Marcus Lindstrom/E+ through Getty Pictures

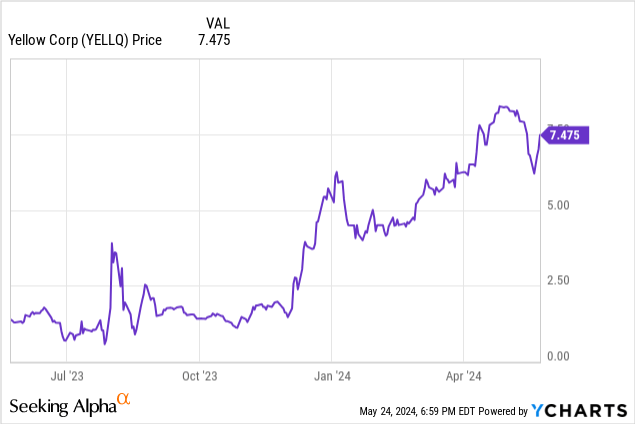

The Ch.11 liquidation of bankrupt Yellow Corp. (OTC:YELLQ) has made vital progress over the past ten months. Receipts whole $2,407,864,963 as of April 30 (docket 3442) and disbursements whole $2,206,688,213. The present whole money is $327,659,423 or about $6.29 per share in comparison with the most recent YELLQ inventory value of $7.47. With a view to justify the present inventory value, further asset gross sales should be higher than further bills and recoveries paid to unsecured collectors. That could possibly be an issue. As well as, the time worth of cash must be factored in as a result of it could possibly be a very long time earlier than there are any funds to shareholders.

The cash obtained to date contains $1.88 billion from the public sale sale of 130 owned properties and $92 million from the sale of 23 leased properties. Yellow additionally obtained money from amassing on accounts receivables, promoting gas oil and tires, and from the sale of rolling inventory. They used a part of the money obtained to repay all their prepetition secured debt, together with $737 million plus curiosity to the federal authorities, and DIP financing. Money has additionally been used to pay wages, utilities, taxes, {and professional} charges.

Official Committee of Unsecured Collectors – Membership Change

A significant motive why I by no means purchased YELLQ final 12 months was that I didn’t just like the composition of the Official Committee of Unsecured Collectors appointed by the U.S. Trustee, which I lined in my November 27 article. There have been 5 members related to labor/pension fund organizations of the 9 members. This share simply acquired worse. Michelin North America, Inc. resigned in early Could (docket 3430), which implies 5 out of the eight committee members at the moment are related to labor/pension funds who’re attempting to get recoveries for the roughly $7.8 billion MEPP and over $1.0 billion WARN Act claims.

The committee appears to have modified its method to the chapter course of after Michelin’s resignation. On April 18, the Committee filed a docket supporting the corporate’s objection to arbitration to settle numerous pension claims (docket 3057), however on Could 21, the Committee filed a movement of deposition (docket 3440) for discovery relating to the movement filed by Yellow Corp. to increase the exclusivity interval 90 days to file a reorganization plan to September 2 from June 3 and solicit acceptance of the plan to October 25 (docket 3433). What? Normally, these extension motions are simply “rubber stamped” with no objections. A June 3 listening to will embrace the extension movement. This means to me the Committee’s method might have modified from working with the corporate throughout the chapter course of to changing into probably adversarial. This isn’t good for YELLQ shareholders.

Massive Authorized/Skilled Charges Are Impacting Shareholders

Earlier than wanting on the standing of assorted litigations, it is very important level out the potential for very excessive authorized/skilled charges that receives a commission from money earlier than shareholders get something. Authorized/skilled charges paid to date whole $68,038,916 as much as April 30 (docket 3332), together with $13.441 million paid in April. These are paid charges. Many providers haven’t even been billed but. For instance, their lead counsel, Kirkland & Ellis has been paid $19,389,660, however that’s solely as much as January 31. They’re within the technique of attempting to receives a commission $2,593,892.80 (billed $3,242,366.00 and there’s a 20% holdback) for February. (dockets 3489 and 2942). Kirkland & Ellis may simply invoice over $3.2 million per 30 days from March 1, 2024 to March 1, 2025 as a result of there are a number of trials later this 12 months and the Ch.11 plan/disclosure assertion haven’t even been negotiated but. There are various different consultants and legislation corporations that will even proceed to invoice. These professionals invoice at very excessive charges – some Kirkland & Ellis companions invoice at $2,305/hour. When your entire Ch 11. Chapter course of is accomplished, I’d not be stunned if the authorized/skilled charges whole over $160 million, which is near $3 per YELLQ share.

Replace on Lawsuits

There are a variety of important lawsuits that may impression the quantity, if any, YELLQ shareholders obtain. Numerous labor organizations wished their pension claims, which whole about $7.8 billion, to be dealt with by arbitration as a substitute of by the chapter court docket, which I lined in my February article. Chapter Choose Craig T. Goldblatt determined that the chapter court docket will hear the pension claims – not through arbitration (docket 2765). This was a significant win for shareholders. If the claims have been dealt with through arbitration, different collectors and shareholders wouldn’t be included within the arbitration course of. With the chapter court docket now deciding if the pension claims needs to be allowed and for a way a lot, if any, different collectors and shareholders, equivalent to MFN that owns 42.5% of the inventory, can take part within the course of, together with participation throughout hearings on this subject.

Except there’s a negotiated settlement, there almost definitely might be appeals to the federal district court docket by the dropping events if the claims course of is set both by arbitration or the chapter court docket. For my part, the chapter court docket course of will make it extra seemingly there might be a negotiated settlement sooner fairly than later as a result of all of the events can take part as a substitute of simply the corporate, labor organizations, and the arbitrator. A listening to is presently set for August 5.

I lined the potential WARN Act liabilities in my November article, however I wish to replace the standing of the present $1.0 billion litigation. As anticipated, Yellow rejected the WARN claims (docket 2578) and the Teamsters filed a response (2778) in March. A trial is presently set for September 23-27. There may be an attention-grabbing technicality which will favor Yellow. The Third Circuit Court docket made an attention-grabbing ruling in Varela v. AE Liquidation, Inc. (No. 16-2203):

On attraction, we’re requested to find out whether or not a enterprise should notify its workers of a pending layoff as soon as the layoff turns into probable-that is, extra seemingly than not-or if the mere foreseeable risk {that a} layoff might happen is sufficient to set off the WARN Act’s discover necessities. As a result of we conclude {that a} likelihood of layoffs is important…”

The Teamsters, subsequently, must persuade the court docket {that a} layoff was “possible” (extra seemingly than not). That may be a a lot greater bar than simply “attainable”.

A federal choose dismissed the lawsuit Yellow Company et al., v. Worldwide Brotherhood of Teamsters et al. (Case No. 23-1131-JAR-ADM) in March. Yellow was looking for “$137 million in damages for the Union’s obstruction of Section 2, in addition to the lack of Yellow’s enterprise worth, which it estimates at roughly $1.5 billion”. Whereas just a few YELLQ shareholders have been anticipating that the corporate may get some cash from this litigation, it was an extended shot. The choose asserted that there was a course of to resolve these points outdoors of the court docket. In principle, the case may return into court docket as a result of it was dismissed with out prejudice, however I believe it’s extremely unlikely.

Present YELLQ Inventory vs Potential Recoveries

In attempting to find out potential recoveries for YELLQ shareholders requires utilizing some previous numbers, however it ought to nonetheless give a good “back-of-the-envelope” estimate. The most recent SEC submitting for Yellow Corp was a 2Q 2023 10-Q for the quarter ending June 30, which was about 5 weeks earlier than the corporate filed for chapter.

All of the prepetition secured debt and the DIP have already been paid. Another liabilities equivalent to prepetition salaries have additionally been paid already. The $171.7 million accounts payable and the $40.3 million “different accrued and present liabilities” as of June 30 will almost definitely be categorised as common unsecured claims that must be paid earlier than shareholders get a restoration. The precise allowed claims from these previous numbers is unsure, however they’re a place to begin. From this $212 million ($171.7 million + $40.3 million) $18.5 million prepetition important distributors have already been paid. There was additionally a complete of $12.7 million setoffs to date with different events the place Yellow owed cash and the opposite social gathering owed Yellow. That brings the full right down to $180.8 million.

There are two main objects that might be paid from their money place. The authorized/skilled charges that I estimate will whole no less than $160 million implies that a further $92 million might be paid earlier than shareholders get a restoration. Since Yellow Corp nonetheless has some workers and different month-to-month bills, there might be a future money burn, which I’m estimating at $7 million/month. As extra belongings are bought, there might be fewer workers, decrease insurance coverage bills, decrease property taxes, and decrease utility bills, so one cannot simply use numbers in prior MORs, however these prior numbers nonetheless do give some perception into the potential month-to-month money burns. For the sake of dialogue, I’m utilizing 12 months from April 30 till April 30 subsequent 12 months @ $7 million/month to get a complete money burn of $84 million.

Including $180.8 million, $92 million, and $84 million leads to a complete of $356.8 million. Yellow’s money as of April 30 was $327.7 million. This suggests a possible destructive money of $29.1 million. The present whole fairness worth of YELLQ inventory is $390 million. This suggests traders expect no less than $419.1 million from further asset gross sales and even ignores the time worth of cash and potential WARN/pension claims. Or it implies that traders expect some mixture of decrease authorized/skilled charges, decrease month-to-month burn charges, or decrease authorised claims based mostly on 2Q’23 numbers than my estimates.

Continued Asset Gross sales

A significant supply of more money will come from promoting their tractors and trailers. The sale of their rolling inventory belongings by Ritchie Bros. has, nevertheless, been disappointing. Initially, my tough estimate of the quantity they’d obtain was $487 million after charges, which I lowered to $438 million in my February article. Based mostly on the poor outcomes to date and since used tractor and trailer costs have plunged since my unique estimate, I’m decreasing that estimate to $310 million. The used truck market within the first quarter of this 12 months was very weak, however it has lately stabilized considerably. That discount of $177 million is roughly $3.40 per YELLQ share.

Summing up all of the reported particular person promoting transaction within the MORs, Yellow obtained a complete gross quantity of $56.734 million for 14,132 rolling inventory models as of April 30. The quantity obtained to date is earlier than charges of 9.25%. The corporate initially said that they had roughly 11,700 tractors and 34,800 trailers to promote. [They are also abandoning 93 units (docket 3498)] It, subsequently, appears they’ve over 32k models remaining to be bought. I’d warning readers about utilizing the typical quantity obtained to date per unit as a result of the worth vary within the particular reported gross sales was extraordinarily vast. At this level, I ponder if they’re holding again a few of their extra useful tractors and trailers till the used market improves. For the reason that MORs use money accounting, there may really be a major quantity which were “bought”, however the money transaction has not closed but and is, subsequently, not reported within the MOR.

Utilizing the estimated $310 million and $51.5 million obtained to date, which displays the 9.25% charge, an estimated $258.5 million money could possibly be obtained from the sale of their rolling inventory fleet. Subtracting that quantity from $419.1 million, $160.6 million must come from different sources. I lined the accounts receivable subject in my final article, and I doubt they’ll get a lot more money from pre-petition accounts receivable at this level. They’re simply too “previous”. That leaves the sale of actual property – each owned and leased.

Yellow is attempting to imagine 78 leased properties with the intention sooner or later to assign these leases (dockets 2157, 3076, 3086). How a lot they may get for every lease is simply hypothesis. As well as, there could possibly be continued litigation over any very useful lease. Yellow additionally has 39 owned properties, based mostly on my calculations, that they wish to promote. Once more, it’s pure hypothesis to estimate the eventual proceeds from these gross sales. Among the costs for properties already bought weren’t simply based mostly on the variety of “doorways”, but additionally on useful land that could possibly be developed.

I believe that it’s pretty affordable to count on that these properties collectively might be bought for greater than $160.6 million. Even when these properties are bought considerably greater than $160.6 million, the potential claims from numerous pension/WARN litigations must be paid earlier than YELLQ shareholders get any restoration. Negotiated settlements of 10 cents on the greenback leads to about $880 million allowed unsecured claims, which might almost definitely imply no restoration for shareholders. MFN would by no means conform to a settlement that wipes them out. Any settlement must give MFN and different YELLQ shareholders a significant restoration or they’d fairly struggle within the courts.

(Word: The month-to-month working studies – MORs usually are not based mostly on GAAP accounting. They’re based mostly on U.S. Trustee requirements and will be very complicated as a result of intercompany objects usually are not cancelled out, which is completed beneath GAAP. The Trustee is usually concerned with money and who was paid money throughout the month. For instance, the most recent MOR exhibit (docket 3445) exhibits whole pre-petition liabilities of $8,228,382,000 for Yellow Corp. That’s method too excessive.)

Conclusion

I’m downgrading YELLQ to a “promote” from “maintain” as a result of: 1) the inventory value is already up 315% from my November article and up 66% from my February article; 2) the rolling inventory gross sales to date have been very disappointing; 3) there was a membership change on the Official Committee of Unsecured Collectors; 4) hovering authorized/skilled charges; 5) time worth of cash – litigations may take years except there are settlements; 6) the continued threat that shareholders may get no recoveries if labor/pension funds win their litigations.

Editor’s Word: This text discusses a number of securities that don’t commerce on a significant U.S. alternate. Please concentrate on the dangers related to these shares.

{kind=link}