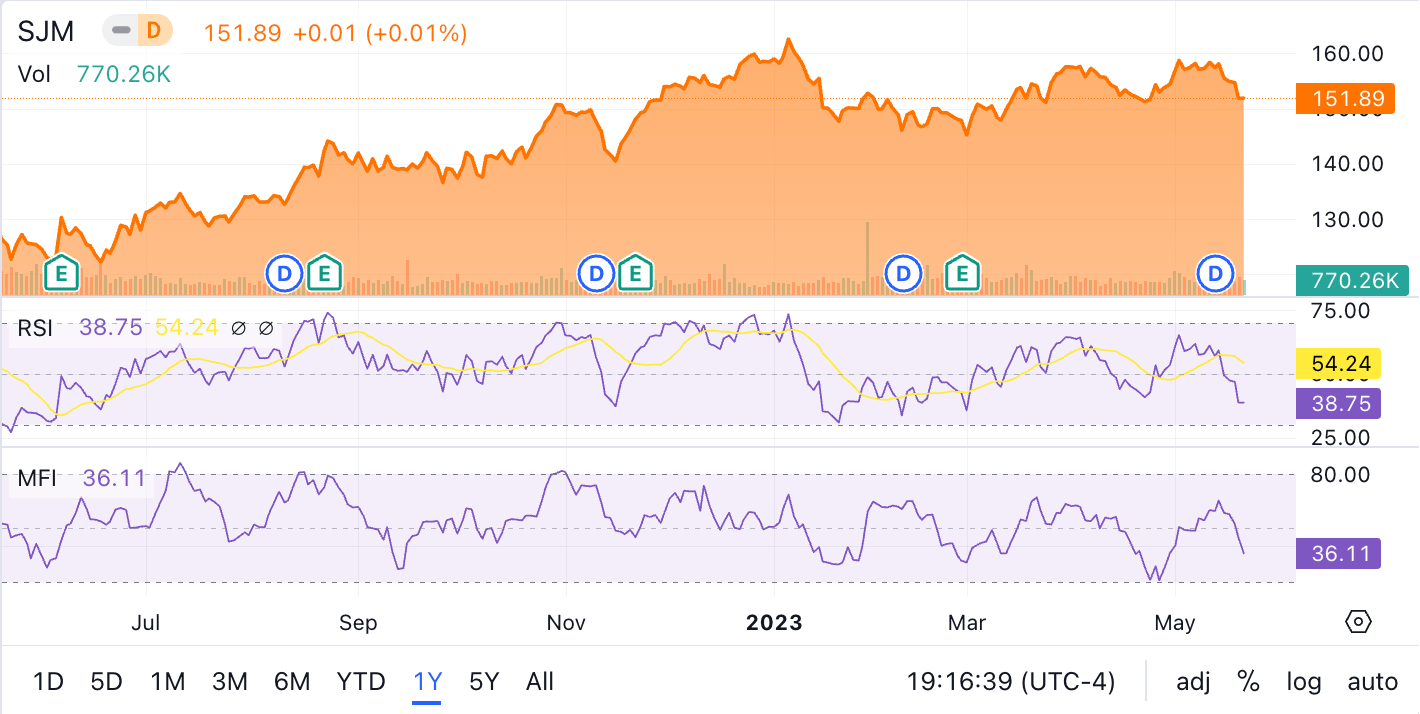

J. M. Smucker has misplaced momentum over the previous three months, having returned 1.3%. The inventory has achieved exceedingly properly, returning 23.5% in comparison with the S&P 500 whole return of 9.3% (Exhibit 12). The inventory has underperformed the S&P 500 Index on a 3-year, 5-year, and 10-year foundation. The RSI and MFI technical indicators present a weakening momentum within the inventory, with each within the mid-thirties trending in the direction of oversold ranges (Exhibit 13).

Exhibit 12:

The J.M Smucker Firm’s Inventory Efficiency (Searching for Alpha)

Exhibit 13:

The J.M. Smucker Firm Technical Indicators (Searching for Alpha)

The J.M. Smucker Firm is dwelling to many iconic manufacturers that will probably be favored for generations. The inventory is buying and selling at a slight premium to its five-year common as traders have piled into client staples shares searching for safety in opposition to the market’s volatility. Buyers might think about shopping for the inventory if the inventory falls 10% or extra within the coming months.

{kind=link}