vadimrysev

Funding Overview

ImmunoGen (NASDAQ:IMGN) – an beneath the radar, Waltham, Massachusetts primarily based biotech based in 1981 despatched its shareholders into raptures yesterday after publishing new information from its Section 3 MIRASOL examine of its drug ELAHERE, in sufferers with FRα-Constructive, Platinum-Resistant Ovarian Most cancers (“PROC”).

Previous to yesterday’s information, ImmunoGen inventory had been buying and selling at a price of ~$4 – which is in regards to the common throughout the previous 5 yr interval. Shares ended the day buying and selling at $12.2 – their highest worth because the finish of 2015. Throughout the previous 5 years the inventory is now up simply 8.4%, though throughout the previous yr, it’s +142%.

ELAHERE Overview And Why Yesterday’s Information Is So Essential

ImmunoGen’s enterprise is targeted on the event of next-generation antibody drug conjugates (“ADCs”), a category of drug the corporate describes as follows in its Q1’23 10-Q submission (quarterly earnings and updates):

An ADC with our proprietary expertise includes an antibody that binds to a goal discovered on tumor cells and is conjugated to one in all our potent anti-cancer brokers as a “payload” to kill the tumor cell as soon as the ADC has sure to its goal. ADCs are an increasing class of anticancer therapeutics, with twelve authorized merchandise and the variety of brokers in growth rising considerably lately.

4 of the 12 approvals talked about above had been secured by the Seattle primarily based, oncology centered drug developer Seagen (SGEN), a enterprise that was just lately acquired for $43bn by Pharma large Pfizer (PFE), which helps to underline the promise the business sees in ADCs.

ELAHERE – or Mirvetuximab Soravtansine, to present it its chemical identify, is, in response to ImmunoGen:

a first-in-class ADC focusing on folate receptor alpha (FRα), a cell-surface protein over-expressed in quite a few epithelial tumors, together with ovarian, endometrial, and non-small-cell lung cancers.

In November final yr the FDA agreed to award ELAHERE an accelerated approval for the drug, as a remedy for grownup sufferers with FRα optimistic, platinum-resistant epithelial ovarian, fallopian tube, or major peritoneal most cancers, who’ve obtained one to a few prior systemic therapy regimens.

This was primarily based on information from a single arm SORAYA examine of 33 sufferers that confirmed an Goal Response Charge (“ORR”) of 31.7%, and a Period of Response (“DOR”) of 6.9 months. Analysts provided peak gross sales estimates across the $170m each year mark, though as a consequence of a earlier failed Section 3 examine during which ELAHERE failed to extend progress free survival (“PFS”) by greater than chemotherapy, had been skeptical of the influence the drug might have in an actual world setting.

ELAHERE just isn’t the primary FRA-targeting drug to have flunked a late stage trial – Japanese Pharma Eisai noticed its drug farletuzumab fail to fulfill endpoints in a Section 3 ovarian most cancers examine, while Merck (MRK) and companion Endocyte deserted a Section 3 examine of FRA-targeting candidate vintafolide in ovarian most cancers.

Yesterday’s information from Immunogen nonetheless apparently turns the thesis that focusing on FRA doesn’t work effectively in Ovarian Most cancers remedy on its head. The Section 3 MIRASOL examine, which enrolled 453 sufferers, demonstrated “a statistically important and clinically significant enchancment in OS in comparison with IC chemotherapy”, in response to a press release. The discharge goes on:

With 204 OS occasions reported as of March 6, 2023, the median OS was 16.46 months within the ELAHERE arm, in comparison with 12.75 months within the IC chemotherapy arm, with a hazard ratio (“HR”) of 0.67, p=0.0046. This represents a 33% discount within the danger of loss of life within the ELAHERE arm compared to the IC chemotherapy arm.

ELAHERE demonstrated a statistically important and clinically significant enchancment in PFS by investigator evaluation in comparison with IC chemotherapy, with a hazard ratio of 0.65 (p<0.0001), which represents a 35% discount within the danger of tumor development or loss of life within the ELAHERE arm in comparison with the IC chemotherapy arm. The median PFS within the ELAHERE arm was 5.62 months, in comparison with 3.98 months within the IC chemotherapy arm.

ORR by investigator evaluation within the ELAHERE arm was 42.3%, together with 12 full responses (CRs), in comparison with 15.9%, with no CRs, within the IC chemotherapy arm.

Anna Berkenblit, MD, Senior Vice President and Chief Medical Officer of ImmunoGen added that:

Importantly, ELAHERE is the primary drug to point out an total survival profit on this affected person inhabitants.

In brief, these outcomes had a real “wow issue” about them. When ImmunoGen had introduced the accelerated approval of ELAHERE again in November, its share worth hardly budged, once more primarily based on doubts in regards to the drug’s profile, its deliberate $6k per vial (with sufferers anticipating to obtain 3-4 vials per course of therapy) worth level, and competitors within the type of already authorized PROC medicine similar to AstraZeneca’s (AZN) Lynparza, and vascular endothelial progress issue (“VEGF”) focusing on Avastin.

Maybe surprisingly, nonetheless, pretty much as good because the MIRASOL outcomes are, some analysts haven’t noticeably raised their peak gross sales expectations for the drug. SVB Securities apparently raised expectations from $170m each year, to $210m, on the idea that probabilities for achievement in platinum delicate ovarian most cancers remained low, and in addition pointing to 55% of sufferers who obtain AstraZeneca’s PARP inhibitor Lynparza through the MIRASOL examine.

However, Piper Sandler upgraded ImmunoGen inventory, noting the outperformance in Total Survival, and elevating its worth goal to $16 per share, from $6 per share.

ELAHERE – What Occurs Now?

It may appear odd that such an necessary, share worth needle transferring information win might not translate to a income alternative that helps ImmunoGen’s new market cap valuation of $2.8bn. Based mostly on peak gross sales expectations of $210m each year, we have now a ahead worth to gross sales ratio of ~13.3x, which both signifies that ImmunoGen inventory is now considerably overvalued, or that the market believes there’s a lot to come back from this drug, this firm, and this firm’s pipeline.

Actually, ImmunoGen will now have the ability to submit a supplemental Biologics License Software (“sBLA”) and virtually actually obtain a full approval for ELAHERE, doubtless this yr. That is the primary new PROC drug to be authorized since 2014, and ELAHERE revenues in Q1’23 had been $29.5m, which looks as if a formidable begin, plus administration says it has protection insurance policies in place for ~55% of Medicare and ~70% of economic lives.

In keeping with ScienceDirect:

Platinum-resistant ovarian most cancers, typically outlined as development occurring inside 6 months after finishing platinum-based remedy, happen in about 20 % of the sufferers after first-line platinum-based remedy

If my understanding is appropriate that subsequently makes platinum delicate ovarian most cancers (“PSOC”) the a lot bigger market, and regardless of analysts’ skepticism, it’s a goal marketplace for ImmunoGen, with ELAHERE being evaluated as a monotherapy on this indication.

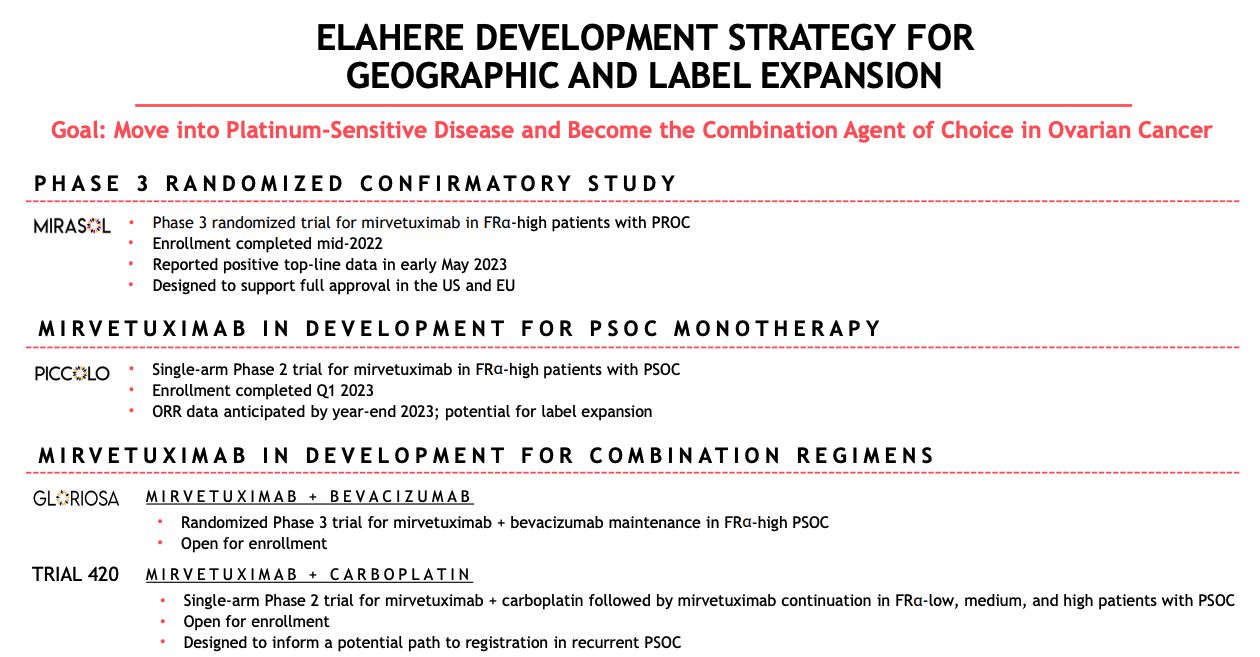

ELAHERE growth technique (ImmunoGen presentation)

As we are able to see above, moreover MIRASOL, there’s a Section 2 PICCOLO examine evaluating ELAHERE as a monotherapy in PSOC ongoing, with information anticipated this yr, and a pair of additional research, GLORIOSA and TRIAL 420, evaluating the drug in combo with Swiss Pharma Roche’s (OTCQX:RHHBY) Avastin, and chemo drug Carboplatin.

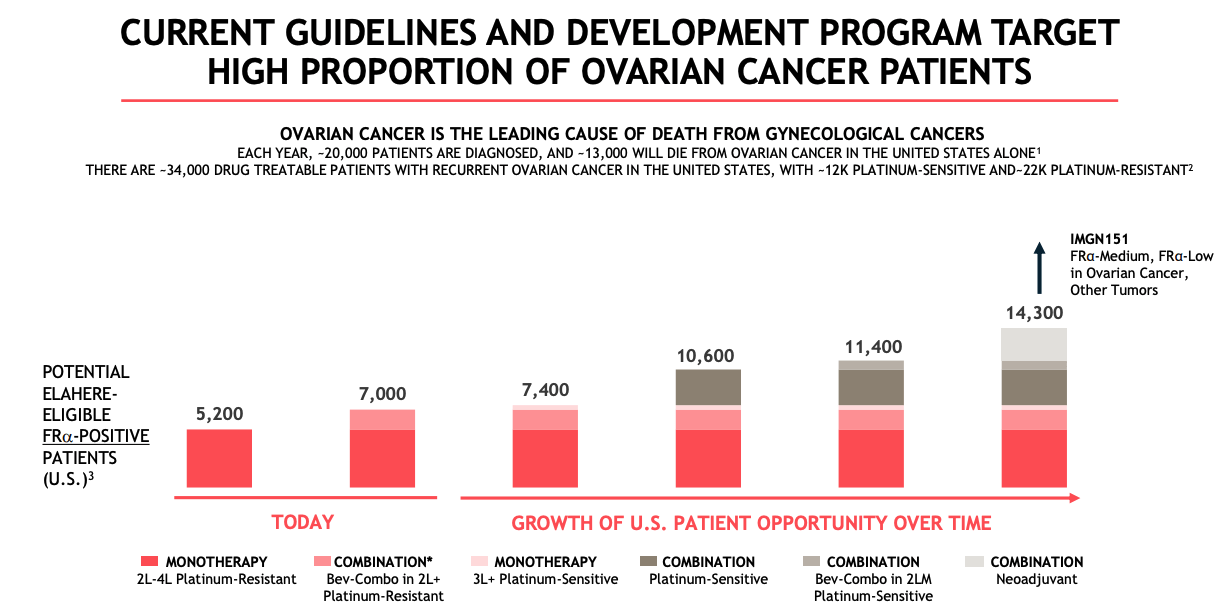

ImmunoGen affected person alternative forecast for ELAHERE (ImmunoGen presentation)

As we are able to see above, if all research had been to achieve success – and that’s removed from assured, it ought to be pressured – then ELAHERE’s goal market might improve from 5k sufferers right this moment, to >14k if all label expansions are authorized. Based mostly on the close to 3x improve in sufferers, an optimistic situation would possibly recommend that ELAHERE might go on to realize blockbuster (>$1bn each year) gross sales in Ovarian Most cancers alone.

ELAHERE has not but secured approval in Europe and the UK, though this appears more likely to occur quickly primarily based on the info, which will increase the whole addressable market (“TAM”) nonetheless additional, while ImmunoGen additionally has a Chinese language companion – Huadong Medication – who might pay ImmunoGen as much as $265m extra if growth and approval milestones are met.

Plus, ELAHERE just isn’t ImmunoGen’s solely ADC candidate. Pivekimab Sunirine is being evaluated in 2 Section 2 research, in sufferers affected by Blastic plasmacytoid dendritic cell neoplasm (“BPDCN”), and Acute Myeloid Lymphoma (in combo with chemo medicine), while IMGC936 is in Section 1 research in varied stable tumor cancers, and IMGN151 in a Section 1 examine endometrial cancers.

ImmunoGen reported a money place of $201m as of Q1’23, and complete revenues of $49m, though complete prices and working bills amounted to $92.3m, leading to a loss from operations of $42.4m. As so many biotechs do on the again of a superb date launch, the corporate has instantly moved to lift $200m through a share providing, which suggests present shareholders will undergo some dilution, though they’ll probably expect a superb return on the $200m raised.

Some Dangers Round ImmunoGen To Think about

With near $400m in money, regardless of making a web lack of $223m in 2022 ImmunoGen must have enough funding for the subsequent couple of years, particularly now that the corporate is producing revenues. FY23 steerage is for $45 – $50m of non-ELAHERE revenues, and OPEX of $320 – $335m. No forecast for ELAHERE revenues is supplied, but when we assume gross sales in later quarters match Q1, that determine could be ~$120m, and web loss would are available at round $160m for the yr.

As such, ImmunoGen will stay a loss-making firm in 2023, and contemplating its present market cap of practically $2.8bn, that does make the present share worth look just a little excessive.

Though ImmunoGen is having fun with a primary mover benefit for an ADC in PROC, an announcement within the firm’s 2022 10K submission discusses its competitors as follows:

Mersana Therapeutics (MRSN), Eisai (OTCPK:ESAIY), and Sutro BioPharma have clinical-stage ADCs focusing on platinum resistant ovarian most cancers, and Pfizer, Seattle Genetics, Roche, Astellas, AstraZeneca, Daiichi Sankyo, GlaxoSmithKline (GSK), AbbVie (ABBV), and the Menarini Group have packages to connect a cell-killing small molecule to an antibody for focused supply to most cancers cells.

With competitors coming within the type of main Pharmas with huge R&D and advertising and marketing budgets similar to Eisai in PROC and AbbVie (ABBV) and Pfizer within the ADC house, it’s potential that ImmunoGen and ELAHERE could possibly be overwhelmed, while the present competitors towards e.g. Lynparza and chemotherapies will proceed. In brief, ImmunoGen might not have the higher hand in, or unique entry to its goal markets and the corporate has very restricted business expertise.

Concluding Ideas: Excellent Outcomes Improve ImmunoGen’s Repute – Though The Highway Forward Stays Considerably Unclear

When a biotech firm launched information as spectacular as ImmunoGen did yesterday with the announcement of its MIRASOL Section 3 information, it deserves to be rewarded as such conclusive information readouts are uncommon. As such, I’m not shocked to see the corporate’s share worth spike in a single day – nonetheless the subsequent query is whether or not the positive factors are sustainable.

The low peak gross sales forecasts for ELAHERE are a priority, for my part, though an approval in Europe and the UK might improve expectations from ~$210m, to ~$350m. That is nonetheless not sufficient to help a $2.8bn market cap, subsequently it does appear necessary that ImmunoGen can penetrate the PSOC market, and that it continues to work on its different ADC property.

One other worth enhancing occasion that I might not rule out is a big Pharma providing to buyout ImmunoGen – this could possibly be achieved for >$10bn, for my part. A Pharma would have few qualms about paying ~$7.5bn for a drug producing the type of information that ELAHERE has, plus 3 different candidates and a expertise platform that additionally helped develop KADCYLA – a marketed ADC ensuing from a growth and commercialization license with Roche. Clearly, ImmunoGen shareholders could be delighted to make a ~270% additional acquire on their funding – after yesterday’s positive factors.

Roche might in reality be the client, or maybe Eli Lilly (LLY), given the two corporations are already working collectively on creating property in a program that has the “potential for as much as $1.7 billion in growth and sales-based milestone funds if all targets are chosen and all milestones are realized”, in response to ImmunoGen’s 10K submission.

However, within the brief time period ImmunoGen nonetheless has a whole lot of work to do, and a key information readout to come back on the finish of this yr when PSOC monotherapy information is shared. Since biotech valuations are likely to drift downward when there aren’t any notable near-term catalysts in play, I might be ready to attend and see if ImmunoGen’s shares lose just a little of their worth within the coming months as share choices and the realities of making an attempt to develop market share in a presently powerful buying and selling atmosphere hit dwelling.

As a biotech inventory watcher I want I had paid extra consideration to ImmunoGen – particularly within the wake of Pfizer’s buyout of Seagen – and invested forward of yesterday’s outcomes, though the danger might effectively have seemed too excessive again then owing to the prior Section 3 fail. There could possibly be rather more to come back from ImmunoGen inventory, nonetheless, and if I see the share worth slip again into the only digits whereas the present upside catalysts are nonetheless in play, I might be tempted to purchase.

{kind=link}