claudiodivizia

By James Smith

The Financial institution of England has raised charges as broadly anticipated to 4.5% – and has saved its choices broad open for future conferences.

There aren’t any huge bombshells right here – the choice to hike charges was backed by seven committee members, because it was on the earlier two conferences. Plenty of the post-meeting headlines will concentrate on the massive upgrades to progress, however in the end this was flagged by the BoE in its earlier set of assembly minutes and as a lot as anything, it displays decrease pure fuel costs over latest months. Importantly, the Financial institution has retained its intentionally obscure ahead steerage that additional hikes may come if inflation exhibits higher indicators of “persistence”.

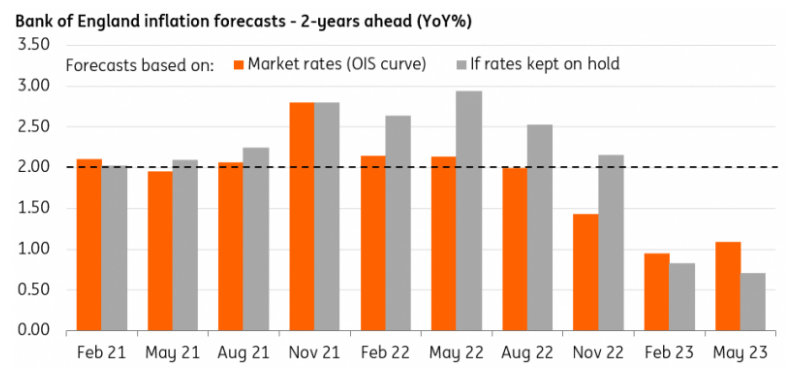

Scratch beneath the floor although, and there are hints that this tightening cycle is reaching its limits. Policymakers typically level to the inflation forecast for two-years’ time, the time horizon over which rates of interest have their largest affect. And as we noticed within the final set of forecasts from February, the committee sees inflation nicely beneath goal at round 1% in mid-2025 – and crucially, that’s no matter whether or not rates of interest comply with the trail anticipated by monetary markets, or if charges keep mounted at 4.5%.

Admittedly a few of this can be accounted for by power – and the committee has made some extent of claiming the dangers are skewed to the upside. However the easy truth is that the Financial institution’s personal forecast exhibits little must take charges larger. Because the chart beneath exhibits, it is uncommon that the two-year-ahead forecast is to date beneath goal.

The BoE is forecasting inflation nicely beneath goal in 2 years’ time

Financial institution of England

What subsequent? We proceed to really feel that this may most certainly mark the highest on this tightening cycle, although we settle for that is closely contingent on the subsequent set of wage and inflation information. One other hike in June is feasible, although for not the bottom case. The Federal Reserve’s much-discussed pause and broadly anticipated charge cuts later this yr does present the BoE with some respiration room.

The extra attention-grabbing query is when charges will in the end be lower. Our view is that that is unlikely to be this yr, partly as a result of the roles market is proving resilient. The Financial institution has watered down its forecasted rise of the unemployment charge, and with that lifted its prediction for wage progress. However equally the story on inflation is beginning to look higher.

Sure, inflation has been larger than the BoE predicted in February, however that’s largely due to stickier meals and items costs – neither of that are as related for financial coverage as service-sector inflation, which has been much less unpredictable and seems to be nearing a peak. Survey indicators are suggesting that corporations’ pricing expectations are cooling off, and assuming fuel costs keep low, we predict there are good causes to suppose service-sector inflation will fall materially over the subsequent 12 months or so.

With rates of interest now, by any cheap definition, in restrictive territory, we predict the Financial institution will start the method of taking them again to a extra impartial footing with charge cuts by this time subsequent yr. We’re penciling within the first lower for Could subsequent yr.

Content material Disclaimer

This publication has been ready by ING solely for data functions no matter a selected person’s means, monetary state of affairs or funding goals. The knowledge doesn’t represent funding suggestion, and neither is it funding, authorized or tax recommendation or a suggestion or solicitation to buy or promote any monetary instrument. Read more

Editor’s Word: The abstract bullets for this text had been chosen by In search of Alpha editors.

{kind=link}