luza studios

Thesis

Nintendo (OTCPK:NTDOY) has two of the highest three best-selling recreation franchises of all time in its portfolio and lots of extra within the prime 50. In actual fact, I feel it’s honest to say that they most likely have the very best portfolio of any video games firm, which is an unbelievable aggressive benefit.

But they’re priced like a really fundamental firm, regardless that they’re a really top quality enterprise. I feel a part of that’s as a result of means enterprise is completed in Japan and the truth that lots of traders do not imagine in Nintendo for the time being.

However for my part, given the long run development alternatives and the issues which can be at the moment priced into the share value, this firm is undervalued and has big potential to ship market-beating returns for long-term shareholders.

Evaluation

Searching for Alpha Charting Tab

EV / EBIT, which I feel is an excellent indicator of whether or not an organization is reasonable or not, we are able to see that Nintendo is buying and selling near its 5-year low and at a a number of of 8.79x. That is positively low-cost, as usually firms with a a number of under 12-13x are within the investable class for many worth traders, and Nintendo’s a number of is nearly 40% decrease.

And such a low a number of might be justified for a struggling firm with little or no development forward, however in my view this doesn’t apply to Nintendo. They’ve a unbelievable catalogue of franchises like Mario, Zelda and Pokémon, plus their console enterprise, the place the Change has offered 107 million models and is the third best-selling console of all time.

The one argument for the time being might be that they have not introduced a brand new technology of consoles, however there are sufficient rumors and hints that the Change 2 will likely be obtainable within the close to future.

Searching for Alpha Charting Tab

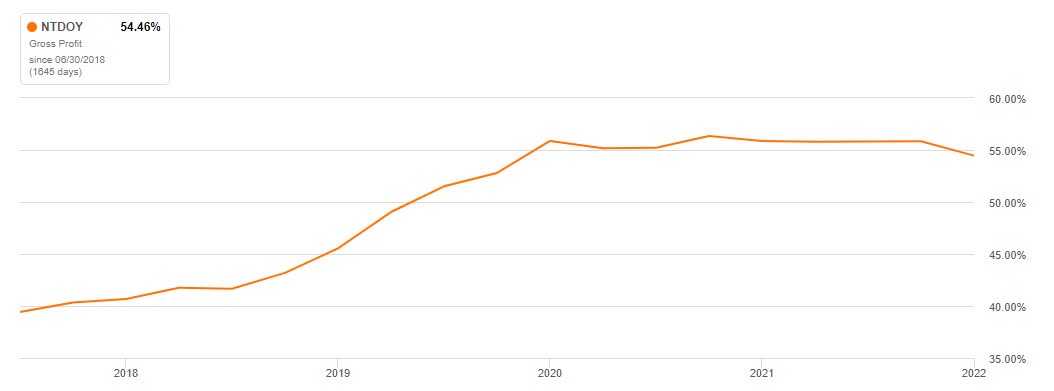

If we take a look at the gross revenue margins, we see a robust enchancment from 40% to 55% over a 5 yr interval, which clearly exhibits that they’ve made progress, and so they have completed so whereas growing gross sales over the identical interval.

Searching for Alpha Charting Tab

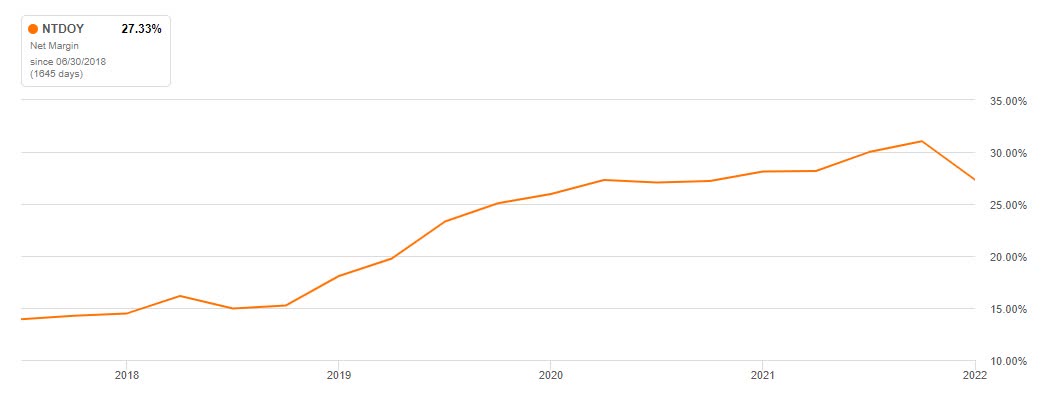

Web revenue margins paint the identical image. A powerful enchancment over the past 5 years to a extremely sturdy web revenue margin of 27.33%. Nintendo is clearly a greater firm than it was 5 years in the past. And the web revenue margin is actually sturdy throughout the board.

Searching for Alpha Charting Tab

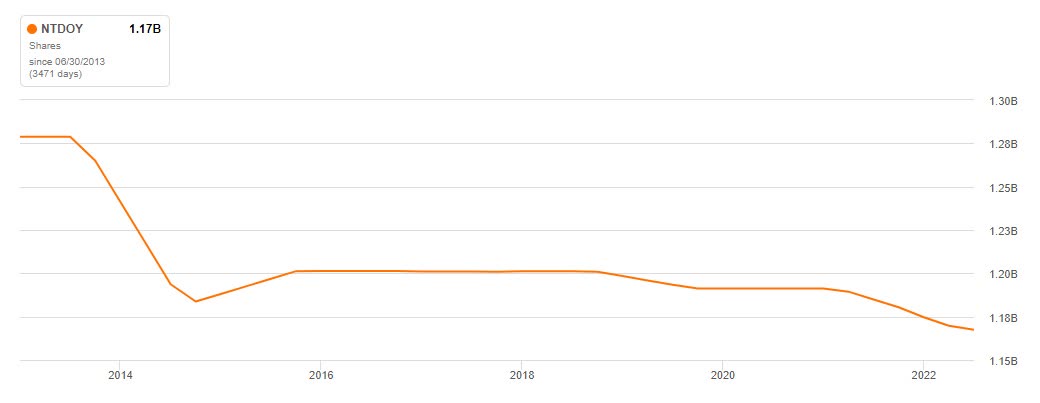

Present shareholders additionally needn’t worry dilution as the corporate has diminished its excellent shares by practically 100 million over the previous 10 years. However Nintendo shouldn’t be a inventory cannibal, so most future returns will come from dividends + enhancing enterprise metrics or multiples.

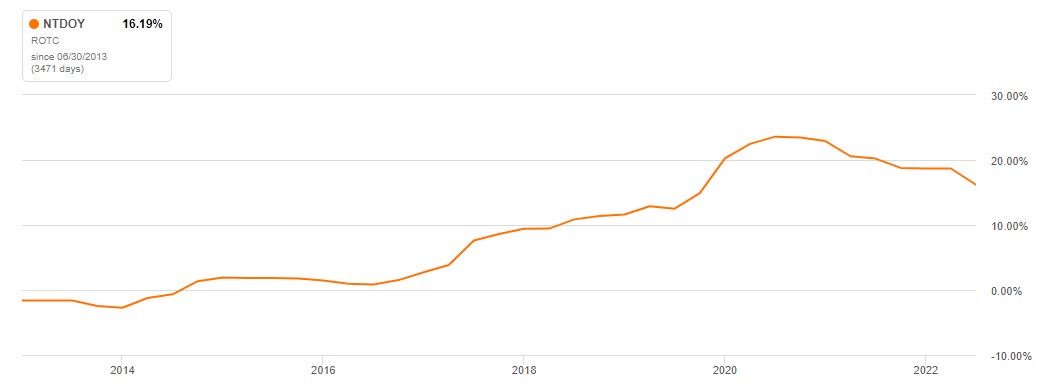

Searching for Alpha Charting Tab Searching for Alpha Charting Tab

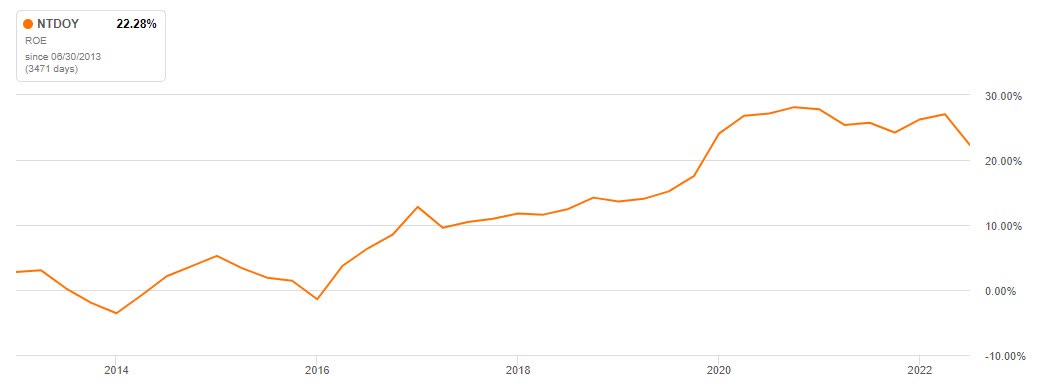

Return on fairness and return on belongings have additionally improved considerably over the past 5 years. As shareholders usually focus extra on ROE as a measure of efficiency, the 22.28% ROE needs to be of actual significance to them. And if they’ll maintain it above 20% for the subsequent few years, which I anticipate, shareholders needs to be nicely rewarded.

The return on capital, however, is down barely to 16.19%, though I usually choose a 5-year common within the 20% vary because it exhibits that they’ll use their capital effectively.

However due to the huge success of the new Mario movie, I feel will probably be a type of blueprint for brand spanking new Nintendo motion pictures, as a result of they’ve lots of attention-grabbing franchises. I might see Zelda positively having lots of potential for a movie or sequence.

With Tremendous Mario Bros. at the moment being the best grossing film in 2023, and simply at this time seeing Mario merchandise being offered in European supermarkets proper on the entrance in a premium location throughout the market, I feel the long run development potential is certainly there.

And I might additionally argue that the Mario motion pictures, given their low prices and excessive revenues, ought to result in a rise in ROC. The chance to spend money on development with maybe over 20% ROC once more ought to result in actually favorable circumstances.

Lengthy-term development alternatives embrace Change 2, motion pictures, theme parks, new video games based mostly on the outdated recipe for achievement, and all of this coupled with a robust administration group that thinks long run and doesn’t wish to please analysts and their over-reliance on quarterly estimates.

Reverse DCF

Writer

To see what’s priced into the inventory, we take the TTM diluted EPS of $2.98 and see what development charges we have to obtain to get to the present share value.

At present, EPS must develop by 11% over the subsequent 10 years to justify the share value. The 5-year realized common was 22.28%, virtually double that determine. And with the brand new technology of consoles and films, I feel EPS might be in step with the 5-year common and even increased within the subsequent few years. So I might argue that the shares are undervalued.

A extremely essential issue for Nintendo is its very strong balance sheet. Zero debt and a money place of 13 billion is about nearly as good because it will get.

Dangers

Nintendo has tried making motion pictures earlier than, and the primary Tremendous Mario Bros. in 1993 was not likely a giant success. It solely has a 29% rating on Rotten Tomatoes. I feel that may have been a consider why they waited so lengthy to make the brand new Mario film.

However I feel the largest threat is that shareholders are usually not the primary precedence in Japan. There are some cultural variations, and Japanese firms usually put the welfare of their workers earlier than profitability, as older persons are extremely revered of their tradition. So it might occur that shareholder returns are a by-product of a well-performing firm and never a precedence.

There’s a small threat that Nintendo’s future video games and consoles is not going to be nearly as good as prior to now, however I don’t assume that would be the case. An organization that has produced top quality content material for nearly 40 years ought to, in all probability, have the opportunity to take action once more.

Conclusion

Given the very sturdy stability sheet and the undervaluation, I feel Nintendo might be a really promising funding for long-term traders. A number of expansions are fairly probably, and matched with rising revenues, this might result in double-digit returns in step with the return on capital over a ten-year interval.

The draw back potential needs to be very small, given the ability and warning of the administration, and the upside potential continues to be massive sufficient to beat the index returns comfortably and even by a large margin.

Editor’s Word: This text discusses a number of securities that don’t commerce on a serious U.S. trade. Please concentrate on the dangers related to these shares.

{kind=link}