Justin Sullivan

Roku, Inc. (NASDAQ:ROKU) has numerous points it’s coping with, however the firm seemingly set a extremely low bar for 2023 with its steerage.

Firm Profile

Roku, Inc. is a tv streaming firm whose working system (OS) powers its personal streaming gadgets in addition to third-party TVs. It additionally started providing its personal Roku-branded TVs in 2023. As well as, the corporate affords varied good dwelling merchandise together with cameras, video doorbells, plugs, mild bulbs, and light-weight strips.

The corporate generates income by the sale of gadgets, in addition to by promoting and content material distribution companies, which it refers to as platform income. Platform income consists of the sale of subscriptions, video promoting in ad-supported channels, transaction-based content material, billing companies, and model sponsorship & promotions.

The agency owns its personal free ad-supported streaming service known as the Roku Channel. It’s accessible within the U.S., Canada, Mexico, and the U.Okay. Within the U.S., Roku Channel offers customers entry to greater than 350 linear channels in addition to on demand content material.

As well as, ROKU has an advert shopping for platform for streaming TV known as OneView. The service lets advertisers arrange, measure, and make any modifications to advert campaigns, whereas offering them engagement analytics.

Alternatives and Dangers

To know ROKU, you really want to grasp its enterprise mannequin. Whereas the corporate is thought for its streaming gadgets, the corporate’s main enterprise is its platform enterprise. Its streaming gadgets are typically offered round value and even as a loss-leader to drive extra customers onto its platform.

In some methods, the ROKU mannequin is much like Apple Inc.’s (AAPL) App Retailer. For paid subscription companies, ROKU typically takes a fee when a service is bought by its platform. By a income share program, ROKU typically takes a 20% cut.

Now, bigger streaming service could also be paying lower than this proportion. Netflix, Inc. (NFLX), the biggest streaming service, has by no means generated a lot income for ROKU, as its clout has helped it keep away from this income share. How a lot newer, bigger streaming companies pay isn’t disclosed, and there have been contractual disputes prior to now, so there are clearly negotiated costs for bigger corporations.

For ad-supported streaming companies, in the meantime, ROKU typically will get 30% of the ad inventory. Now how this works with bigger companies seemingly differs as properly, and not too long ago a number of giant streaming companies have shifted to a mixture of paid subscriptions with advertisements. It took four months for Disney + with advertisements to get onto the ROKU platform as the 2 sides hashed out an ad-share settlement. Whereas the ultimate deal is not going to be disclosed, the Home of Mouse seemingly performed hardball, as streaming companies have turned their deal with profitability over subscriber progress.

Thus, in some ways, ROKU is a play on non-NFLX streaming progress, because it participates in subscriber progress and elevated promoting on different streaming channels which might be bought on its platform.

Beginning in Q2 of final yr, ROKU warned of sudden weak spot within the promoting scatter market, which appeared to hit streamers a little bit tougher than conventional linear TV operators. The corporate blamed a softening economic system and advertisers trying to pull again, however there might be one more reason behind this.

In June, GroupM and promoting measurement firm iSpot.television got here out with a study that stated 17% of advert impressions from streaming gadgets (corresponding to dongles, consoles, and sticks) truly play when the TV is turned off. Whereas on its Q2 call ROKU administration stated it was on the forefront of serving to stop this on its gadgets, that is merely not true, and its gadgets are maybe among the many worst offenders.

The rationale why – its gadgets can’t be powered down by turning off the TV and should be unplugged from the TV or energy supply to be turned off. Anecdotally, I’ve seen that after I flip off my TV watching a streaming present by way of a Roku gadget that I usually discover it a number of episodes forward of the place I had left it off.

This won’t sound like a giant deal, nevertheless it’s estimated that this concern is costing advertisers $1 billion a yr. That’s an issue.

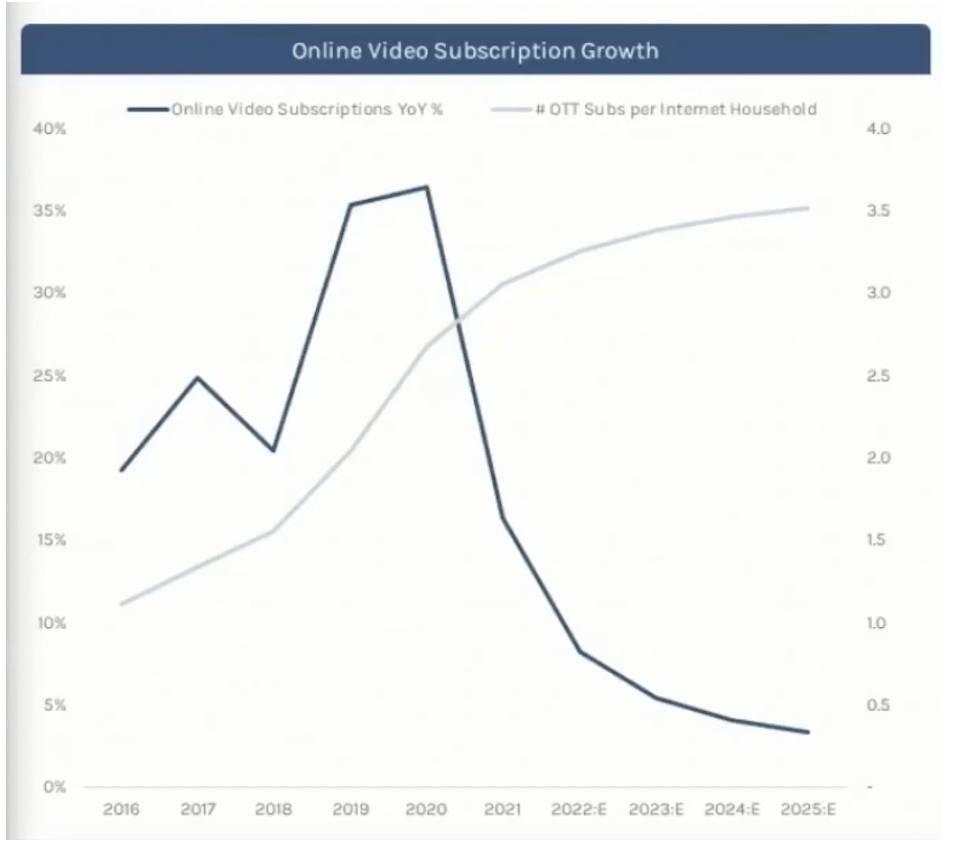

One other concern for ROKU is that OTT sub progress peaked in 2020, and is projected to develop at a a lot slower price going ahead. With over 3 OTT subs per Web family, the marketplace for new gadgets to connect with streaming companies simply isn’t there.

Hedgeye

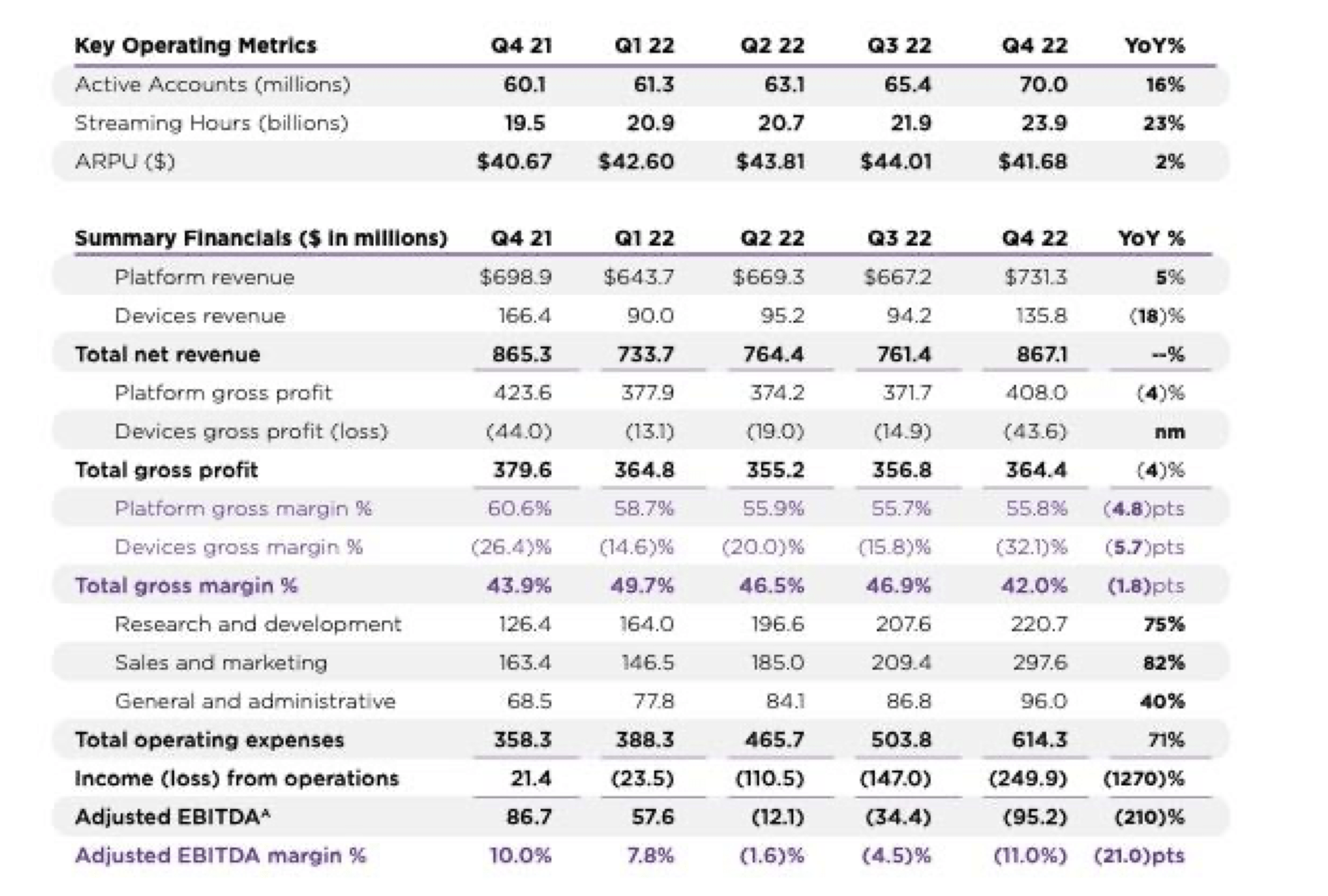

I’d additionally query how ROKU calculates its lively customers. The corporate states that it primarily generates most of its platform and participant income from the U.S. and that worldwide is a small proportion of income. So, presumably, the overwhelming majority of its customers are U.S. households (it defines an lively person as a single account that could be utilized by a couple of particular person, corresponding to a household, whereas noting that one account could also be used on a number of streaming gadgets). Final quarter, ROKU reported that it had 70 million lively accounts. This compares to Netflix reporting that it has 74.3 million paid members within the U.S. and Canada. There are about 131 million total households within the U.S.

To me, both ROKU’s lively account numbers are being misrepresented or it’s reaching fairly excessive saturation within the U.S.

In the meantime, whereas I believe the shift in the direction of ad-supported tiers for the massive streaming corporations is a constructive for them, I don’t assume it is going to be for ROKU. The take-rate ROKU will get from a lot of its clients already appears excessive versus the worth it offers. It’s not offering the pipes into a house like a cable firm, neither is it a duopoly creating refined smartphone working techniques and marketplaces. There are many methods to stream, and a ROKU gadget or a ROKU-powered good TV doesn’t have to be used.

NFLX has by no means paid ROKU something significant given its heft, and I don’t see different giant streamers giving the corporate very favorable phrases in an ad-supported tier. As is typical of ROKU administration, when requested concerning the affect of subscription companies creating ad-supported tiers, they talked about how extra streaming hours is sweet for them. This, in fact, isn’t essentially true as somebody watching extra hours on NFLX doesn’t assist them within the least.

Within the fall, the corporate introduced that it was moving into the house automation market. The corporate plans to supply floodlight cameras, indoor/out of doors cameras, 360° indoor cameras, video doorbells, good mild bulbs, mild strips and each indoor and out of doors plugs. The gadgets have been developed in partnership with low-cost linked gadget maker Wyze.

To me, this transfer appears determined. First, ROKU is delving deeper into {hardware}, when the corporate is primarily an promoting firm. None of those gadgets will assist it promote promoting. As well as, it’s going into an area with numerous well-established gamers corresponding to Nest, which owned by Alphabet (GOOGL), Ring, which is owned by Amazon (AMZN), and Arlo (ARLO). In the meantime, on the higher-end of dwelling automation are typically security-related corporations corresponding to Alarm.com (ALRM) and Vivint.

Wyze, the corporate Roku has partnered with to develop the merchandise, has additionally been on the center of controversy. The corporate did not disclose a safety vulnerability in its safety cameras, and it took three years for it to lastly roll out firmware to repair the problems. The corporate additionally had a significant 23-day knowledge breach in 2019.

Conclusion

Roku, Inc.’s underlying numbers are faltering. Platform gross margins have gone from 65.0% in Q3 2021 to 55.8% final quarter. On the identical time, gross sales and advertising and marketing bills have skyrocketed, whereas lively account progress has cooled. Gross sales and advertising and marketing was up a whopping 82% in This autumn, whereas account progress solely rose 16%. ARPU was up solely 2% year-over-year and truly fell -5% sequentially.

Firm Presentation

ROKU’s EBITDA turned detrimental in Q2 and received worse in Q3 and This autumn. The corporate is projecting -$110 million in EBITDA for Q1 2023. The present consensus for the full-year 2023 is for ROKU to generate detrimental EBITDA of -$299.5 million. The corporate additionally recorded almost $360 million in stock-based compensation in 2022, which is an actual expense that will get excluded within the EBITDA calculation.

Now, one factor seemingly working in ROKU’s favor is that it seemingly simply kitchen-sinked its steerage. And that kind of setup is usually a very good factor, as shares usually get rewarded for beating straightforward steerage. A bigger firm may additionally look to purchase ROKU for its person base, which proper now could be valued at about $110 per sub. On that foundation, it’s not that costly for a big firm wanting to come back in and purchase a bunch of subscribers.

Thus, whereas the numbers and developments look actually poor, I’m going to be impartial on Roku, Inc. right now and price it a “Maintain.” I may transfer to “Promote” on a giant transfer if Roku, Inc. inventory rallies after beating straightforward Q1 steerage.

{kind=link}