dednuel photographs/iStock through Getty Photographs

Funding Thesis

I consider Shopify (NYSE:SHOP) is priced in such a manner that a few years of progress are already included. I take into account the analysts’ estimates to be very optimistic. Gross sales progress has already slowed even earlier than inflation, rising rates of interest and a potential recession put strain on the patron. All this stuff have began in 2022 however want time to unfold absolutely, and I count on we’ll start to see the financial impression this 12 months. Given these dangers, a P/S ratio above ten just isn’t justified in my opinion.

Firm overview

I first heard about Shopify in 2016 when associates began a dropshipping enterprise mannequin by way of Aliexpress (BABA): the web retailer ran through Shopify, the promoting on Fb (META), and when somebody ordered, it was delivered immediately from Aliexpress to the client. For a whereas, this mannequin labored properly, particularly for Fb, which obtained essentially the most important share of the pie. However the mannequin was much less good for the shoppers. Sadly, I missed shopping for Shopify inventory on the time, which was buying and selling beneath $10.

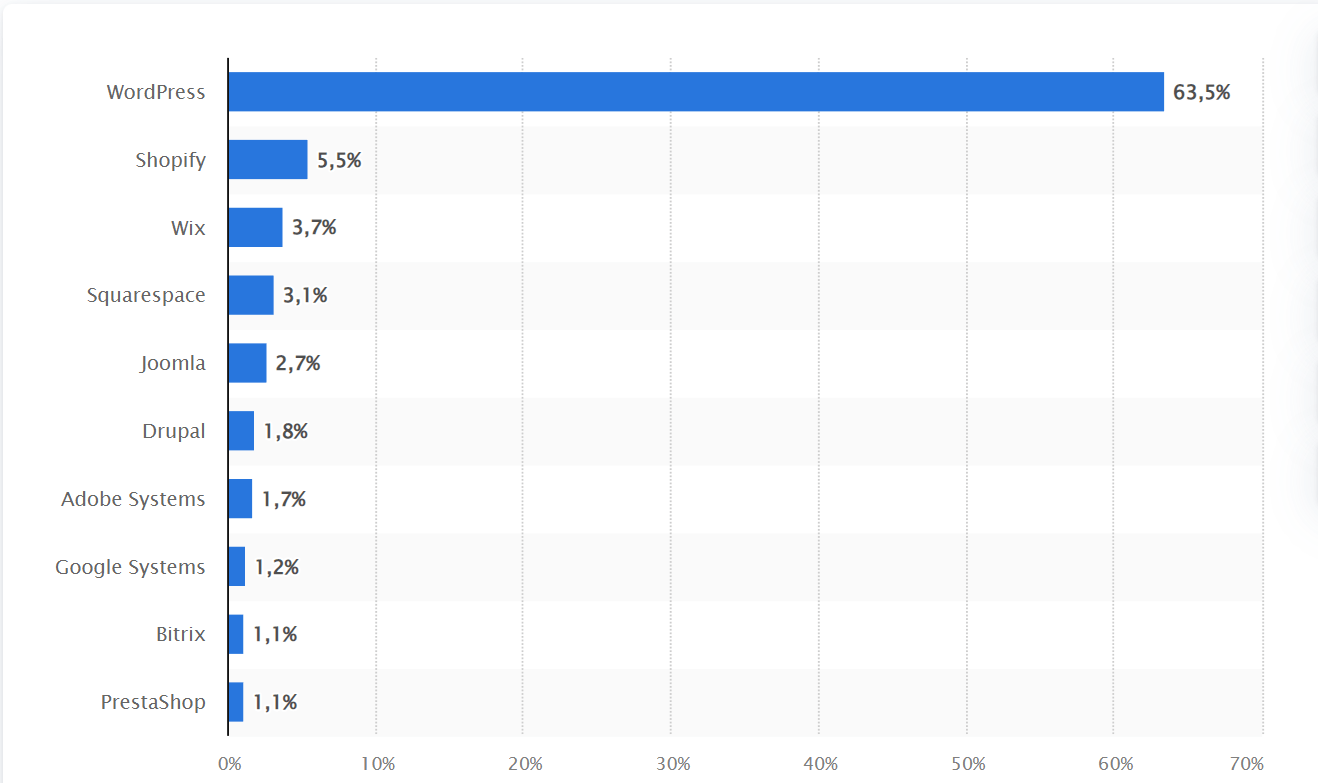

These enterprise fashions have since disappeared, however Shopify has turn into the second-largest content material administration system (CMS). And but the market share is just 5.5% because the free and open-source answer WordPress is main. Nonetheless, it may be mentioned that Shopify nonetheless has a lot theoretical potential to develop, not even counting a rising e-commerce market. Nevertheless, one have to be cautious right here as a result of content-management techniques may be known as something and don’t solely check with shops. The goal group of Shopify is just retailer operators, so thousands and thousands of WordPress customers won’t ever have a cause to change to Shopify.

statista.com

Shopify vs. WordPress

A rising market share of Shopify will come from WordPress and rivals like WIX (and Amazon shedding market share to different, smaller Retailers), so it is price asking why WordPress is so in style with customers. I’ve constructed three web sites with WordPress up to now 5 years, together with a web-based retailer.

The largest benefit of WordPress is its flexibility. All the things may be individualized and outsourced properly as a result of many individuals know the right way to use it: from the web site’s look to particular person coding to the selection of internet hosting servers. It’s an open-source system that provides the person extra management but in addition extra accountability. One other benefit is that WordPress tends to be cheaper and, due to this fact, extra in style with smaller retailer house owners. The draw back is that WordPress will get cluttered extra shortly as you have a tendency to put in many plugins with particular person settings.

The frequent opinion of internet sites evaluating each platforms is that Shopify is far sooner and less complicated to arrange a retailer. One of many greatest manufacturers that makes use of Shopify is Tesla (TSLA).

E-commerce market share

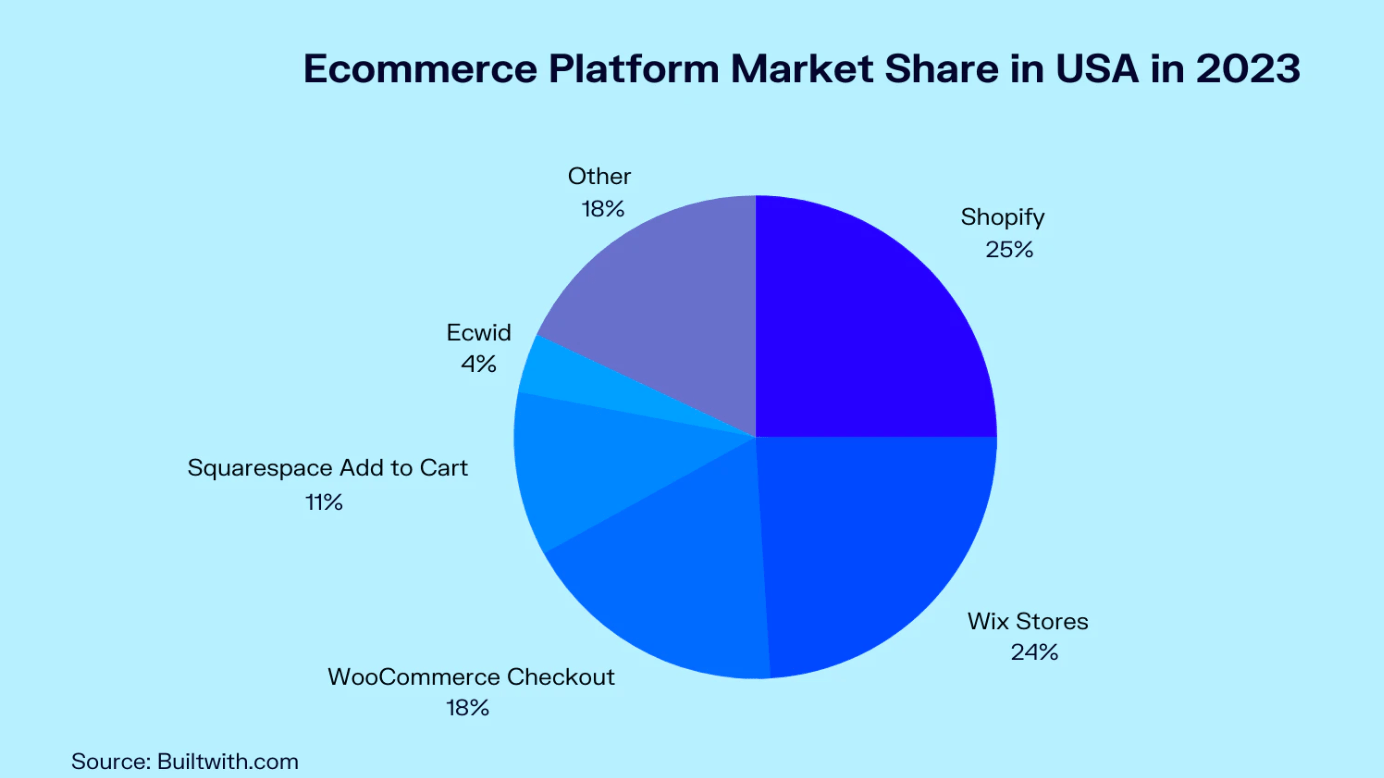

As mentioned, Shopify is a CMS system, however not all CMS techniques are additionally shops. What’s Shopify’s market share in e-commerce? Right here I’ve discovered varied information from about 19% to 25%.

builtwith.com

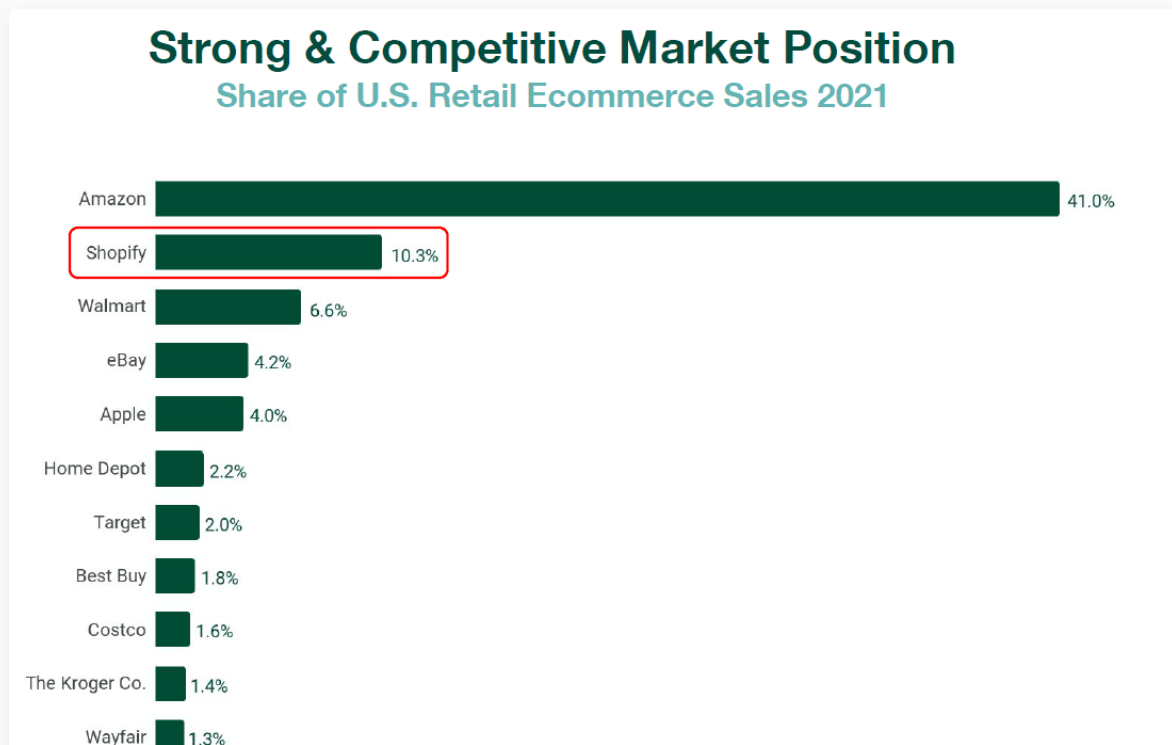

So, inside CMS e-commerce shops, there’s nonetheless a couple of fourfold potential. If you happen to embrace Amazon (AMZN) and the full market, Shopify accounts for about 10% of the U.S. on-line gross sales quantity.

kinsta.com

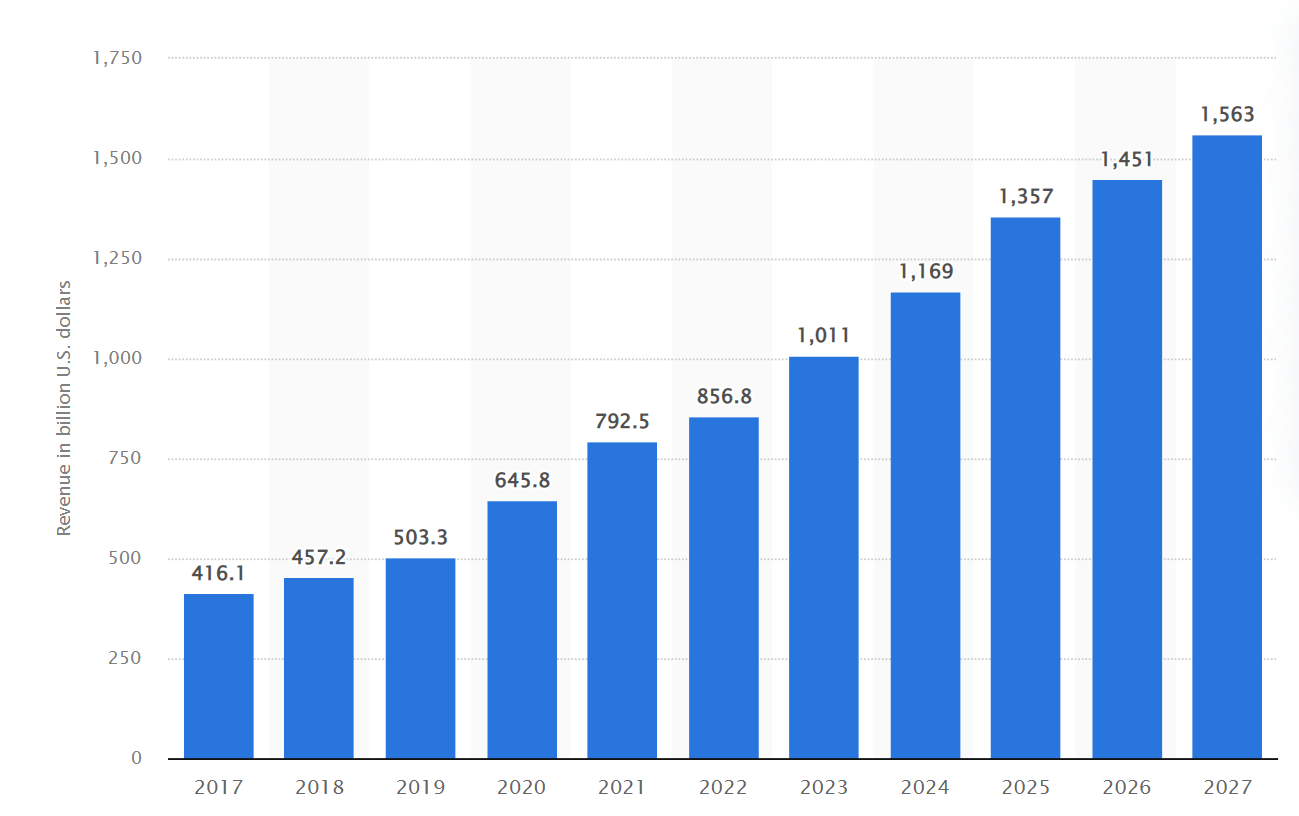

However giving a 10x TAM within the U.S. e-commerce market is pointless, as Shopify won’t ever even come near 100%. It’s a extremely aggressive market in opposition to giants like Amazon but in addition in opposition to different CMS purchasing techniques. However all on-line shops have a standard tailwind: the rising on-line purchasing market. This might double once more from immediately’s degree by 2030 if the next estimate from Statista is appropriate.

statista.com

Due to this fact, I feel a sensible estimate is a continuing market share however twice as a lot income generated by all Shopify shops mixed. A worldwide enlargement for the corporate has far more progress potential. At the moment, america has by far the most important share of Shopify shops, and there are quite a few rising nations with many individuals however only a few shops. In Malaysia, for instance, there are solely 3,600, and in Indonesia, with its 270M inhabitants, just one,400.

builtwith.com

Within the 2022 Investor presentation, nonetheless, the world “Going world” is just talked about in little or no element, which I discover fairly disappointing. Buyers can not assess how a lot focus the corporate places on rising markets. In precept, the next excerpt is the one slide with info, and even that’s fairly sparse.

Investor presentation

General, on-line purchasing nonetheless has loads of room for progress, however one shouldn’t make the error of overestimating it. There could also be a doubling potential in industrialized nations however definitely not 10x. And in some creating nations, there’s nonetheless a 10x potential, however at this level, we can not estimate whether or not nations will create their very own on-line retailer platforms or additionally fall again on Chinese language techniques. The Chinese language Shopify different can be a publicly traded firm known as Baozun (BZUN). And China is the most important buying and selling companion of most nations. So how these relationships unfold in the long run is unclear.

Valuation

The corporate is at present valued at an enterprise worth of $60.5B. Market cap is $64B, so there’s much less debt than money.

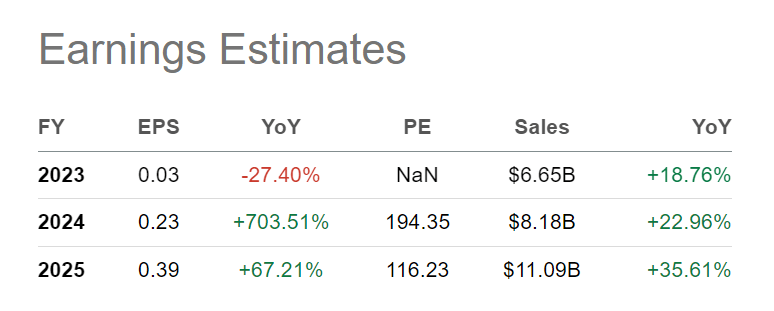

A valuation on a P/E foundation just isn’t potential as Shopify has been worthwhile in only some quarters up to now and has slipped again into unprofitability in 2022. The worth/gross sales ratio may be very excessive at over ten.

Even when the analysts’ estimates are appropriate, the worth/gross sales ratio would nonetheless be 6 in 2025. Furthermore, as mentioned within the earlier a part of the article, I’m not positive the place the expansion is meant to return from anyway because the markets of the industrialized nations are rising, however extra slowly than up to now. Given these circumstances, a YoY income progress of 35% from 2024 to 2025 appears very optimistic.

Looking for Alpha

Lately, the corporate has steadily elevated its workforce. Nevertheless, 10% of the workers has already been laid off this 12 months. Recruiting, customer support, and gross sales are particularly onerous hit. The corporate’s earlier enlargement ambitions, in line with CEO and founder Tobias Lütke, can’t be applied within the present context. The CEO seems critical of himself since he anticipated continued robust progress in e-commerce even after the pandemic.

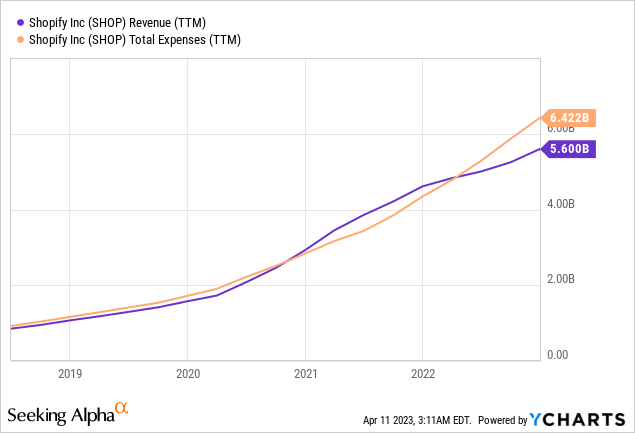

So the aim is to get prices beneath management first, as they’ve been rising sooner than revenues these days. Why are analysts so optimistic when even the CEO says he was unsuitable about progress after the pandemic? Mixed with the specter of recession, I’m very skeptical about these progress figures.

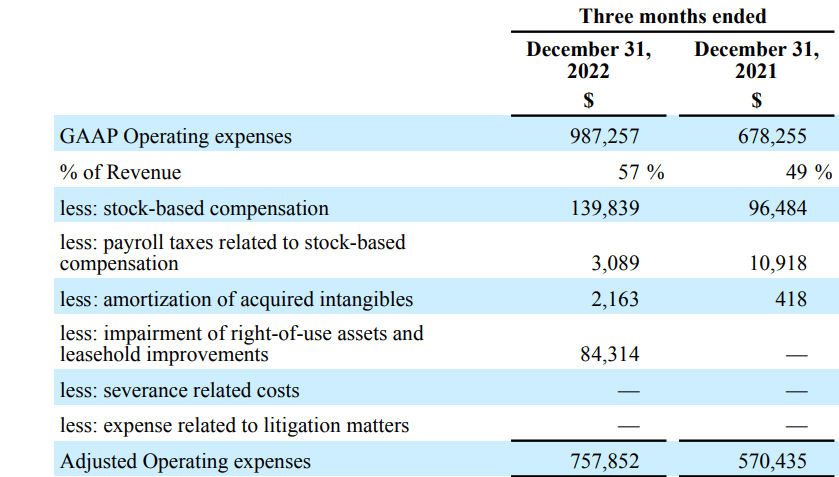

To not overlook that the figures that make the headlines are principally non-GAAP figures, and the GAAP figures often look a lot worse. It is because, amongst different issues, SBCs are hidden on this manner. The GAAP, non-GAAP disproportion is altogether a subject which, for my style, will get far too little consideration. Here is one other instance: in line with GAAP information, working prices elevated YoY by $300M. However after some changes by lower than $200M. Primarily as a result of SBCs and “impairment of right-of-use belongings and leasehold enhancements.”

Shopify 2022 outcomes

Dangers

Shopify began as an answer for small entrepreneurs and freelancers and solely later unfold to bigger firms. Particularly small companies undergo lots from inflation and the specter of recession. Shoppers have much less cash left over for non-essentials. It’s inconceivable to say in figures what number of small on-line shops are in peril of getting to shut, however there’s positively an impression.

Though the share has already fallen by 70% from its peak, it can’t be mentioned that the inventory is now cheaply valued. If one of many subsequent quarterly outcomes unexpectedly disappoints, it might come to a different large sell-off, as we now have seen up to now 12 months after the publication of their quarterly outcomes.

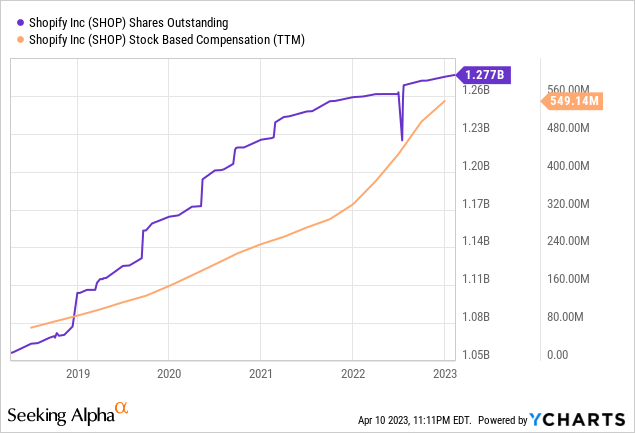

Share dilution and insider promoting

I at all times take note of share dilution and whether or not there’s insider promoting. As well as, it is essential to have a look at stock-based compensations. I’ve not discovered any details about insider gross sales these days. The excellent shares have grown by about 10% since 2020. SBCs added as much as $550M within the final 12 months or 10% of complete income. Which implies a mean of $50k per individual per 12 months with 11000 staff. That is fairly large, and the curve of SBCs remains to be getting steeper.

Conclusion

General, evidently a lot optimism and future progress is already priced in, so the danger of a destructive shock may be very excessive. Or in different phrases, if progress comes as assumed, in all probability not a lot will occur to the inventory, but when it disappoints, it might crash. Development was already slowing down even earlier than inflation, rising rates of interest, and any potential financial downturn pressured the patron. The consequences of those three elements will turn into obvious solely this 12 months. That, mixed with the very excessive valuation and excessive SBCs, I see no cause as an investor to take a position right here in the intervening time. On the optimistic facet, the corporate has no debt, and I consider the CEO has confirmed to run the corporate properly and sustainably for years. The probabilities are that Shopify will nonetheless exist in 20 years, however a few years of progress are already priced in. I feel the almost certainly situation is that Shopify has a couple of tough years forward of them, but when they handle to faucet the huge potential of rising markets, then the corporate ought to have a golden future. Nevertheless, this situation remains to be too far-off and too unsure to make it the idea of 1’s funding thesis.

{kind=link}