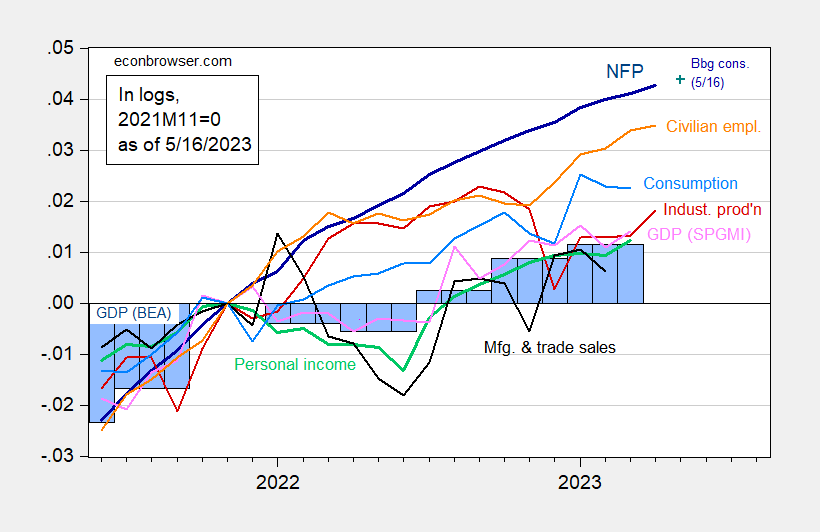

With the economic manufacturing launch exhibiting an upside shock (0.5% m/m vs -0.1 consensus) as a consequence of an outsized manufacturing enhance (1% vs. 0.1% consensus), that is the image of the collection the NBER Enterprise Cycle Relationship Committee (BCDC), plus month-to-month GDP from S&P International Market Intelligence (SPGMI) previously Macroeconomic Advisers.

Determine 1: Nonfarm payroll employment, NFP (darkish blue), Bloomberg consensus of 5/16 (blue +), civilian employment (orange), industrial manufacturing (pink), private earnings excluding transfers in Ch.2012$ (inexperienced), manufacturing and commerce gross sales in Ch.2012$ (black), consumption in Ch.2012$ (gentle blue), and month-to-month GDP in Ch.2012$ (pink), GDP (blue bars), all log normalized to 2021M11=0. Bloomberg consensus stage calculated by including forecasted change to earlier unrevised stage of employment out there at time of forecast. Supply: BLS, Federal Reserve, BEA 2023Q1 advance launch by way of FRED, S&P Global/IHS Markit (nee Macroeconomic Advisers, IHS Markit) (5/1/2023 launch), and writer’s calculations.

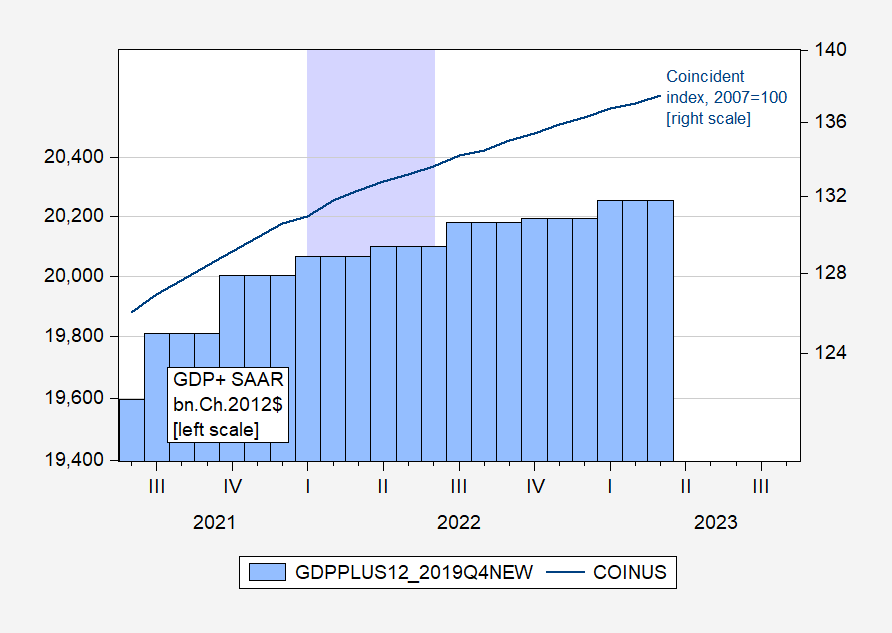

It’s fascinating to contemplate the evolution of two different indicators of the broad state of the economic system: GDP+ and the Philadelphia Fed’s coincident index for the US.

Determine 2: GDP+, scaled to 2019Q4, in bn.Ch.2012$ SAAR (blue bars, left log scale), and coincident index (blue, proper log scale). Lilac shading denotes a putative 2022H1 recession. Supply: Philadelphia Fed and Philadelphia Fed.

Apparently, GDP+ and the coincident index (the latter primarily based totally on labor market indicators) didn’t point out a recession in 2022H1.

With the economic manufacturing launch exhibiting an upside shock (0.5% m/m vs -0.1 consensus) as a consequence of an outsized manufacturing enhance (1% vs. 0.1% consensus), that is the image of the collection the NBER Enterprise Cycle Relationship Committee (BCDC), plus month-to-month GDP from S&P International Market Intelligence (SPGMI) previously Macroeconomic Advisers.

Determine 1: Nonfarm payroll employment, NFP (darkish blue), Bloomberg consensus of 5/16 (blue +), civilian employment (orange), industrial manufacturing (pink), private earnings excluding transfers in Ch.2012$ (inexperienced), manufacturing and commerce gross sales in Ch.2012$ (black), consumption in Ch.2012$ (gentle blue), and month-to-month GDP in Ch.2012$ (pink), GDP (blue bars), all log normalized to 2021M11=0. Bloomberg consensus stage calculated by including forecasted change to earlier unrevised stage of employment out there at time of forecast. Supply: BLS, Federal Reserve, BEA 2023Q1 advance launch by way of FRED, S&P Global/IHS Markit (nee Macroeconomic Advisers, IHS Markit) (5/1/2023 launch), and writer’s calculations.

It’s fascinating to contemplate the evolution of two different indicators of the broad state of the economic system: GDP+ and the Philadelphia Fed’s coincident index for the US.

Determine 2: GDP+, scaled to 2019Q4, in bn.Ch.2012$ SAAR (blue bars, left log scale), and coincident index (blue, proper log scale). Lilac shading denotes a putative 2022H1 recession. Supply: Philadelphia Fed and Philadelphia Fed.

Apparently, GDP+ and the coincident index (the latter primarily based totally on labor market indicators) didn’t point out a recession in 2022H1.

{kind=link}