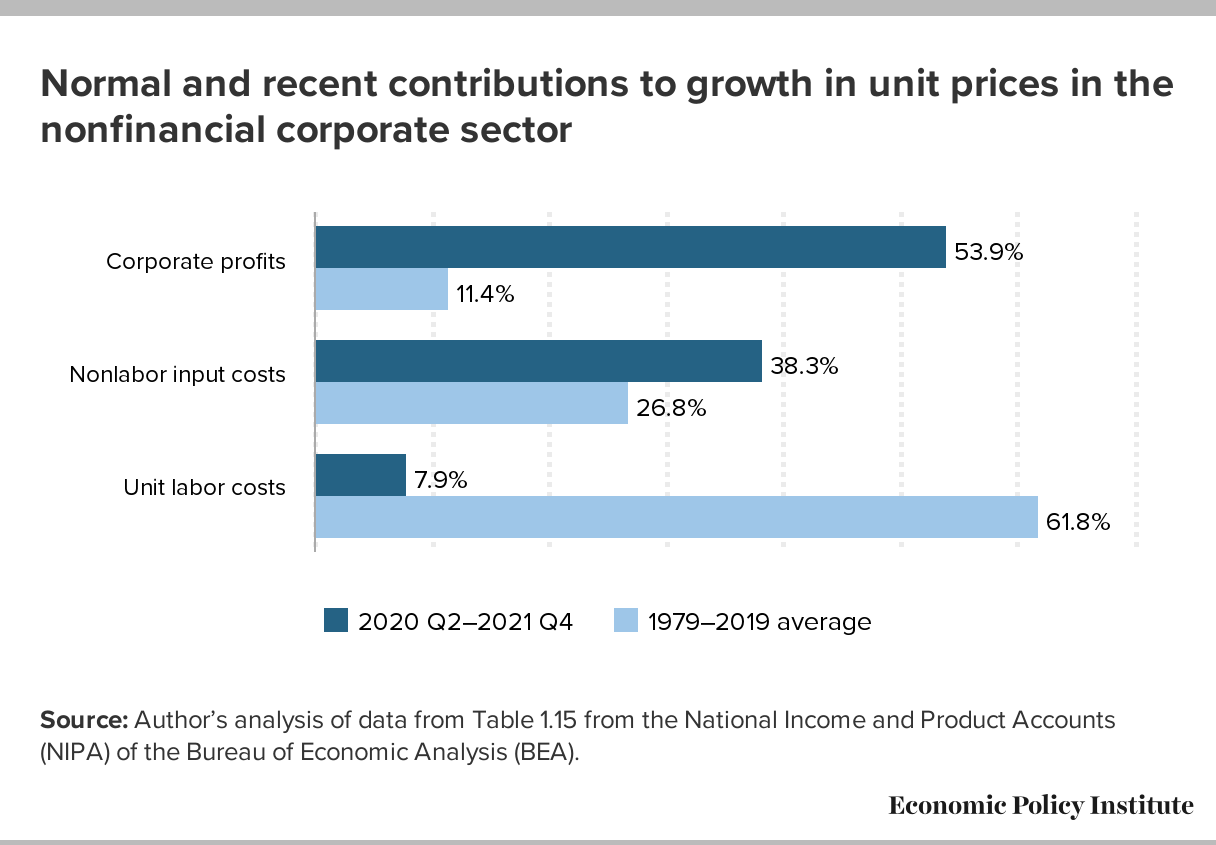

Josh Bivens at EPI has not too long ago offered a decomposition of value modifications into these attributable to price-cost margins (i.e., roughly income), labor and nonlabor enter costs, to wit:

Supply: EPI, April 2023.

Former Fed Governor Brainard in addition to Paul Krugman have commented on this price-price spiral (though I feel the latter is rather less definitive on whether or not he believes this constitutes the vast majority of the inflationary impulse).

Whereas the decomposition is attention-grabbing (it’s a decomposition in spite of everything), I’m undecided that the argument that Bivens forwards that it’s not demand pressures (aka overheating). Whereas in very early NK fashions, the elasticity of demand for the differentiated items are fixed over the enterprise cycle, so the value price margin is fixed, more moderen work (e.g., Nakardo and Ramey, JMCB 2020) notes that relying on the kind of shock, the revenue margin might be procyclical.

It is perhaps helpful to consider value modifications within the presence of stickiness. When inflation is fast, then deviations from the optimum value at any given time between price-resetes will likely be bigger, inducing bigger revenue loss. Assuming extra fast anticipated inflation within the present episode than occurred in earlier durations then implies corporations re-set costs quicker, and by bigger increments. From this angle, I would count on a much bigger mechanically-defined contribution from income, particularly if corporations over-estimate inflation.

The previous argument depends on a Calvo pricing view. If value modifications are staggered, an alternate interpretation is that the strategic complementary that slows value adjusment in periods of low inflation can be attenuated when corporations attain consensus on a quicker charge of inflation.

These aren’t rigorous (i.e., basic equilibrium) arguments for an elevated revenue margin; they’re simply methods of claiming we’re undecided the elevated revenue margins aren’t as a consequence of larger mixture demand.

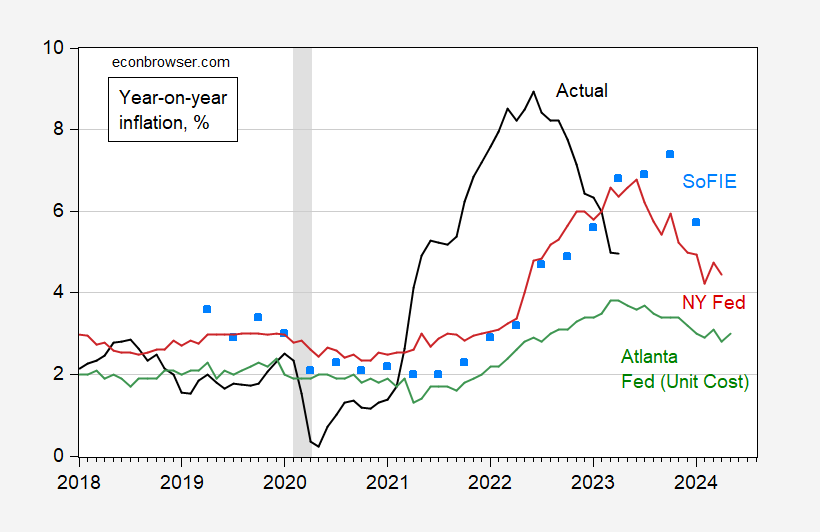

How briskly did agency CEOs count on inflation to be? Coibion and Gorodnichenko present the reply of their Survey of Agency Inflation Expectations.

Determine 2: Precise CPI inflation, y/y (black), NY Fed shopper inflation expectations for yr forward (pink), Atlanta Fed unit price inflation for yr forward (inexperienced), and agency expectations for inflation a yr forward (sky blue squares), all in %. NBER outlined peak-to-trough recession dates shaded grey. Supply: BLS, NY Fed, Atlanta Fed, Coibion-Gorodnichenko, NBER and creator’s calculations.

The final statement we’ve for agency expectations is the January 2023 forecast for January 2024 year-on-year inflation. Curiously, within the November and January surveys, agency anticipated inflation outstripped shopper expectations (which in flip outstripped economists’). In different phrases, corporations anticipated fast inflation (though not as fast as precise outcomes, till April’s quantity). Word the Atlanta Fed measure of anticipated unit price inflation will not be from the identical pattern as that for the agency inflation, so a direct comparability will not be potential.

Not one of the foregoing is to say that the income at the moment loved by corporations is “good”. Quite, I’d simply say it’s not clear that one can infer from revenue margins whether or not demand shocks drove the result or not.

{kind=link}