tadamichi

Historic knowledge exhibits that the huge, huge majority of investments carry out poorly.

That is true for bonds, shares, and actual property as asset lessons. Almost all of it makes for a foul funding for out of doors passive traders.

And what I will present on this piece is that that is each regular and unavoidable. And unintuitively, I will additionally present that it doesn’t suggest that the majority of these investments should not have occurred. But it surely does inform us quite a bit about how we should always attempt to make investments as allocators of capital.

A Historical past of Duds

Whether or not we take a look at bonds, shares, or actual property, the returns for many investments are unhealthy. The highest outliers account for a lot of the returns.

We are able to undergo them one-by-one to quantify how unhealthy they’re:

Historic Bond Returns

The U.S. greenback was the second-best performing forex over the previous century, second solely to the Swiss franc. The USA was the biggest financial system on the planet all through this era, and the greenback rose to grow to be the world reserve forex throughout this time. And but, holding U.S. authorities bonds throughout their time of ascent and dominance underperformed merely holding gold.

Professor Aswath Damodaran maintains records of the efficiency of varied belongings lessons going again to 1928. If you happen to had invested $100 in T-bills (BIL) beginning in 1928 and compounded them via 2023, you’d have $2,249 by the top of 2023. If you happen to had taken extra volatility threat and as a substitute invested in longer length T-bonds (IEF), you’d have turned $100 into $7,278.

That appears nice at first, aside from the truth that that is solely as a result of greenback debasement alongside the best way. If you happen to had merely put $100 into gold (GLD), you’d have turned $100 into $10,042. The variety of {dollars} within the U.S. broad cash provide elevated by greater than 400x from 1928 via 2023.

And gold holders had been steadily diluted too. That is why they solely had a 100x nominal acquire slightly than a 400x nominal acquire which might be in keeping with the cash provide development. Yearly, the worldwide provide of refined gold will increase by an estimated 1% to 2%, which steadily impacts a gold holder’s buying energy. If the provision of refined gold grows by a median of 1.5% per yr, then after 95 years the quantity of refined gold in the marketplace could have elevated by about 4x.

And the maths checks out; every unit of gold elevated in greenback worth by about 100x, and there is about 4x as a lot of it, and so the market capitalization of gold elevated by about 400x which is in keeping with the cash provide development.

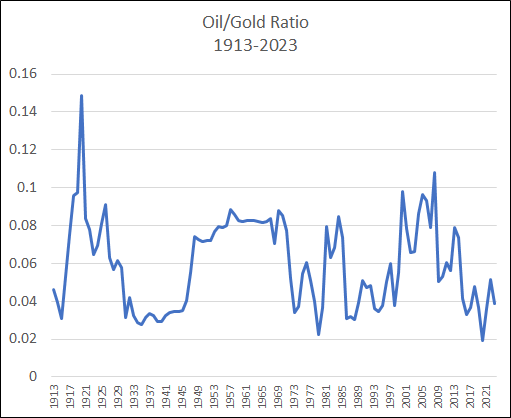

Because of this gradual dilution, over the lengthy arc of time a gold holder’s capability to buy issues like a barrel of oil has been just about flat, whilst our capability to get oil out of the bottom turns into higher as a result of bettering expertise. Here is the chart of the value of barrels of oil denominated in ounces of gold:

Lyn Alden, oil worth knowledge from EIA

A gold holder’s buying energy steadily will increase for issues that we get exponentially higher at making. A gold coin should buy extra agricultural merchandise right now than it may a century in the past, and extra electronics, and extra footwear.

But it surely’s not as a result of gold appreciated, and certainly gold was steadily diluted. It is simply that gold was diluted at a barely slower fee than human expertise/productiveness elevated in combination, and so a gold holder maintained or steadily elevated her buying energy over time in observe. And she or he beat authorities bonds denominated on the planet reserve forex, not to mention each different forex.

Historic Inventory Returns

A number of research through the years have proven {that a} tiny share of equities make up just about all returns in fairness markets.

Professor Hendrik Bessembinder compiled among the most complete datasets on this phenomenon.

For his U.S. study, he discovered that amongst 26,000 recognized shares between 1926 and 2019, greater than half did not outperform T-bills. However the actuality is even worse than that. Simply 4% of all shares accounted for mainly all inventory market returns in extra of T-bills; the opposite 96% of shares collectively matched T-bills as a gaggle. And simply 86 shares accounted for half of all extra returns.

In different phrases, nearly all of U.S. shares traditionally underperformed T-bills, after which one other large minority of shares generated solely minor extra returns over T-bills, after which a really small sliver of huge outperformers represented almost all inventory market extra returns over T-bills. And because the earlier part confirmed, T-bills underperformed gold. And so, the overwhelming majority of shares did not outperform the buying energy of a bit of yellow metallic.

And that is for the USA, which had the best-performing shares of the previous century. For non-U.S. equities, the numbers are even worse. For his global study, Bessembinder studied 64,000 shares from the world over over a three-decade interval and located an unbelievable focus of returns:

We research long-run shareholder outcomes for over 64,000 international widespread shares in the course of the January 1990 to December 2020 interval. We doc that almost all, 55.2% of U.S. shares and 57.4% of non-U.S. shares, underperform one-month U.S. Treasury payments when it comes to compound returns over the complete pattern. Specializing in combination shareholder outcomes, we discover that the top-performing 2.4% of companies account for the entire $US 75.7 trillion in web international inventory market wealth creation from 1990 to December 2020. Exterior the US, 1.41% of companies account for the $US 30.7 trillion in web wealth creation.

U.S. shares as a gaggle had been among the many absolute best investments. Investing within the prime 500 U.S. corporations (SPY), and rotating them as essential to keep up these prime 500 as they be part of and depart that group over time, would have turned $100 in 1928 to over $787,000 via 2023 in line with Professor Damodaran’s knowledge. However as beforehand proven, that is as a result of a tiny share of them created monumental worth whereas the bulk did not sustain with gold.

The worldwide outcomes had been much less stellar. And if Bessembinder had been in a position to run his worldwide numbers for the longer 1926-2019 interval then they’d have been even worse. A lot of inventory markets had been fully nullified of their entirety at one level or one other, as a result of outbreak of conflict or a shift towards communism. Even the inventory markets that made it via the previous century intact usually underperformed the U.S. inventory market.

Historic Actual Property Returns

Actual property has lengthy been referred to as a great long-term funding. However is it?

Professor Aswath Damodaran’s information present that $100 invested into U.S. actual property in 1928 would have became $5,360 by 2023. That is higher than T-bills, however worse than T-bonds and worse than gold. If an investor levered it up they’d have achieved a lot better, however we’ll get to that matter later.

To double-check this knowledge, we will verify Professor Robert Shiller’s dataset on actual property that goes again to 1890. His knowledge exhibits that the nominal house worth index elevated by 88x from 1890 to the current. In the meantime, the value of a unit of gold elevated by 123x throughout that interval. If the house owner/landowner paid a small upkeep fee annually, in addition to a recurring property tax annually, then the hole between these two numbers would have been even wider.

In fact, some actual property has carried out very properly. If somebody purchased Manhattan land on the flip of the twentieth century, or land in Silicon Valley in the beginning of the enterprise period, these bets actually paid off. These had been prime percentile actual property performances.

However in distinction, vital quantities of actual property goes to zero if town they’re close to decreases in inhabitants and financial exercise. For instance, there are deserted properties throughout Detroit. These are giant once-expensive properties that at the moment are rotting on parcels of land that no person needs. And actual property cannot be moved if the financial scenario or political scenario in a area turns into untenable.

Most actual property falls someplace between these extremes. It performs decently, particularly when contemplating that it may change the proprietor’s rental earnings or be rented out for cashflows, however after upkeep and taxes are thought-about, its unlevered whole return from worth appreciation and cashflow technology web of upkeep leaves one thing to be desired relative to gold.

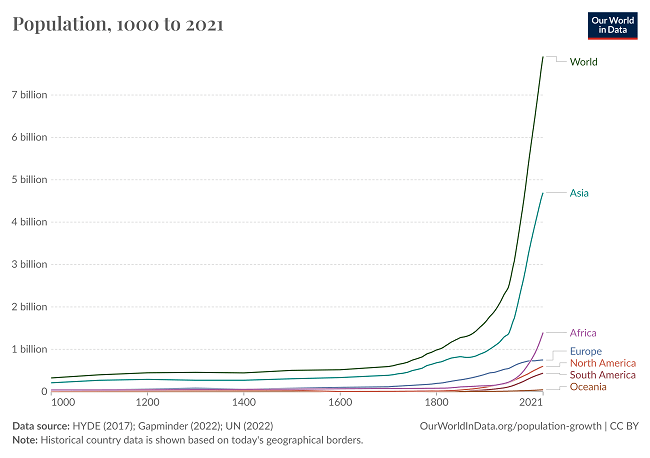

And this mediocre efficiency in unlevered actual property occurred regardless of the huge inhabitants improve that occurred in the course of the nineteenth and twentieth centuries.

Our World in Knowledge

Though rural and suburban residential land is slightly ample, if somebody purchased land in a great neighborhood close to a metropolis that grew considerably, their funding probably did properly. However as inhabitants development cools off, so do actual property costs. In Japan, there are millions of abandoned countryside homes which might be almost free. Lots of them are in stunning and secure rural areas, and but there’s inadequate demand for them. They’ve various states of high quality, however in combination they’re now deteriorating as a result of abandonment.

Placing this all collectively, actually all authorities bonds have underperformed gold over the long term, and most unlevered actual property has underperformed gold as properly. Shares as an asset class drastically outperform gold, however solely as a result of the highest 4% of them within the best-performing market do all of the heavy lifting whereas the opposite 96% as a gaggle do not generate any extra returns.

Proprietor-Operators are the Winners

The numbers proven within the prior part are slightly disastrous at face worth; the overwhelming majority of investments underperform gold. Does that imply they should not have been made within the first place?

The reply, particularly for shares and actual property, is that loads of these investments really made sense to do. However not essentially for outdoors passive traders.

An enormous expense for corporations consists of salaries for staff. This contains salaries for the founders and executives as properly. And a younger firm is usually owned by the founder/president.

If a fairly profitable firm goes via its whole lifecycle from beginning to dying and fails to outperform T-bills or gold, it would not normally imply that the corporate should not have existed in any respect. Alongside the best way, it sustained salaries and work for many individuals, together with the founders and executives and salaried staff. It offered merchandise and/or providers to prospects, which improved general human productiveness and high quality of life.

These companies had been usually nice for owner-operators and staff, and for patrons, however not for outdoors passive traders.

Being an owner-operator of a enterprise, or a employee at a enterprise, makes loads of sense. Nevertheless, the overwhelming majority of companies will not be sturdy sufficient to offer good returns for out of doors passive traders in spite of everything bills (together with salaries) are thought-about.

Good returns for out of doors passive traders are reserved for under the finest forms of corporations; corporations which might be so dominant and high-margin that even after paying all of their executives and staff, they’ve loads of extra income for out of doors passive traders. Though shares from any sector can have these traits, Bessembinder’s analysis discovered that main outperformers had been disproportionally concentrated within the expertise, telecommunications, power, and healthcare/pharmaceutical sectors. They’re on the appropriate facet of an rising tech development, they’ve community results, they’ve economies of scale, they’ve protected intangible property corresponding to patents, or they’re a part of an oligopoly, and so forth.

Actual property usually rewards owner-operators as properly. As an actual property investor that owns cashflow-producing properties, the extra work that you simply outsource, particularly if the property is unlevered, the much less probably there’s to be extra income for you above the speed of simply holding gold. Unlevered cap charges of cashflow-producing properties are typically fairly low. Nevertheless, somebody who takes time to check totally different property markets, make investments into choose properties utilizing leverage, construct them or repair them up and selectively rent or contract folks to assist him, after which re-sell the properties or lease them out, can earn a great residing from that exercise. It is his time and a focus that’s including worth and producing returns.

So the primary reply to the query of why most companies or actual property investments present weak returns and but nonetheless make sense to exist, is that you need to take a look at them from the angle of owner-operators and staff (i.e. the within energetic individuals), not for out of doors passive traders. And the second reply has to do with leverage.

Turning Mediocrity into Wealth by way of Leverage

Traditionally, a key option to flip mediocre investments into good investments has been to use leverage. That is not a suggestion; that is a historic evaluation, and it comes with survivorship bias.

When leverage is used outdoors of sure contexts, it normally seems disastrously. A number of well-known traders have well-known quotes about how leverage is not wanted, and but while you take a look at how they function and what they purchase, they usually do use leverage. In lots of instances, leverage is constructed into an funding itself, or held via a number of layers.

If you use leverage to personal an funding (corresponding to a enterprise or some actual property), you are borrowing (i.e. shorting) the ample fiat forex and utilizing it to purchase issues which have some extent of shortage to them relative to that forex (corresponding to first rate companies and properties).

When leverage improves a mediocre funding for out of doors passive traders, what’s actually occurring is that their fiat forex brief is an effective funding. And since leverage is harmful, there are solely a handful of how to deploy giant quantities of leverage safely. The mediocre funding on this context primarily serves as an honest platform for traders to connect a fiat forex brief to, after which arbitrage a revenue out of that distinction.

Debt and Bonds

Giant quantities of bonds are purchased by banks or different levered entities. They borrow from depositors at a low rate of interest for his or her legal responsibility facet, whereas their asset facet consists of higher-yielding and longer-duration loans and securities, together with authorities bonds in lots of instances. Banks have traditionally usually been levered round 10-to-1 or extra.

This permits them to earn a excessive return on their capital. They revenue drastically from the unfold between the speed they borrow from depositors at and the speed they lend at or the speed they personal securities at.

Different monetary establishments have interaction in comparable leveraging, the place they use authorities bonds as collateral for loans, or different comparable preparations.

Debt and Actual Property

Actual property is probably the most leverageable asset for many traders. Throughout the context of the fiat forex system, it has been each quantifiably workable and socially acceptable to personal actual property with 5-to-1 and even 10-to-1 leverage. People who find themselves not skilled traders will routinely put 20% down and borrow 80% of the worth of a house, with numerous choices to extend that to 10/90 in some instances, as a result of we arrange our monetary system round this being a standard factor to do.

This happens for a pair causes. One is that actual property on common is much less unstable than equities. A second is that it’s a lot much less liquid; a home will get appraised much less continuously than a inventory does, and there are vital prices of each money and time to purchase or promote a home and to maneuver from one home to a different. Because of these two issues, actual property debt is usually not call-able, that means that so long as she is making funds on time, a mortgage borrower would not get liquidated and grow to be compelled to promote her home if the home worth dips beneath the borrowed quantity, which might be the case for many different forms of leveraged collateral.

After upkeep and recurring taxes, nearly all of unlevered actual property, even when rented out for cashflows, would not outperform gold. However not like gold, 5-to-1 leverage makes actual property really fairly good in lots of contexts, and traditionally permits it to outperform gold. Actual property’s repute as constructing wealth has been well-deserved in observe as a result of this truth. And naturally, the true successful mixture has been to personal the top-decile performing properties and lever them.

Debt and Shares

Giant companies do the identical factor as actual property traders, however at decrease charges of leverage.

If an organization is profitable sufficient to grow to be one of many largest thousand corporations round, they have an inclination to have glorious entry to company bond markets. They’ll borrow giant quantities of cash for many years at low rates of interest, and use that capital to organically develop their enterprise, purchase smaller corporations, or purchase again their very own shares. Both approach, they’re borrowing ample fiat forex at low charges and utilizing that capital to construct or purchase enterprise fairness, and they’re arbitraging that unfold for shareholders.

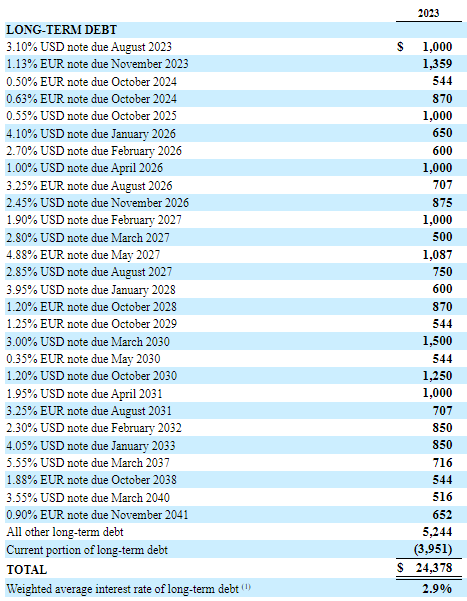

Take into account Procter & Gamble (PG) for instance. The corporate was based in 1837, and has been worthwhile just about yearly for many years straight. And but they’ve over $24 billion in long-term debt. Why? As a result of they’re utilizing that debt for the aim of monetary arbitrage. It is how they enhance fairness returns. They difficulty bonds with durations of ten or twenty years in lots of instances, and traditionally at very low rates of interest which might be almost as little as authorities borrowing charges. They usually use these proceeds to make acquisitions or purchase again their very own shares. As their debt matures, they refinance it into extra debt. They voluntarily hold tens of billions of debt on their books on a everlasting foundation as a result of it is a everlasting fiat forex brief.

Lots of Procter & Gamble’s bonds had been issued when charges had been beneath 1% or 2%. These are long-term fiat forex shorts, they usually had been among the finest investments that the corporate ever made:

Procter and Gamble 2023 10k

You possibly can consider it within the following phrases. In developed markets, the broad cash provide traditionally grows by 6-9% per yr on common. In the USA that determine has been round 7% per yr on common over the long run. If an actual property investor or an organization can borrow at 1% or 3% or 5% charges in that context, then their borrowing fee is lower than the cash provide development fee. The client of these bonds will get diluted over time relative to the expansion of the cash provide, whereas the vendor of these bonds has successfully shorted them, and may deploy the capital into scarcer issues like fairness and property.

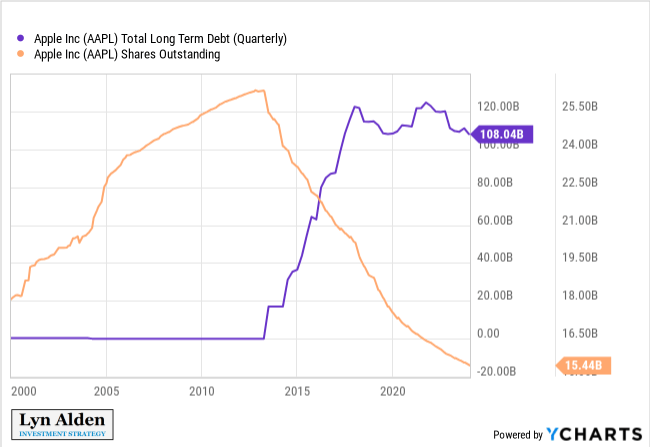

A number of blue-chip corporations do that. They’ve among the many lowest value entry to debt on the planet, and they also use it. Beginning in 2013, Apple (AAPL) started taking out $108 billion in low-interest debt and utilizing it to purchase again their very own shares. They’re probably the most profitable firm in fashionable monetary historical past, and but like everybody else, they started utilizing debt as a strategic a part of their capital construction as a result of they profit from arbitraging the unfold between 1) shorting ample fiat forex and a couple of) shopping for scarcer issues together with their very own fairness.

YCharts

Warren Buffett and his firm Berkshire Hathaway (BRK.B) have taken this a step additional, by arbitraging an insurance coverage float.

Insurance coverage corporations soak up buyer premiums, and pay out buyer claims. In between these two actions, they maintain capital as a “float” they usually usually make investments that float into bonds. An insurance coverage firm is leveraged on this approach, and its borrowing is mainly within the type of a zero-rate mortgage from its buyer premiums. In lots of instances, an insurance coverage firm will break even when it comes to paying out as many declare {dollars} because it takes in {dollars} from premiums, nevertheless it makes a web revenue anyway as a result of holding interest-bearing bonds with that zero-rate float.

Berkshire Hathaway is among the largest insurance coverage corporations on the planet. However Warren Buffett deploys a large share of that float into shares slightly than bonds. And the shares he buys usually use leverage as beforehand described. He owns or has owned large stakes of corporations like Apple, Procter & Gamble, Coca-Cola (KO), Chevron (CVX), Kraft Heinz (KHC), and lots of others. These are blue chip corporations that purposely use loads of low-rate company debt regardless of being persistently worthwhile corporations. He additionally has traditionally invested in loads of banks, which make use of leverage much more. After which Berkshire as an organization additionally points long-term low-rate bonds, along with having leverage from its insurance coverage float.

So Berkshire Hathaway is an enormous leveraged insurance coverage firm that borrows some huge cash at low charges and deploys that capital into corporations who’re additionally leveraged at low charges. For the complete stack, there are a number of layers of low rate of interest borrowings constructed on prime of each other, and that capital is redeployed into scarcer enterprise fairness and property. That unfold, throughout all these layers, creates large wealth for folks utilizing this technique relative to those that are lengthy currencies and bonds. Buffett makes positive to concentrate on low-volatility long-term compounding shares with financial moats to deploy this technique on, which retains the chance in verify.

Berkshire has additionally made a behavior out of shopping for small and medium sized personal companies in full. Many of those smaller corporations would have larger borrowing prices in the event that they had been unbiased. However Berkshire should buy loads of them, after which difficulty company debt on the mum or dad firm degree at a lot decrease rates of interest than any of them may difficulty on their very own. So he should buy loads of unlevered cashflow-producing small or medium-sized companies, and switch them right into a portfolio of companies which might be levered with Berkshire’s very low value of capital.

This has been extremely efficient, as a result of the bigger it has grow to be, the decrease the price of capital has grow to be. Buffett understood this properly from the beginning, and reached essential mass with this technique.

A number of Berkshire’s wholly-owned companies and inventory positions can be considerably unremarkable in the event that they had been unlevered. However first rate enterprise operations, if their cashflows are steady sufficient, make glorious platforms to connect fiat forex shorts to. And a mediocre however dependable enterprise with a long-term low-cost fiat forex brief hooked up to it, has been a wonderful funding.

Even inside the previous few years, Berkshire borrowed loads of yen at ultra-low charges, and used it to purchase the Sogo shosha Japanese shares, which have loads of laborious belongings and constructive cashflows (and which have their very own yen-denominated company debt as properly). It was a wonderful transfer; Buffett’s firm benefited each from first rate operations by the Sogo shosha shares themselves, in addition to the unfold between them and the quickly devaluing yen brief that was used to purchase them.

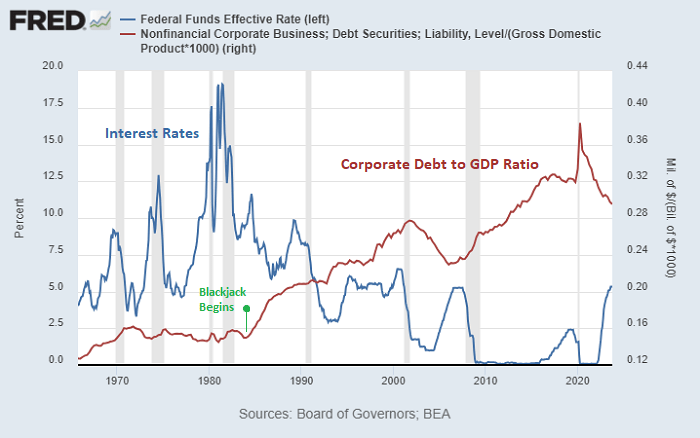

A Sport of Monetary Blackjack

Within the card recreation of Blackjack, the objective is to get as near 21 as attainable along with your playing cards, however with out going over 21. If you happen to go over, you mechanically lose.

Over the previous 4 many years specifically, the worldwide monetary system has rewarded gamers of monetary Blackjack. Entities that borrow cash and use it to purchase scarce belongings, however in a prudent sufficient approach that they aren’t among the many first wave to explode in a recession, have been the winners. You need leverage, however you do not wish to “go over”.

This has been a key contributor to rising wealth divide amongst people, and a key contributor to the efficiency hole between giant and small corporations. Bigger and wealthier entities, as they develop bigger and wealthier, get even higher entry to low value capital, which provides them much more of a bonus. It is a virtuous cycle for some time. Bigger entities have entry to decrease prices of capital on a tough cash system to some extent, however ever-devaluing fiat forex is a supercharger for this development as a result of the arbitrage from having good entry to credit score is approach greater than it’s with a tough cash system.

Throughout the present monetary system, those that don’t use leverage usually lose. Those that leverage an excessive amount of or too unskillfully and “go over” additionally lose. However those that leverage reasonably and elegantly have been the winners. They get pleasure from a multi-trillion-dollar annual arbitrage by shorting ample fiat forex for lengthy durations at low rates of interest and utilizing it to purchase scarcer enterprise fairness or properties.

If you happen to do not play the sport as an investor, you normally lose as a result of leverage drives up the valuations on your potential investments. A key motive why cap charges on actual property are so low, is that so many individuals purchase them with leverage. If there was no vital leverage accessible for them, then unlevered cap charges would should be larger to incentivize the funding, however with the existence of many individuals utilizing leverage for them, it drives down the cap charges and makes them into usually low-returning investments for anybody wanting to personal cashflow-producing properties unlevered.

And since it is a international recreation, the gamers have an enormous gameboard to make use of this technique on. If one forex turns into too laborious for this technique to work, they’ll make use of jurisdictional arbitrage and deploy their capital elsewhere. There are roughly 160 fiat currencies on the market. Dozens of them have first rate liquidity and capital markets. Funding companies can borrow (go brief) the yen and purchase (go lengthy) Brazilian belongings. They’ll borrow (go brief) the euro and purchase (go lengthy) American belongings. The permutations of this technique have been very ample for many years.

I say “they” however after all I embrace myself right here as properly. I borrow American {dollars} or Egyptian kilos for multi-year durations at low charges and deploy it into scarcer property. I personal equities that borrow for lengthy durations at low charges and deploy it into scarcer enterprise fairness. I profit, each straight and not directly, from the unfold between shorting ample fiat forex and longing scarcer property and enterprise fairness. This has been the successful technique.

The Altering Sport Guidelines

The properties of the fiat forex system have incentivized debt accumulation and the enjoying of this international recreation of monetary Blackjack.

4 many years of falling rates of interest have been an enormous tailwind for this technique, since money owed may regularly be refinanced at ever-lower charges, and more and more at charges which might be very low relative to the speed of cash provide development. Moreover, giant numbers of open capital markets in an more and more related world have made it attainable to arbitrage between jurisdictions as properly.

St. Louis Fed

Now, after rates of interest bounced off zero in developed markets and will begin going structurally sideways as a substitute of structurally down, the effectiveness of that technique is prone to diminish.

And as governments world wide more and more have excessive debt at their sovereign degree, they grow to be more and more incapable of sustaining excessive constructive actual yields for lengthy intervals of time, which makes it more durable for them to convincingly combat inflation. International locations that face acute fiscal points usually flip to capital controls, which impairs the sport of worldwide monetary Blackjack. It occurred on a regular basis in developed international locations from the Thirties into the Nineteen Seventies, and nonetheless occurs on a regular basis extra lately in numerous rising markets.

Excessive public debt usually produces the drama of default and restructuring. However debt can also be lowered via monetary repression, a tax on bondholders and savers by way of damaging or below-market actual rates of interest. After WWII, capital controls and regulatory restrictions created a captive viewers for presidency debt, limiting tax-base erosion. Monetary repression is most profitable in liquidating debt when accompanied by inflation. For the superior economies, actual rates of interest had been damaging ½ of the time throughout 1945–1980. Common annual curiosity expense financial savings for a 12—nation pattern vary from about 1 to five % of GDP for the complete 1945–1980 interval. We advise that, as soon as once more, monetary repression could also be a part of the toolkit deployed to deal with the newest surge in public debt in superior economies.

–The Liquidation of Government Debt, IMF Working Paper 2015/007

Geopolitical conflicts are prone to additional add boundaries between the free motion of capital. Whether or not it is kinetic wars or commerce wars or monetary wars, as giant teams of nations more and more have tensions between one another when it comes to strategic pursuits and run into their very own fiscal dominance points, the frictions on international capital motion have a excessive probability of accelerating.

So, the effectiveness of this international monetary Blackjack technique is probably going going to decrease, though entities that already locked their debt in for lengthy durations are probably able to experience the momentum for fairly some time longer.

The forms of investments that labored properly in the course of the previous 4 many years are much less prone to work fairly as properly over the subsequent 4 many years. The virtuous cycle of ever-lower rates of interest, ever-higher personal debt ranges, and ever-higher fairness valuations, is probably going getting previous its prime, and is susceptible to rolling over right into a vicious cycle within the different route.

And in that shifting surroundings, it is necessary to keep in mind that most investments are unhealthy. The vast majority of unlevered companies will not be sturdy sufficient to supply returns for passive traders that outperform T-bills or gold. The vast majority of unlevered actual property properties, after upkeep and operation and taxes are thought-about, additionally fail to outperform primary belongings like gold.

So in that surroundings, from the angle of a passive outdoors investor trying to deploy capital, it is necessary to both search out the companies which have sturdy aggressive benefits (community results, highly effective manufacturers, intangible property, economies of scale, oligopoly participation, and so forth), or to be very delicate to valuations when shopping for mediocre corporations.

The prior 4 many years are unlikely to be a great dataset for back-testing and forming methods that may work for subsequent 4 many years, as a result of the situations will probably be fairly totally different.

For fairness and actual property traders, the important thing takeaways from this piece are 1) don’t extrapolate the prior many years for a given funding and as a substitute assess it with this context in thoughts, 2) attempt to emphasize the sectors that Bessembinder recognized as ones that disproportionally generate extra returns, and three) search for corporations which have locked in or are in any other case nonetheless in a position to play this arbitrage recreation going ahead in a tougher surroundings for it.

Moreover, laborious monies grow to be a critical different as soon as once more on this context, and are value critical consideration for a portfolio slice, as a result of the hurdle fee for shares to outperform them is excessive when there will not be loads of tailwinds on the backs of shares.

{kind=link}