JHVEPhoto

Funding Thesis: Marriott Worldwide may see modest upside till we see proof that RevPAR progress can speed up heading into the summer time months. I proceed to fee the inventory as a maintain – in keeping with my prior article.

In a earlier article again in February, I made the argument that Marriott Worldwide (NASDAQ:MAR) may even see a plateau in progress within the quick to medium-term, owing to modest progress in RevPAR and a decline within the Ritz-Carlton’s common every day fee – indicating a plateau in demand for higher-priced manufacturers.

Since then, we’ve seen the inventory descend barely by slightly below 3% on the time of writing:

Investing.com

The aim of this text is to evaluate whether or not my prior outlook on Marriott Worldwide nonetheless holds taking current outcomes into consideration.

Efficiency

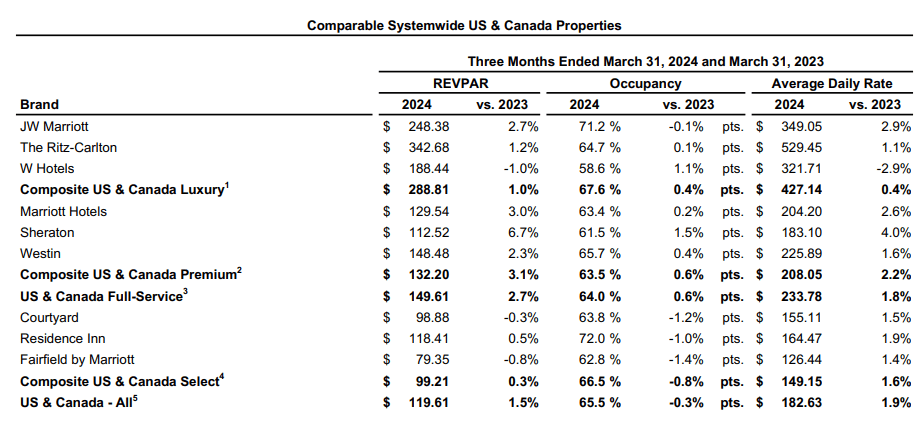

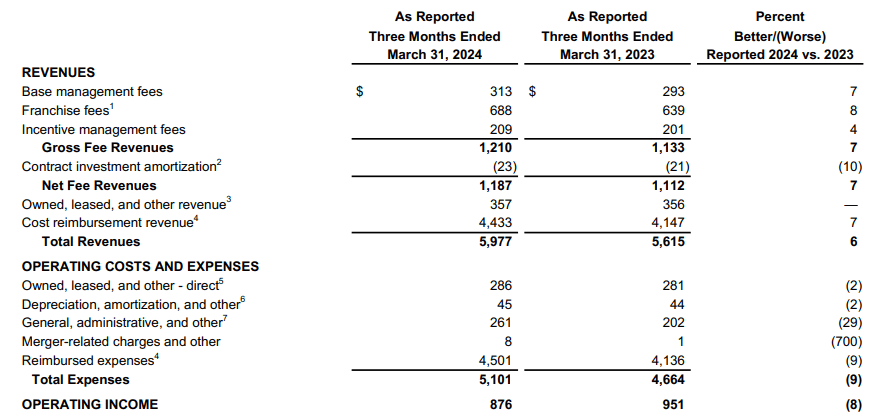

When Q1 2024 earnings results (as launched on Might 1), we will see that throughout all US & Canada system-wide properties – ADR (common every day fee) was up by 1.9% from that of the prior yr quarter, whereas RevPAR was up by 1.5% over the identical interval, with a decline in occupancy of -0.3%.

Marriott Worldwide: Q1 2024 Earnings Launch

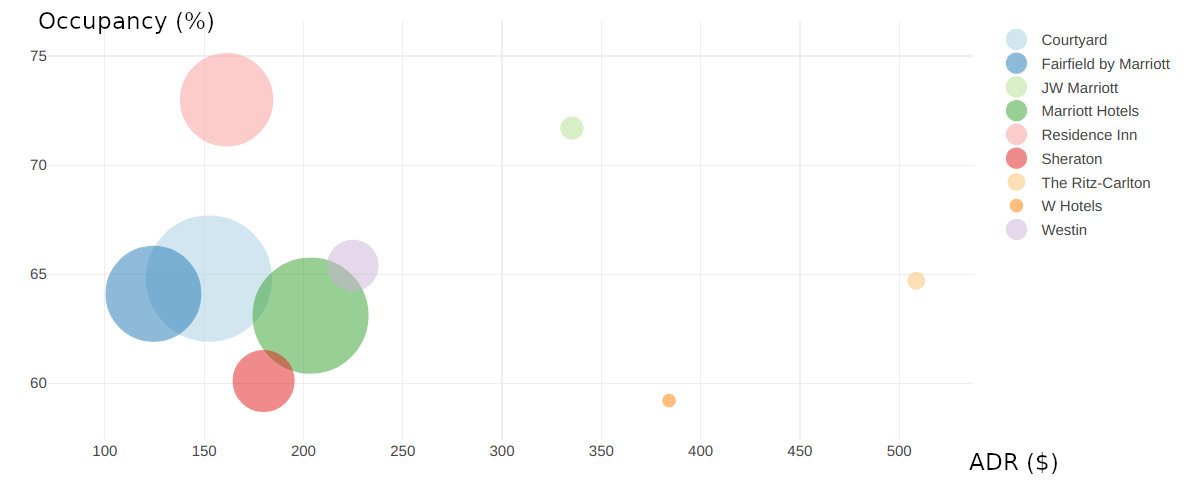

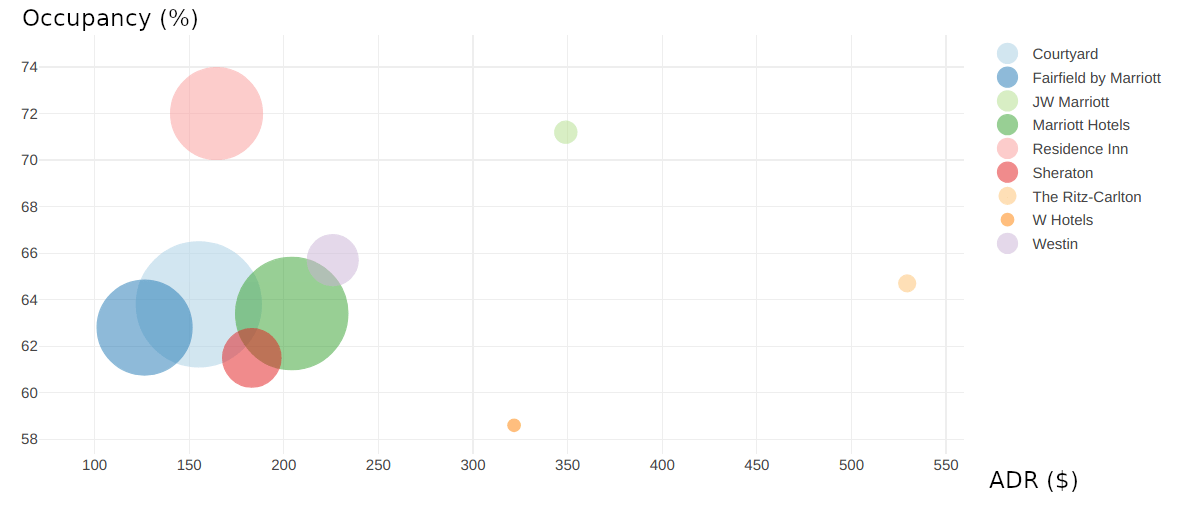

The beneath illustrates a plot of ADR (common every day fee) vs. occupancy (%) by model, with bubble measurement representing the variety of rooms by model. When model efficiency for Q1 2024 versus the prior yr quarter, we will see that the most important manufacturers by room measurement even have decrease ADR than their higher-priced friends, which cater to a smaller set of luxurious clients.

Among the many increased ADR manufacturers, we will see that whereas W Inns noticed a drop in ADR of -2.9% as in comparison with the prior yr quarter – each the Ritz-Carlton and JW Marriott noticed progress of 1.1% and a pair of.9% in ADR respectively, and additionally it is notable that occupancy for these manufacturers was notably increased than that of W Inns.

An interactive web-based model of the beneath graphs is offered here.

Q1 2023

Graph created by writer utilizing Shiny Net Apps. Related figures sourced from Marriott Worldwide Q1 2023 Earnings Launch.

Q1 2024

Graph created by writer utilizing Shiny Net Apps. Related figures sourced from Marriott Worldwide Q1 2024 Earnings Launch.

From this standpoint, the truth that we’ve seen progress in ADR (and RevPAR) for Ritz-Carlton is encouraging – notably on condition that Q1 represents off-season for journey throughout the US and Canada owing to the winter months.

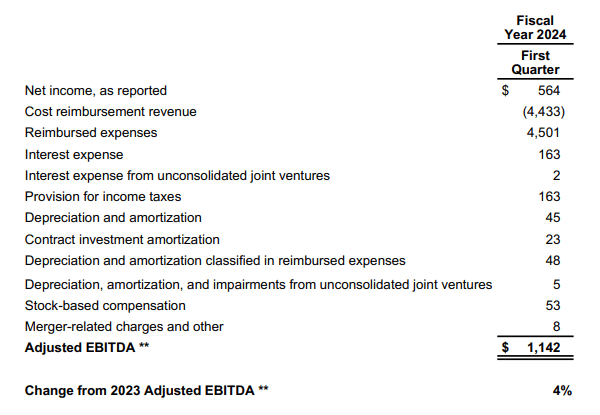

When a breakdown of net income – we will see that adjusted EBITDA is up by 4% as in comparison with the prior yr quarter.

Marriott Worldwide, Inc. Press Launch Schedules Desk Of Contents Quarter 1, 2024

Nonetheless, additionally it is notable that web earnings this quarter was decrease at $564 million as in comparison with $757 million within the prior yr quarter, and adjusted EBITDA was increased primarily on account of a rise in reimbursed bills.

My Perspective and Wanting Ahead

As regards my tackle the above outcomes and prospects for the inventory going ahead – we will see that whereas RevPAR progress has remained on an upward trajectory, general progress has been modest.

As well as, whereas complete revenues noticed progress of 6% from that of the prior yr quarter, this was outweighed by a 9% improve in reimbursed bills – in the end leading to an 8% drop in working earnings.

Marriott Worldwide, Inc. Press Launch Schedules Desk Of Contents Quarter 1, 2024

From this standpoint, I proceed to take the view that RevPAR progress must speed up for Marriott Worldwide to see additional progress from right here.

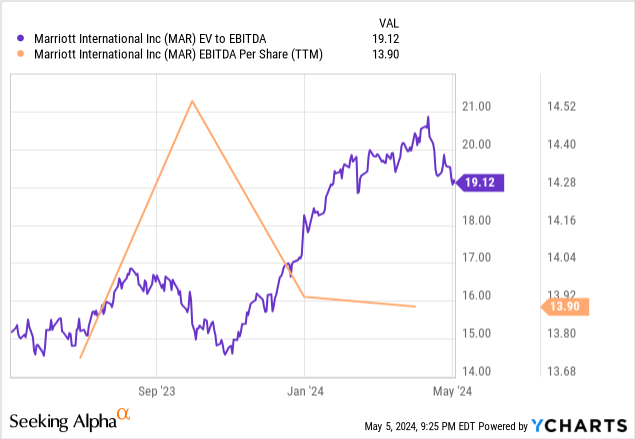

We additionally see that the EV to EBITDA ratio has seen a rise over the previous yr – with EBITDA per share failing to see sustained good points.

YCharts

For my part, the inventory is prone to see little progress from right here till we see a big acceleration in each revenues and EBITDA.

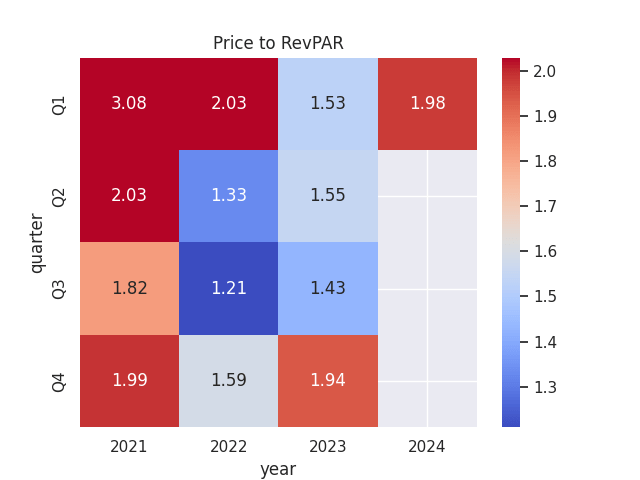

Furthermore, when worth to RevPAR (worldwide), we will see that the ratio is now at its highest degree since Q1 2022 – indicating that inventory worth has turn out to be costlier relative to the quarterly worldwide income per accessible room.

Value to RevPAR calculated by writer utilizing costs sourced from nasdaq.com and historic quarterly earnings statements for Marriott Worldwide. Heatmap generated by writer.

For my part, this additional serves as proof that the inventory is doubtlessly buying and selling at a premium at the moment. Having beforehand cited a goal of $210 for the inventory – we may see some consolidation of inventory worth on this course till RevPAR sees vital progress, and we see a lower cost to RevPAR ratio going ahead.

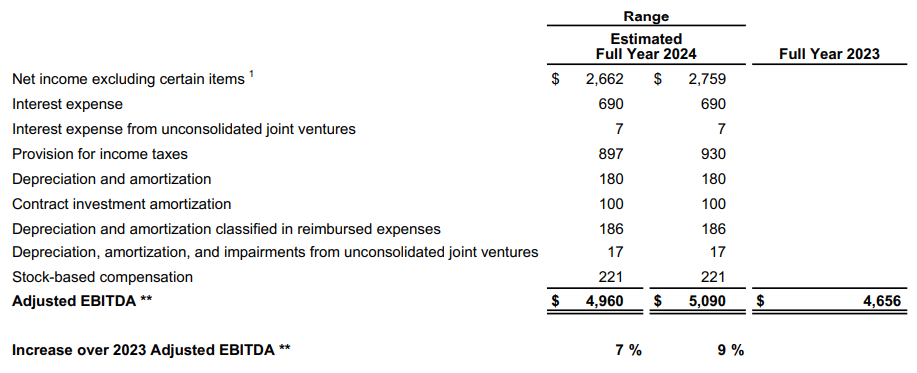

For the complete yr 2024, Marriott Worldwide is forecasting potential progress of seven% to 9% in adjusted EBITDA.

Marriott Worldwide, Inc. Press Launch Schedules Desk Of Contents Quarter 1, 2024

Whereas RevPAR efficiency over the summer time months stays to be seen, I take the view that reaching this might be unlikely except we had been to see vital RevPAR progress. I’d count on at the least a 6% progress in systemwide RevPAR throughout US & Canada for the upcoming quarter – which is similar fee of progress that we noticed for Q2 2023. An impediment to reaching this will likely be what Marriott sees as a “normalization” in home U.S. trip bookings, with leisure spending within the US and Canada exhibiting indicators of moderating.

Furthermore, with a good portion of Marriott’s properties catering to a “midscale” class of consumers and above – this might make it harder for Marriott to considerably improve income on the idea of quantity progress throughout extra mainstream manufacturers.

As such, whereas RevPAR efficiency may are available higher than anticipated – I in the end take the view {that a} normalisation of RevPAR would make it harder for Marriott Worldwide to realize an adjusted EBITDA vary of seven% to 9%.

Conclusion

To conclude, I proceed to take the view that Marriott Worldwide stays a maintain at the moment.

Going ahead, I count on that we must always see some seasonal RevPAR progress heading into the following quarter because the summer time months strategy – and I’ll notably be searching for proof that Q2 RevPAR progress considerably exceeds that of the prior yr quarter going ahead. Ought to progress be modest (e.g. just like the expansion of 1.5% that we noticed for Q1), then this might imply low progress prospects for the inventory within the quick to medium-term.

Whereas the inventory does have potential for longer-term upside if the corporate can meet its EBITDA progress goal of seven%-9% for this yr, RevPAR progress has remained fairly modest and the inventory may see little progress till we see proof that progress has the capability to rise as we head in the direction of the summer time months.

{kind=link}