kzenon

Introduction

United Leases (NYSE:URI) is among the compounding superstars I’ve adopted and lined for a few years. Not solely has the corporate found out easy methods to successfully penetrate a extremely aggressive development tools market. It additionally has develop into a dividend progress inventory, with the potential to ship each outperforming capital positive factors and excessive dividend progress for a few years to return.

Sadly, resulting from its cyclical habits, its shares are promoting off. That is what I wrote in February (emphasis added):

The corporate is able to robust long-term progress. It has a wholesome steadiness sheet, excessive free money move, and the flexibility to reward buyers with long-term dividend progress on high of buybacks.

Whereas the valuation is honest, I consider that financial headwinds will present us with new shopping for alternatives down the highway.

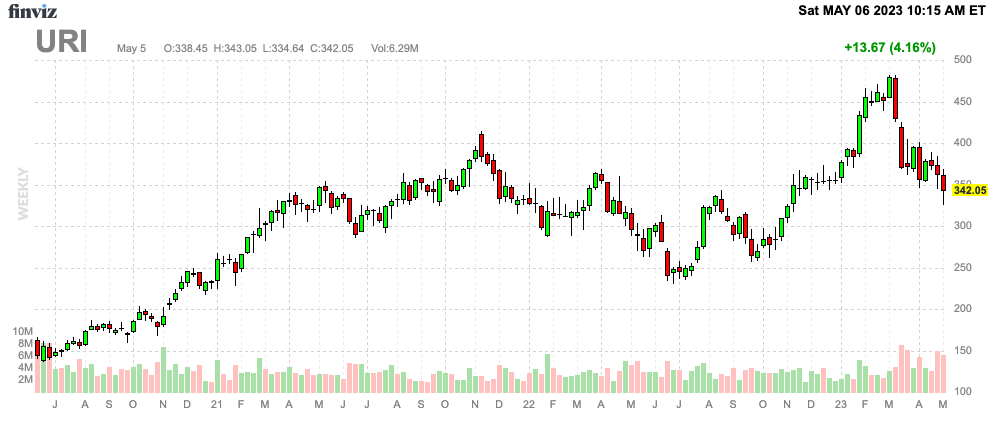

Since my February article, URI shares have misplaced 1 / 4 of their worth, which makes it one of many steepest sell-offs because the 2020 pandemic.

FINVIZ

Based mostly on that context and the just-released earnings, we’ve so much to debate, as discovering an appropriate entry may lead to super long-term worth for URI buyers.

So, let’s get to it!

Rising The URI Manner

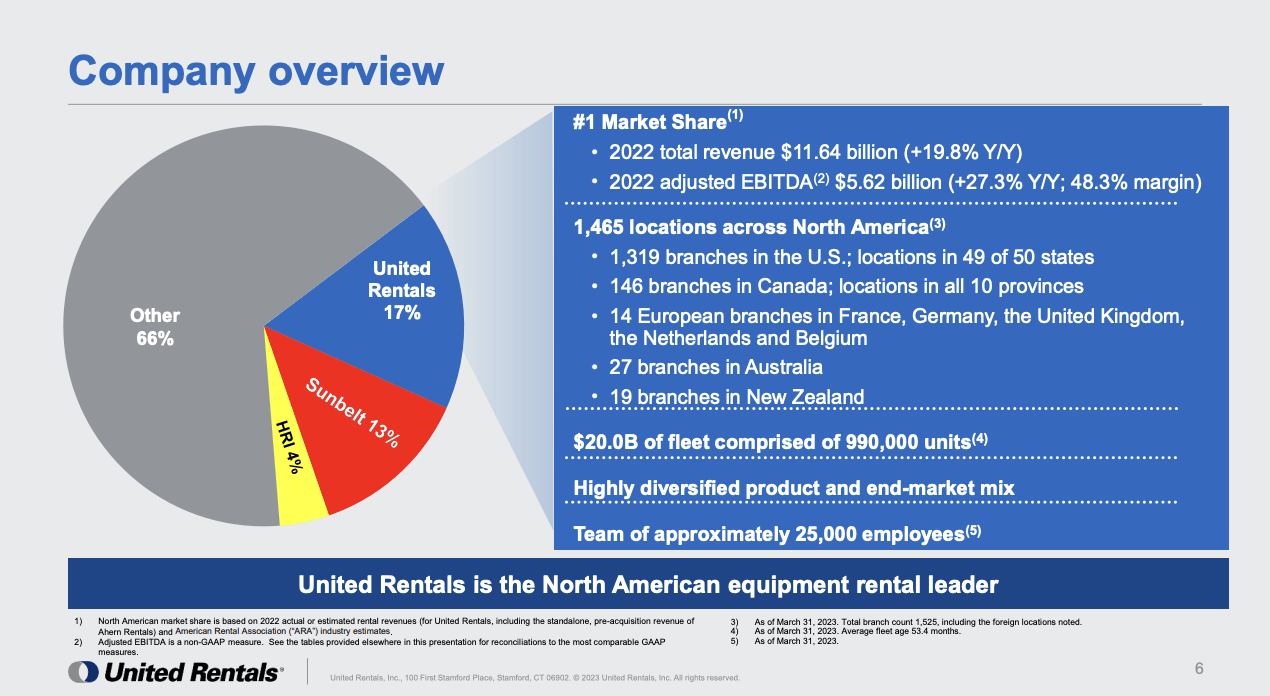

With a market cap of roughly $24 billion, Stamford, Connecticut-based United Leases is the biggest firm within the Rental & Leasing Companies trade. This trade is part of the economic sector.

The corporate was included in 1997 and based by Mr. Brad Jacobs, who additionally based LTL large XPO, Inc. (XPO), which has spun off a lot of main corporations in different transportation industries.

With that mentioned, I am not fascinated by shopping for rental corporations. Entry limitations are low, and development (and associated) tools is extraordinarily cyclical. Throughout financial downturns, there is a large probability you personal an organization with a yard filled with money-losing equipment – if you happen to permit me to color with a broad brush.

Whereas this can be a threat that applies to United Leases, the corporate is totally different. It has exploited the truth that entry limitations are low and created a enterprise mannequin that achieves fast progress via natural progress and acquisitions.

The corporate ended 2022 with a 17% market share, which included virtually 1,500 places in North America, 13 branches in Europe, 27 branches in Australia, and 19 branches in New Zealand.

United Leases

- 48% of its clients are industrial clients, which incorporates energy and utility corporations, manufacturing, oil downstream, metals and mining, oil and fuel, and the whole lot associated to those industries.

- 47% of its clients are non-residential development clients.

- Solely 5% of its clients use tools for multi-family development.

Once I consider URI, I consider the Monopoly recreation. There are different shares the place this is applicable to as effectively. Principally, gamers that get forward early within the recreation are likely to win. I haven’t got scientific knowledge to again it up, however I believe it is a cheap thesis. The second gamers get forward, they will construct homes and lodges, rising the percentages of constructing much more cash. In some unspecified time in the future, it is recreation over as corporations profit from an rising benefit over opponents.

United Leases is analogous. The corporate has constructed a terrific framework over the previous few a long time. It now has a large community of shops supported by relationships and capabilities that permit the corporate to supply companies that smaller gamers can’t compete with.

United Leases

Under are among the advantages that I listed in February:

- Dimension – The corporate is massive sufficient to service massive clients that require substantial portions of apparatus. Smaller corporations can’t compete with that.

- Selection – Its measurement additionally comes with selection, which means it has tools for particular functions. Once more, smaller operators can’t compete with that.

- Buying energy – When URI buys new tools, it has a significantly better place in the case of negotiating higher costs. Once more, it is associated to the “measurement” profit.

- The Nationwide Account Program – This program establishes long-term relationships with massive corporations with a nationwide or multi-regional presence. This combines all the advantages above and ties them to long-standing clients.

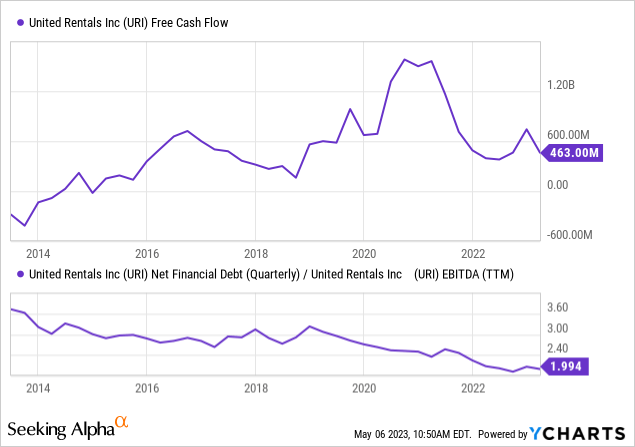

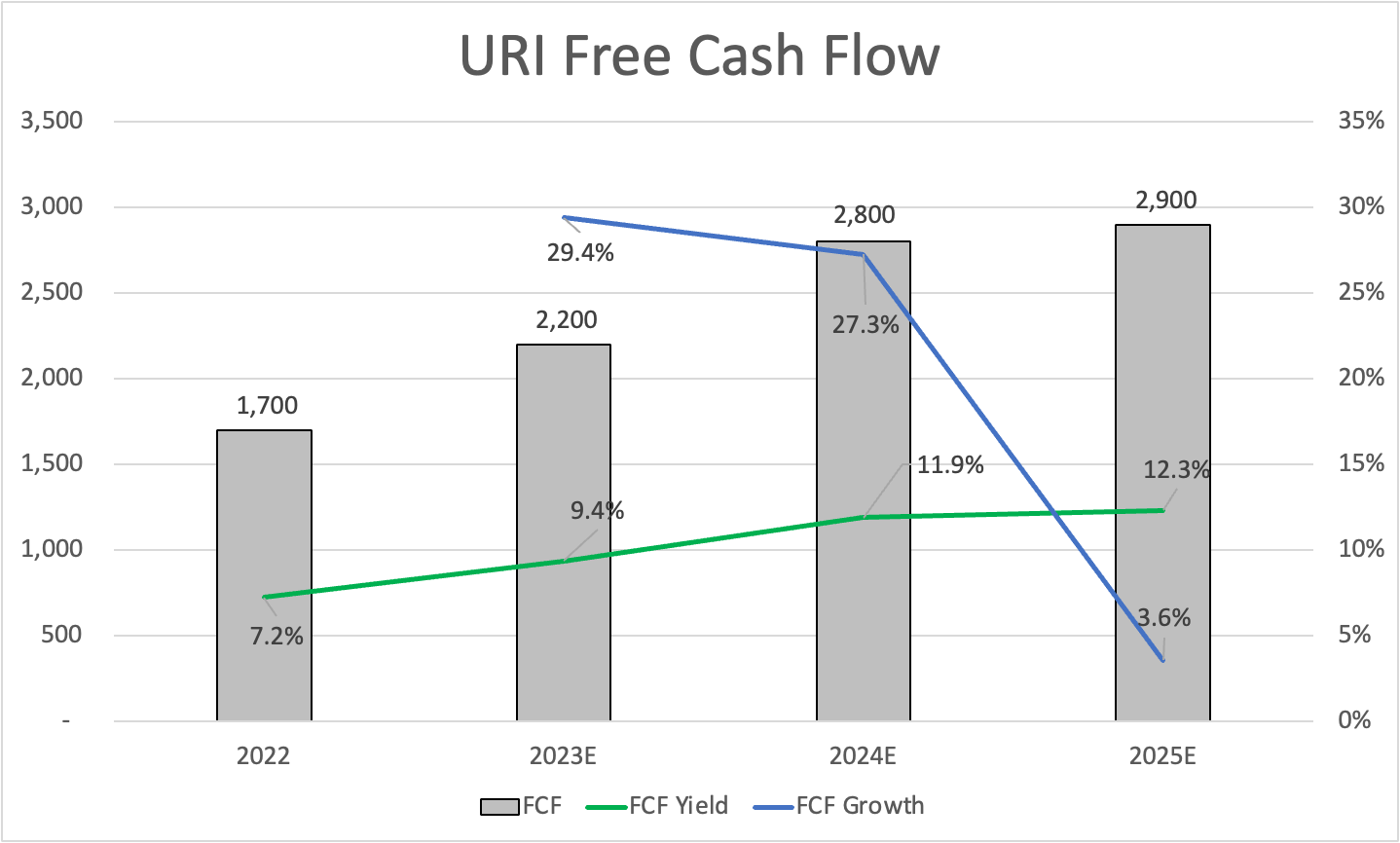

Wanting on the chart beneath, we see that URI has develop into more and more highly effective. Since 2015, the corporate is persistently reporting optimistic free money move, which has resulted in a steep decline within the firm’s internet leverage ratio. The corporate presently enjoys a BBB- credit standing.

Additionally, notice that this monetary efficiency is predicated on aggressive M&A. The corporate has spent billions on acquisitions prior to now decade, shopping for robust gamers to reinforce its personal working efficiency. Not solely that, however the firm has completed this with out inflicting its steadiness sheet to develop into dangerous. The decline in internet debt above speaks for itself.

United Leases

On high of that, URI is now a dividend (progress) inventory.

Dividends, Buybacks & Outperformance

On January 25, URI introduced its first dividend. The corporate initiated a $1.48 per share per quarter dividend, which interprets to a yield of 1.7%.

This dividend is protected by its wholesome steadiness sheet and a load of free money move. Taking a look at estimates, the corporate is just not solely anticipated to keep up excessive free money move however it’s also anticipated to finish up with a double-digit free money move yield after 2023 – primarily based on its present market cap.

Leo Nelissen

Whereas the corporate didn’t say something particular with regard to its dividend in its 1Q23 earnings call final month, it did touch upon its dividend in January.

We plan to purchase again $1 billion of inventory this 12 months. And we’ll even be instituting quarterly dividends for our shareholders, totaling $5.92 per share this 12 months. These two choices underscore our confidence within the sturdiness of our money era and the energy of our steadiness sheet. And collectively, they’ll return $1.4 billion of capital to our shareholders in 2023.

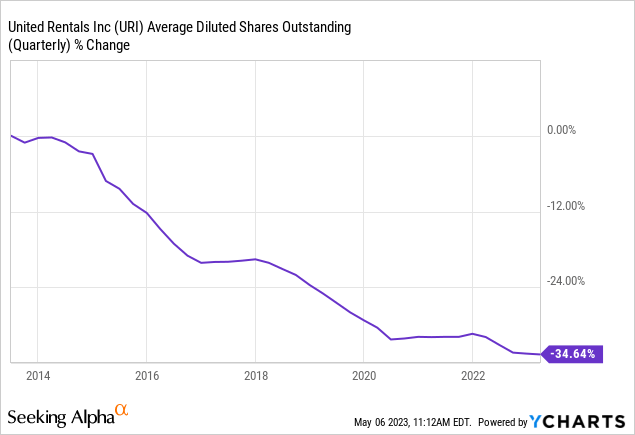

Moreover, URI has purchased again greater than a 3rd of its shares since early 2013. That is regardless of aggressive M&A throughout this era.

So, simply to reiterate as a result of it is so spectacular:

- URI operates in a extremely cyclical trade.

- It has grown via natural progress and aggressive acquisitions.

- It has a really wholesome steadiness sheet and a long-term decline in its leverage ratio.

- It has engaged in aggressive buybacks for greater than a decade.

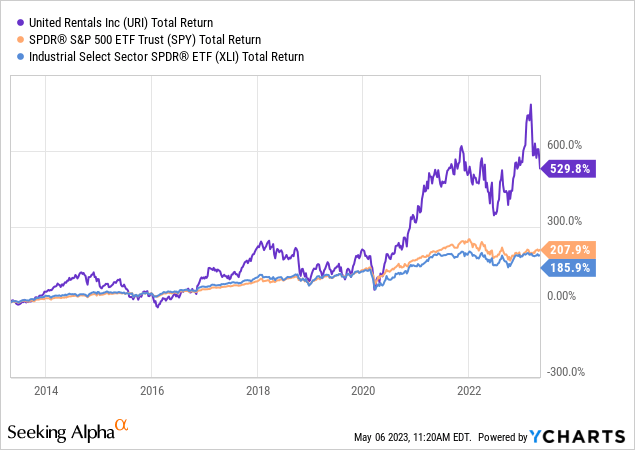

Therefore, it is no shock that the inventory has outperformed the market and industrial sector friends by a large margin.

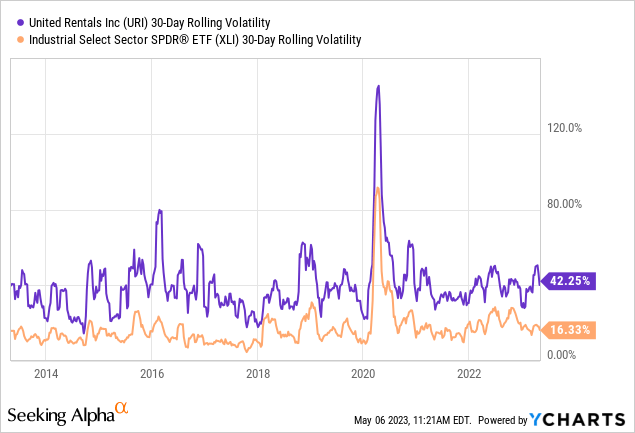

Nonetheless, URI comes with excessive volatility. The corporate’s 30-day rolling volatility is persistently near 40%, which is excessive for a person inventory.

Excessive volatility is accompanied by common and steep downturns. Nonetheless, these drawdowns usually are not random.

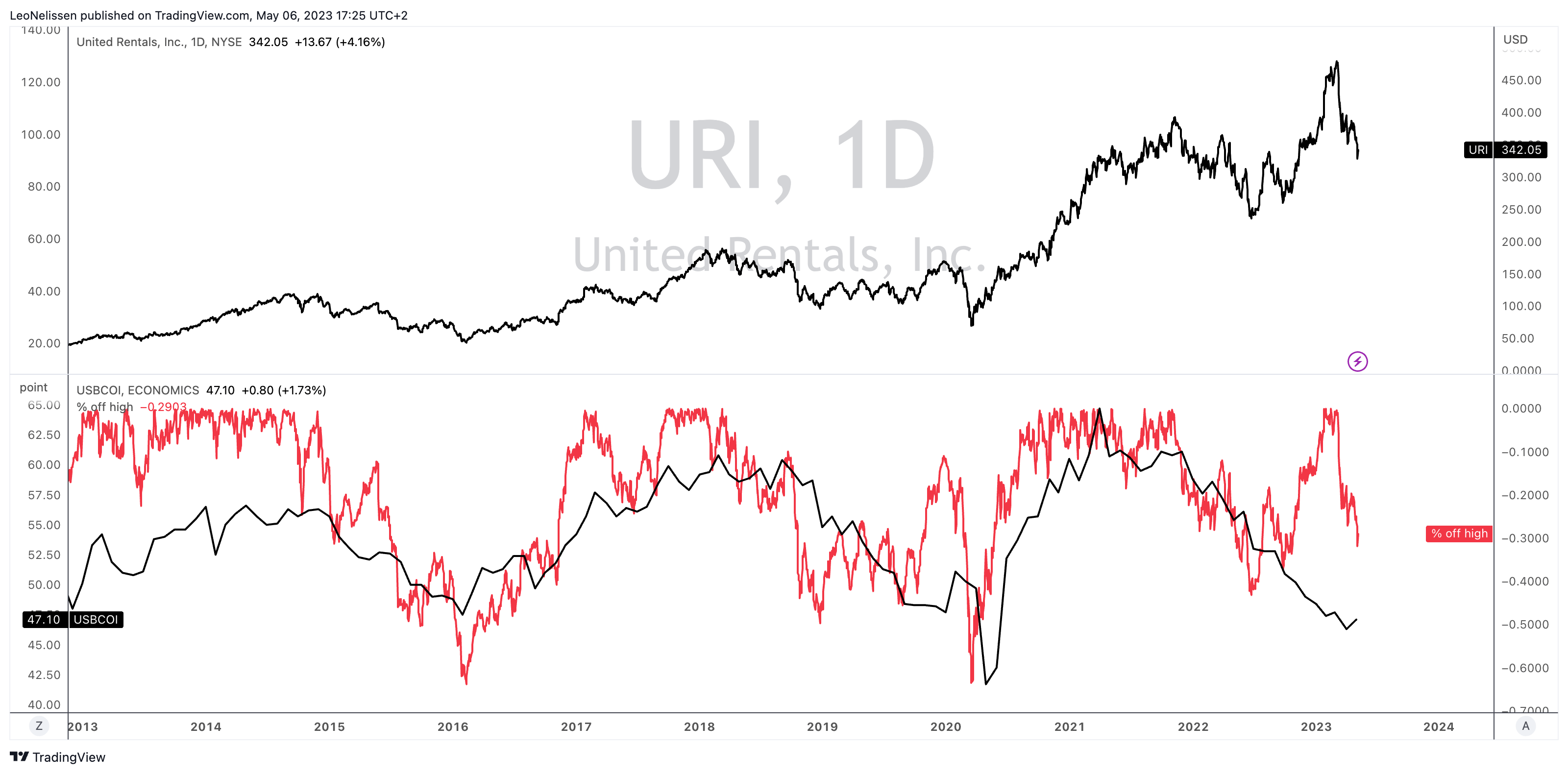

The chart beneath compares the URI inventory worth efficiency (% off its all-time excessive) to the ISM Manufacturing Index. URI completely follows financial expectations, which is sensible, as its enterprise is cyclical.

TradingView (URI, ISM Index)

The truth that financial progress is in a steep downtrend can be the explanation why I advised readers to attend for weak spot in February.

Most of the time, URI shares fall 40% to 60% throughout manufacturing downturns. The present downturn is 30%.

This brings me to the just-released earnings.

Recession? What Administration Has To Say

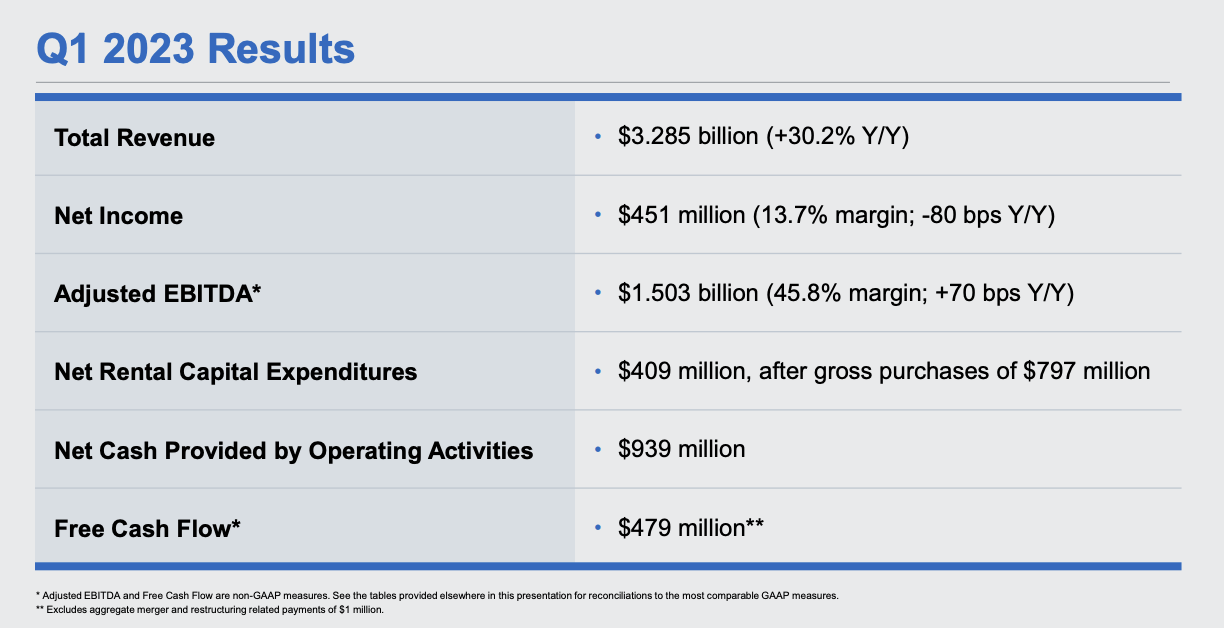

In 1Q23, URI reported a 30.6% income enhance to $3.29 billion, beating analyst estimates by $120 million. Adjusted EPS got here in at $7.95, which missed estimates by $0.04.

United Leases

What’s fascinating is that URI noticed progress throughout all of its areas, together with double-digit progress. Non-residential development, industrial manufacturing, and energy all noticed optimistic progress. The corporate’s specialty enterprise delivered nice outcomes, with rental income up 24% year-on-year and excessive progress throughout all traces of enterprise, particularly the cellular storage staff. URI opened six new places and is on observe for round 40 chilly begins this 12 months.

URI is optimistic about its enterprise and the optimistic trade indicators for the steadiness of 2023 and past. The corporate stays assured in its capability to capitalize on vital multi-year tailwinds for the rental tools trade, which they consider are resilient in any financial setting. URI is well-positioned to help its clients as they undertake tasks throughout clear power and superior manufacturing funded by the Inflation Discount Act. The tailwinds maintain the potential for over $2 trillion of undertaking spending within the US over the following decade.

It stays early, however we proceed to see a ramp in spending from the federal infrastructure invoice throughout a wide range of undertaking sorts, together with airports, bridges and highway and freeway. We’re additionally effectively positioned to help our clients as they undertake tasks throughout clear power and superior manufacturing funded by the Inflation Discount Act.

Inside personal development, we proceed to see robust investments throughout manufacturing, led by autos, semiconductors and power and energy. Mixed studies point out that these tailwinds maintain the potential for over $2 trillion of undertaking spend within the U.S. over the following decade.

The corporate is true when it mentions secular tailwinds like financial re-shoring. I’ve been bullish on this for some time. As a matter of truth, URI is one in all my high picks in that space.

Nonetheless, buyers do not care about that. Financial indicators are poor, which causes buyers to be extra petrified of short-term ache than long-term positive factors.

That is regular for cyclical shares and nice for buyers trying to purchase on weak spot.

Valuation

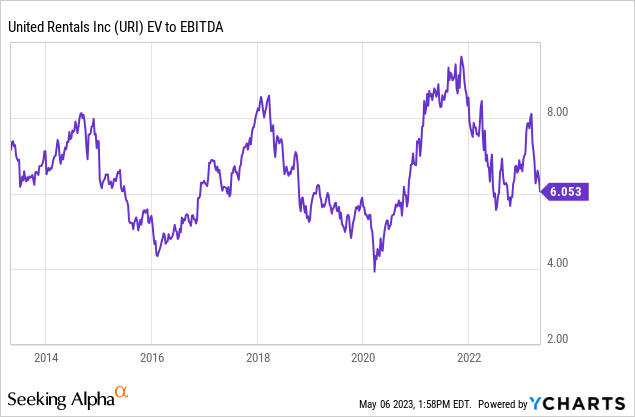

URI is buying and selling at 6.1x LTM EBITDA. The inventory trades at 5.0x 2023E EBITDA, which is the results of analysts pricing in progress this 12 months. Add to this that the inventory is buying and selling beneath 9x subsequent 12 months’s free money move.

Simply trying on the uncooked numbers, URI is a complete steal proper now.

Nonetheless, it is not that easy – not that anybody anticipated it.

- EBITDA estimates will come down if financial progress expectations don’t recuperate quickly.

- Markets are typically irrational throughout each bear and bull markets. Even when EBITDA estimates had been to stay unchanged, the inventory might get cheaper. In any case, URI has a historical past of dropping greater than 40% throughout manufacturing recessions. That is one thing to bear in mind, even when URI is now a extra mature enterprise than it was throughout prior cycles.

When coping with a fast-growing inventory like URI, I consider the very best factor to do is to purchase progressively. Whereas I am nonetheless contemplating if I want URI (I’ve near 50% industrial publicity already), I might begin small and add progressively over time. If the inventory continues to drop, buyers can common down, which is nice for a long-term funding. If the inventory takes off, buyers have a foot within the door.

Takeaway

On this article, we mentioned United Leases, a captivating inventory working within the industrial sector. This firm is shortly taking on the tools rental trade due to aggressive M&A and a enterprise mannequin that permits for superior customer support.

Not solely that, however the firm is now at a degree the place it’s considerably rising its free money move, permitting it to keep up a really wholesome steadiness sheet, purchase again shares, and develop its just-initiated dividend at a fast tempo.

Regardless of all of this and progress outlook, URI shares are promoting off. The issue is that financial progress is slowing down, inflicting buyers to dump cyclical shares like URI.

As a lot as I just like the valuation, I might not make investments massive sums in URI. I consider that gradual shopping for is the best way to go.

My purchase score displays its longer-term potential.

{kind=link}