Sewcream

“Industrial actual property is crashing!”

That’s the sentiment we hear time and again. It is the message the market appears to be sending by discounting all actual property funding trusts (“REITs”) throughout the assorted sectors of economic actual property. The idea is that rates of interest of 5%+ have destroyed the enterprise mannequin of REITs, which should pay out 90%+ of their taxable revenue and are due to this fact reliant on the fairness and debt markets for funding. And this surge in rates of interest is exacerbating a perceived plunge in demand for CRE amid a weakening economic system.

These sentiments are simply plain incorrect.

As I defined in “Blue-Chip Real Estate Is A Bargain – Top Picks Across 5 Sectors,” business actual property ≠ workplace buildings. Though there are positively some extreme issues in sure corners of workplace actual property, business actual property extra broadly continues to thrive.

Do not take it from me. Let’s hear from some specialists.

In a latest CNBC interview, CEO of CBRE & Associates (CBRE) Bob Sulentic defined:

I feel a few of the speak of doom and gloom is out forward of what is actually occurring. Workplace area has bought a tricky circumstance, partly due to return to the workplace challenges after COVID, partly, due to jobs being eradicated in tech and others. However in case you take a look at industrial area, very sturdy fundamentals, 3.5% emptiness. For those who take a look at institutional high quality multifamily, lower than 5% emptiness. Inns, very sturdy fundamentals. Single-family [rentals] backed by institutional high quality financing, very sturdy fundamentals. Even retail fundamentals are bettering, rental charges are going up. So the story round business actual property is not fairly what folks suppose.

And this is a press release from Bridgewater Associates (h/t Baron Real Estate Fund Q1 letter), the biggest hedge fund on the planet, from the tip of March:

We do not suppose business actual property is a scientific threat, largely as a result of the sector lacks the issues that existed in (principally residential) actual property within the late 2000s: unhealthy lending requirements, plenty of leverage, and a provide glut following a building increase. CRE is a extremely various sector that features one troubled sub-sector in workplaces (about 15% of the market), but additionally residences, hospitals, warehouses, information facilities, nursing houses, retail, and extra. Industrial building exercise can also be fairly subdued relative to the early Nineteen Nineties, when a CRE bust led to a wave of losses. Whereas there are strains at some regional banks, the higher underwriting practices and the run-up in costs during the last decade will mute the loss cycle.

Be aware of that final level: CRE building is muted, largely due to the diploma to which building prices have soared in the previous couple of years. Pricing in CRE, like all different markets, is decided by provide and demand. And although demand stays sturdy and rising (even when slower than the previous couple of years), provide is just rising at a crawling tempo.

Based on Inexperienced Avenue Advisors (courtesy of Baron Actual Property):

[E]xpectations for business actual property building (annual building completions as a % of current stock) from 2023 to 2026 are anticipated to be only one.5% for residences, 1.0% for wi-fi towers and lodges, 0.8% for workplace buildings, 0.3% for buying facilities, and 0.1% for retail malls.

Likewise, in response to Inexperienced Avenue, CRE occupancy ranges are favorable at present in comparison with the interval throughout the Nice Monetary Disaster. Three examples:

- Industrial: 96% at present vs. 88% in 2009

- Self-storage: 94% at present vs. 81% in 2009

- Manufactured housing: 97% at present vs. 87% in 2009

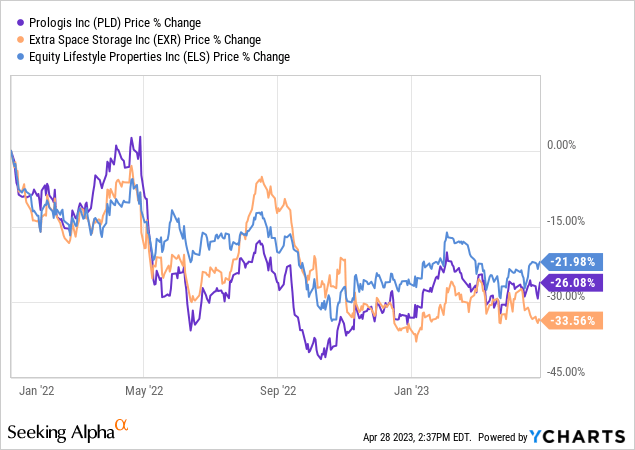

This doesn’t sound just like the method for a CRE meltdown, and but world-class REITs like the economic big Prologis (PLD), self-storage chief Further Area Storage (EXR), and manufactured housing landlord Fairness LifeStyle Properties (ELS) have shed 22-34% of their market worth because the starting of 2022:

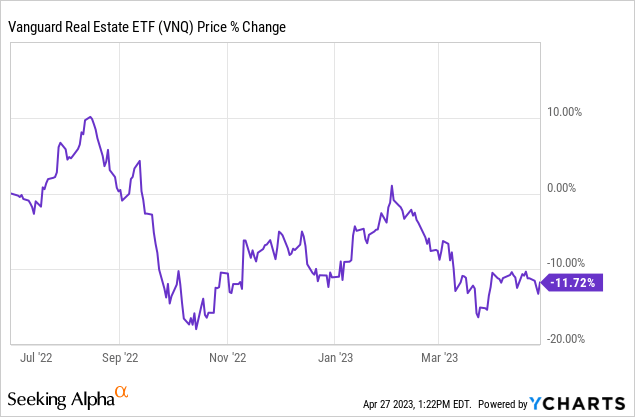

These are usually not cherry-picked instances. The Vanguard Actual Property ETF (VNQ) has misplaced 28.5% of its market worth because the starting of 2022, as of this writing.

This is the reason Jon Grey, President of Blackstone, said in Blackstone’s (BX) Q2 2022 conference call in reference to non-public versus public CRE:

The most effective alternatives at present are clearly within the public markets on the display screen and that is the place we’re spending a number of time.

And REITs have shed one other ~12% of their market worth since Grey made this assertion!

If the biggest actual estate-focused asset supervisor within the nation noticed REITs as an important worth in mid-2022, how way more are they good values at present?

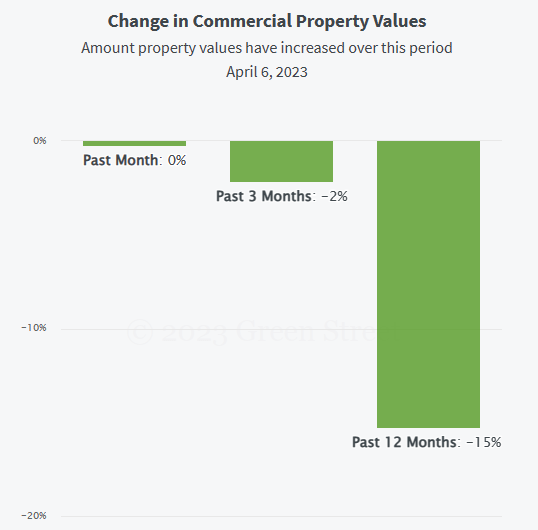

Now, admittedly, CRE property values have fallen about 15% during the last yr, in response to Inexperienced Avenue:

Inexperienced Avenue Advisors

As credit score circumstances have tightened, the movement of capital into CRE has drastically pulled again, which has led to a softening in CRE property costs.

However these drops in property costs are usually not unfold evenly throughout all sectors of CRE. They’re overwhelmingly concentrated in a single specific sector: workplace.

Take into account these factors:

- Declines in property values don’t essentially translate into declines in lease charges or internet working revenue.

- Most banks are well-capitalized, and most types of CRE are performing very effectively.

- Nearly all sectors of CRE are not overbuilt or oversupplied. The one exception is workplace.

- A lot of the misery in CRE is confined to decrease high quality (Class B and C) workplace properties, which have comparatively excessive emptiness charges.

- A tightening of credit score circumstances and lending requirements ought to primarily have an effect on these lower-quality workplace properties.

- For instance, for Q1 2023, Class A NYC workplace landlord S.L. Inexperienced (SLG) reported occupancy nonetheless above 90%, and so they secured a $500 million refinancing at 250 foundation factors above SOFR, swapped to a hard and fast price of 6.11% for 3 years.

- Most banks, together with most regional banks, should not have ample publicity to Class B and C workplaces to make a systemic meltdown possible.

- Some extremely leveraged non-public and public CRE entities, no matter their specific actual property, might nonetheless blow up as a result of tightened credit score circumstances. However these are particular instances.

Once more, although, do not take it from me. Let’s take a fast tour by means of the Q1 2023 outcomes of some main REITs throughout varied sectors to examine the heartbeat of CRE proper now.

REIT Q1 Earnings Updates

Alexandria Actual Property Equities (ARE)

ARE, proprietor and developer of Class A life science services within the nation’s finest positioned and best biotech clusters, put up Q1 outcomes that absolutely defy the ~33% drop in inventory value it has suffered during the last yr.

AFFO per share rose 6.8% on the again of the very best quarterly straight-line lease progress in firm historical past at 48.3%. Money lease progress additionally got here in sturdy at 24.2%, whereas money same-property NOI progress hit 9.0%. In the meantime, regardless of the market’s worry that ARE’s smaller biotech tenants may need suffered from the collapse of Silicon Valley Financial institution, ARE collected 99.9% of contractual lease in Q1 and 99.7% thus far in April.

With whole liquidity of $5.3 billion plus free money movement after dividends of $375 million (AFFO payout ratio of 55%), ARE has loads of capital accessible to speculate opportunistically this yr.

As an indication of how ARE’s Class A life science properties have retained their worth, the REIT bought a minority curiosity in certainly one of its properties for a cap price of 5.4% throughout Q1. It would not sound to me like there’s a “crash” in life science property costs.

Mid-America Residence Communities (MAA)

Sunbelt multifamily trade chief MAA reported sturdy outcomes for Q1, even when progress has cooled off from final yr on account of plateauing financial progress and elevated provide coming on-line in its markets.

Even so, AFFO per share surged 15.7% within the quarter on the again of a 95.5% occupancy price and 12.5% same-property NOI progress.

In the meantime, with $1.4 billion in liquidity on prime of an underleveraged stability sheet (A- credit standing) of 28% debt to belongings and a 3.5x internet debt to EBITDA ratio, MAA’s capitalization seems pristine. On the Q1 conference call, administration made clear their intentions to pounce on any enticing acquisition alternatives which will come up later this yr from multifamily house owners who weren’t as prudent with their debt as MAA.

Whereas multifamily property costs are coming down, the scenario is way from a “crash.”

Camden Property Belief (CPT)

CPT’s Sunbelt-focused multifamily portfolio is top-notch in its areas in addition to its diversification throughout city/suburban areas and high-rise/mid-rise/garden-style residences.

Regardless of new provide coming on-line and condominium demand cooling off, CPT nonetheless achieved blended (new and renewal) leasing spreads of 4.0% within the first quarter and 4.2% thus far in April. Identical-property NOI progress got here in at 8.1% YoY within the quarter, and the REIT expects SPNOI to common 5% for the yr. In the meantime, occupancy has remained regular, dipping solely barely from This autumn 2022’s 95.8% to Q1 2023’s 95.3%.

CPT has six properties below growth proper now, together with its first single-family rental neighborhood within the Woodlands, Texas, to be delivered within the coming years.

Though provide deliveries needs to be notably excessive within the Sunbelt multifamily area within the subsequent few years, these markets additionally take pleasure in long-term demographic benefits comparable to above-average job and inhabitants progress on account of decrease prices of dwelling and business-friendly regulatory environments.

W. P. Carey (WPC)

WPC is the 2nd largest internet lease REIT behind Realty Revenue (O) at an enterprise worth of about $23 billion and with a property portfolio of 1,446 properties spanning three continents (primarily North America and Europe).

WPC’s AFFO per share of $1.31 within the first quarter was admittedly flat YoY, however that is primarily as a result of lack of administration payment revenue from absorbing its final non-public fund final yr in addition to larger curiosity bills.

The REIT has secured over $740 million in actual property investments year-to-date, as WPC’s goal tenants are discovering sale-leasebacks to be a extra enticing type of financing than debt. This yr, administration expects to see whole funding quantity between $1.75 billion and $2.25 billion whereas disposing of solely $300-400 million of properties.

Between ahead fairness locked in at a better inventory value than at present’s and the power to challenge attractively priced debt such because the latest €500 million term loan swapped to a hard and fast price of 4.34%, WPC is well-prepared to attain its spectacular 2023 funding quantity steering.

What’s extra, WPC’s attribute CPI-based lease escalations ought to make sure the portfolio’s same-store lease escalations common round 4% in 2023 and over 3% in 2024. It is uncommon to see a internet lease REIT take pleasure in this degree of natural lease progress.

Rexford Industrial Realty (REXR)

REXR completely owns high-quality industrial properties positioned within the extraordinarily supply-constrained Southern California market, the place administration calls the economic provide scarcity “nearly uncurable.”

Core FFO per share elevated 8.3% (decrease than the 34% whole FFO progress as a result of firm’s use of its peer-leading price of fairness by way of inventory issuance), whereas same-property NOI progress rose 7.3% YoY.

Essentially the most unbelievable metrics are from lease-over-lease lease progress. In Q1, REXR’s new and renewal leases on comparable areas generated 80% straight-line lease progress and 60% money lease progress. You learn that accurately. Occupancy stood at 98% throughout the quarter. And on prime of that unbelievable natural progress, REXR additionally acquired $804 million of recent properties in Q1.

And REXR joins asset high quality with stability sheet high quality: a BBB+ credit standing, internet debt to enterprise worth of 13.6%, and 0 floating rate of interest publicity.

Prologis (PLD)

You may accuse me of cherry-picking the very best industrial REIT with REXR, so let’s additionally take a look at the most important participant within the public REIT area: PLD.

PLD scored 12% core FFO per share progress in Q1, as its portfolio occupancy stood at 98% and generated an all-time excessive same-property money NOI progress of 11.4%. Talking of all-time highs, PLD’s internet efficient straight-line lease progress of 69% and money lease progress of 42% on new and renewal leases additionally reached all-time excessive ranges.

In the meantime, PLD’s stability sheet can also be very good, with debt to enterprise worth of19.1%, a weighted common rate of interest on debt of two.6%, and only a few debt maturities till 2026.

Crown Citadel (CCI)

As I defined extra totally in “Crown Castle: Take Advantage of the Market’s Short-Termism,” CCI is struggling proper not from a crash within the worth of its cell towers or fiber strains however relatively (1) larger rates of interest and (2) the cancellation of some Dash leases after its acquisition by T-Cellular (TMUS). However each of those headwinds are momentary.

Nearly everybody available in the market expects the Federal Reserve to start reducing rates of interest by someday subsequent yr, which ought to ease stress on CCI on the curiosity expense facet. And given the oligopoly that now exists among the many three main wi-fi carriers, additional consolidation seems extremely unlikely on this trade. As such, extra lease cancellations don’t seem possible.

In the meantime, even amid these headwinds, Q1 AFFO per share rose 3.4% YoY, and CCI’s stability sheet stays sturdy with its BBB/BBB+ credit score rankings and internet debt to EBITDA of 5.0x.

Backside Line

Is business actual property crashing? No, I do not suppose so.

However REIT inventory costs are a special story. They’ve certainly crashed, even whereas their fundamentals stay sturdy. That is the setup for some unbelievable, generationally good shopping for alternatives.

My dividend progress portfolio is already chubby REITs, and I’m glad to make it incrementally extra chubby as a result of, as Warren Buffett as soon as stated, “Diversification makes little or no sense for anybody who is aware of what they’re doing.”

{kind=link}