lcva2

Pricey readers/subscribers,

It has been round 1.5-2 months since I final wrote about Teleperformance (OTCPK:TLPFY). You may marvel why I, after such brief a time, am all of the sudden writing extra articles on the corporate. The reply to that’s comparatively easy – the thesis has grown stronger, and the present upside undoubtedly warrants your consideration.

As a result of seen from a conservative perspective, the upside for Teleperformance at this specific time is likely one of the highest conservative upsides with over 2% yield I see in the complete market, with the corporate’s credit score scores included within the consideration.

Let us take a look at what now we have going for us right here.

Teleperformance – The upside is even increased at this level

So, one of many largest firms in name facilities and associated applied sciences is at the moment undoubtedly on sale. The corporate is likely one of the highest-quality companies on this whole section based mostly on profitability and returns. It really works within the “Enterprise Companies” section, a extremely aggressive section, and being that it is in one thing like Name facilities, this isn’t precisely a high-margin trade, to start with.

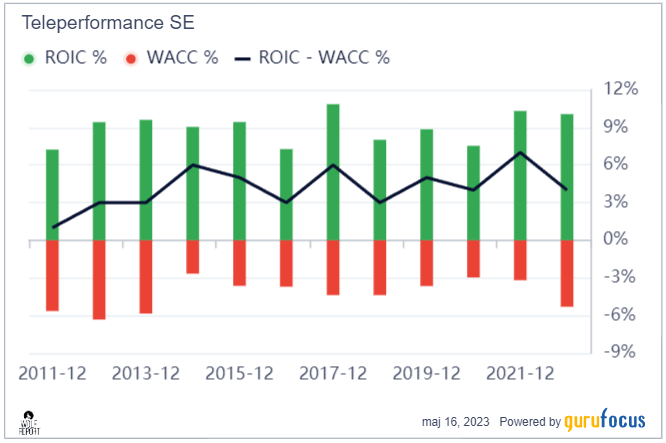

7-9% internet margin is what you’ll be able to count on from this section, double-digits and also you’re an outperformer. Teleperformance is round 8%, with working margins of round 12%, and gross margins of about 32.7%. The corporate is a well-oiled machine, not solely in turning top-line gross sales into internet earnings but additionally when it comes to profitability and ensuring that its investments generate good returns. Over the previous decade, the corporate has at all times had persistently worthwhile ROIC internet of WACC, and the corporate’s high and backside line metrics have been rising.

Teleperformance ROIC/WACC (GuruFocus)

Whereas debt has been rising, the corporate has been successfully managing its total M&A and increasing its enterprise. It now has a really interesting break up as of 2022A, with 32.9% NA; 32.6% EMEA, 20.3% LATAM, and 14.3% Specialised providers.

In a comparatively brief period of time, Teleperformance dropped a good bit, over 20%. That is additionally why after I enter new positions, I usually dimension up slowly – issues may drop, and I like averaging out. It implies that regardless of this drop, since having a median up, I am about at detrimental 6% ROR for my place, which is not worrying to me, since I consider the corporate to be qualitative.

Why the drop, although?

It began with an introduced M&A of Majorel, which precipitated the share value to drop a corresponding quantity in relation to the announcement. We additionally had some indicators of the 1Q23 outcomes. Majorel first, in accordance with the data beneath.

Paris, April 26, 2023 – Teleperformance, a world chief in digital enterprise providers, in the present day introduced its proposed voluntary money and share provide for all shares in Majorel (the “Shares”). Teleperformance provides €30 per share for a complete consideration of €3bn. The Majorel shareholders also can elect to obtain Teleperformance shares at an alternate ratio of 0,1382 Teleperformance share for every Majorel share, as much as a most of €1bn in Teleperformance shares.

Subsequently, the preliminary drop of about €30/share was in no way unusual. As well as, the 1Q23 outcomes we do have, income particularly, noticed a rise of 8.6% YoY excluding COVID-19 contracts, 1.9% on an LFL foundation, and a pair of.2% on an as-reported foundation. This got here from strong natural development from the corporate’s diversified foundation, together with actions in social media, finservices, journey, and with authorities companies.

Teleperformance IR

The corporate additionally managed sustained development in its NA-based offshoring actions, delivering sustained margin enhancements. China reopening was one other constructive for the corporate, and the impacts from the varied COVID-19 contracts ending are getting decrease and decrease as a few of these begin winding down. For 1Q, the present influence was now lower than €150M for the quarter.

Based mostly on the corporate’s sturdy 1Q23, Teleperformance revised its total targets. These targets now embody:

- LFL Rev development, excluding COVID-19, of 8-10% on an annual foundation, and together with COVID-19, round 7%, illustrating the later-year wind down of those contracts.

- EBITDA margin enhancements to file ranges of round 16% or above, which is a 30 bps+ enchancment on a earlier degree.

- The corporate needs to additional goal extra M&As able to producing additional worth as issues transfer ahead.

So, all in all, I see that first interval as just about a affirmation of what I already knew to be a constructive outlook for this wonderful firm. The atmosphere is unsure, and there are some elements that might ship this the incorrect means, that is for positive. Volatility is on this firm’s blood – the 48% detrimental 1-year RoR is proof sufficient of that.

Nonetheless, the corporate has additionally dropped that a lot with out actually any underlying motive so far as earnings, forecasts, or precise tendencies go. The corporate is a succesful market chief, and far of the upside or dominance is not actually up for debate – specifically so far as satisfaction on the shopper/agent aspect.

Teleperformance IR

The corporate’s purchasers are, as you may count on, throughout a number of industries. Some main sectors embody Airways, Hospitality, OTA, Cruise, and Automotive rental industries. Whereas it is correct to explain TP primarily as a “core” providers enterprise, akin to name facilities, based mostly on an 85.7% income portion from this section for 2022, the corporate additionally generates over €1.2B in revenues from specialised providers – and this combine on an total degree is likely one of the attracting elements to this firm that I can see.

As I discussed in my premiere piece on Teleperformance – you should not contact this enterprise until you are in it for the lengthy haul. By this, I imply that the corporate could not materialize its upside for 2-5 years – however when it does, I consider that it’ll accomplish that with a vengeance, bringing with it returns of potential within the 150-300% RoR vary.

The yield is not nice, however at 2%+ it isn’t horrible both. I do know loads of firms which can be usually described as acceptable dividend shares which have beneath 3% in total yield. Provided that it is a once-a-year payout although, I would not count on important dividends on a continuous foundation right here – it is extra alongside the road of a once-a-year paying bond.

The true upside is within the capital appreciation potential – not in seeing Teleperformance as an earnings funding.

Teleperformance – The upside might be large, and try to be paying consideration

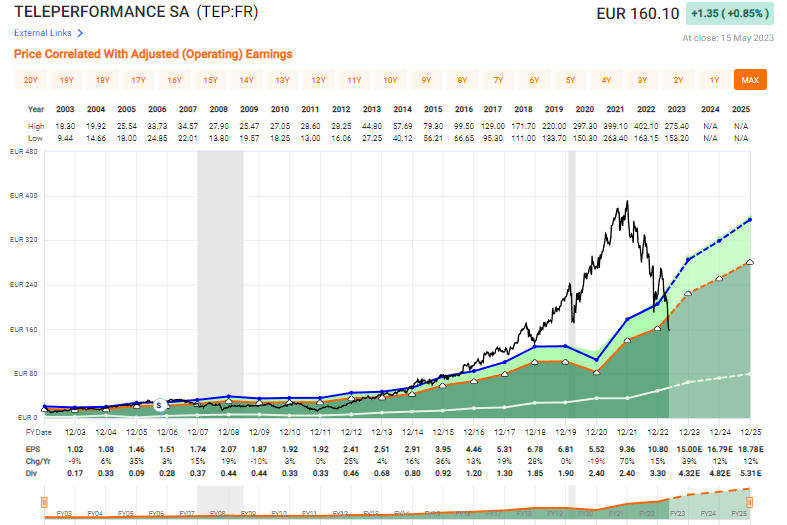

The truth that Teleperformance is an organization that is gone excessive, solely to drop again down “too far” needs to be evident by taking a look at a single graph.

Teleperformance Valuation (F.A.S.T. Graphs)

This can be a visible illustration of what might be seen by taking a look at historic P/E ranges as effectively. What’s occurred over the previous few years, particularly after COVID-19, is that the corporate’s place within the on-line infrastructure has been overestimated, and inflated. Folks have been anticipating this firm to by no means flip down once more.

All the things turns down – even this firm. And that is what we’re seeing right here. That is why the corporate when it comes to valuations, hasn’t been this low cost for nearly a decade. And that, expensive readers, is why I’m beginning to “pound the desk” for Teleperformance as an funding.

The comparatively easy reality is that even estimating Teleperformance at a development price with a 15x P/E, the forecasted numbers give us an upside potential of near 25% per yr, or 75%+ till 2025E. And that’s by forecasting an organization that’s anticipated to develop EPS by an annual price of 18% at a 15x P/E.

You may try this, and you can nonetheless beat the market. However the true magic occurs if you begin estimating the corporate at multiples that might truly be truthful in relation to the place the corporate is predicted to develop. At that time, we begin getting some very completely different numbers.

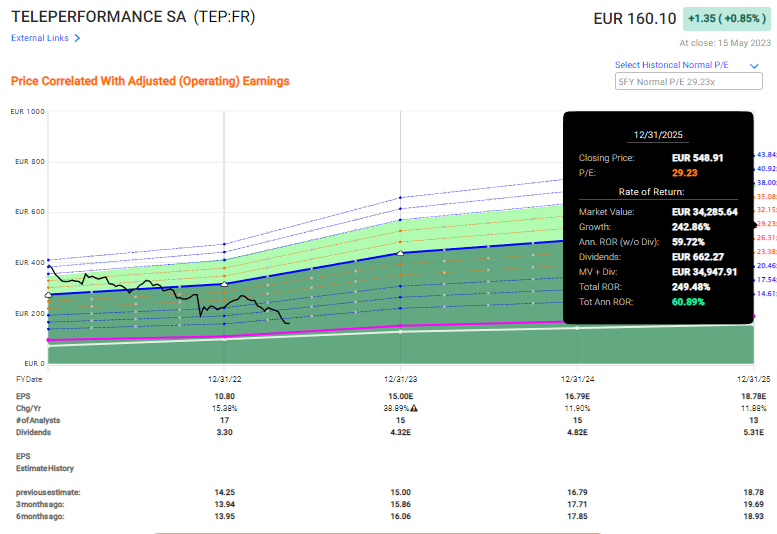

Teleperformance Upside (F.A.S.T. Graphs)

That expensive readers, is full normalization potential. That is 250% in lower than 3 years, and whereas it might be exuberant to count on that type of degree, please word that on a historic foundation, it is not exterior the realm of chance for this enterprise. The truth is, it is completely potential that that is what we may even see. The distinction between the 2 situations is very large – double in P/E within the latter one, clearly. My level is that even when you have been to forecast Teleperformance at 10x P/E, you are still strolling away with doubtlessly market-beating 8.5% returns on a present forecast foundation.

And there usually are not many firms on the market that supply this to you.

The corporate additionally has a confirmed monitor file of worth creation over time and is likely one of the most well-diversified communications firms I’ve ever encountered. Based mostly on this, you should not view enhancements or beating this forecast as unlikely both. Analysts do not miss on this firm both – not usually. A 2-year ahead foundation with a 20% MoE sees analysts hitting the mark of 91% when you embody beats by the corporate. That is a superb statistic, and one I consider we will truly “financial institution” on.

As I discussed in my final article – there are friends, however none are near as attention-grabbing as Teleperformance. These friends embody companies akin to Telus (TU), Concentrix (CNXC), Atento (ATTO), Sykes, TTEC (TTEC), and Webhelp – none come near matching Teleperformance as an funding right now.

The corporate stays considerably undervalued on the idea of different buyers as effectively. Present common S&P World targets give us a median of €307, based mostly on a low of €146 and a excessive of €380/share, giving us an upside of 91.9% with 13 out of 16 analysts at both a “BUY” or an equal outperform ranking.

Conclusively, the upside is now even increased – 250% – and I do not see any elementary or forecast-related motive why the corporate can be underperforming.

Based mostly on this, I give this a continued “BUY”, with an enormous upside.

Thesis

- Teleperformance is an outstanding firm within the name middle and basic enterprise service outsourcing subject. I think about the corporate to be one of many best round, and attributable to a mix of elementary power and wonderful upside, to be a “purchase” right here.

- The “purchase” is said based mostly on a conservative goal share value of €275/share – and by giving it that concentrate on, I am 10-20% decrease than the typical analyst, attributable to my at all times discounting conservatively. Nonetheless, I consider this firm has the very actual potential to outperform.

- For that motive, I lately purchased shares, and I am about to purchase extra.

Keep in mind, I am all about:

- Shopping for undervalued – even when that undervaluation is slight and never mind-numbingly large – firms at a reduction, permitting them to normalize over time and harvesting capital features and dividends within the meantime.

- If the corporate goes effectively past normalization and goes into overvaluation, I harvest features and rotate my place into different undervalued shares, repeating #1.

- If the corporate does not go into overvaluation however hovers inside a good worth, or goes again all the way down to undervaluation, I purchase extra as time permits.

- I reinvest proceeds from dividends, financial savings from work, or different money inflows as laid out in #1.

Listed below are my standards and the way the corporate fulfills them (italicized).

- This firm is total qualitative.

- This firm is basically protected/conservative & well-run.

- This firm pays a well-covered dividend.

- This firm is at the moment low cost.

- This firm has a sensible upside that’s excessive sufficient, based mostly on earnings development or a number of enlargement/reversion.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a serious U.S. alternate. Please concentrate on the dangers related to these shares.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a serious U.S. alternate. Please concentrate on the dangers related to these shares.

{kind=link}