Scott Barbour

Sumitomo Mitsui (NYSE:SMFG) is a Japanese banking choose that really stands out in high quality within the present banking make-up. Whereas there’s publicity to declining bonds of their portfolio, they’re very money wealthy and their stability sheet will not be uncovered to the identical dangers because the US banks. Bettering client confidence is doing rather a lot for a few of its segments. The Japanese credit score state of affairs is beneficial for the corporate, and even a slight rise in rates of interest in Japan are prone to lead to a optimistic increment for the corporate. With a sturdy buyback and yield, SMFG truly seems fairly first rate relative to different monetary picks.

Stability Sheet

Beginning with the stability sheet, 30% is cash, with a lot half of that being held in securities of which international bonds are solely a part. Total international bond publicity on the SMFG stability sheet is less than 7%. Whereas it’s common for Japanese banks to carry outsized quantities of international bonds, in SMFG’s case, the massive money balances specifically insulate them meaningfully from any of the banking stability narratives which have been hitting banks usually. In our opinion, the Japanese banking system has little to fret about, additionally on account of their very own financial coverage and the truth that there are massive multi-service banks which might be upholding the economic system.

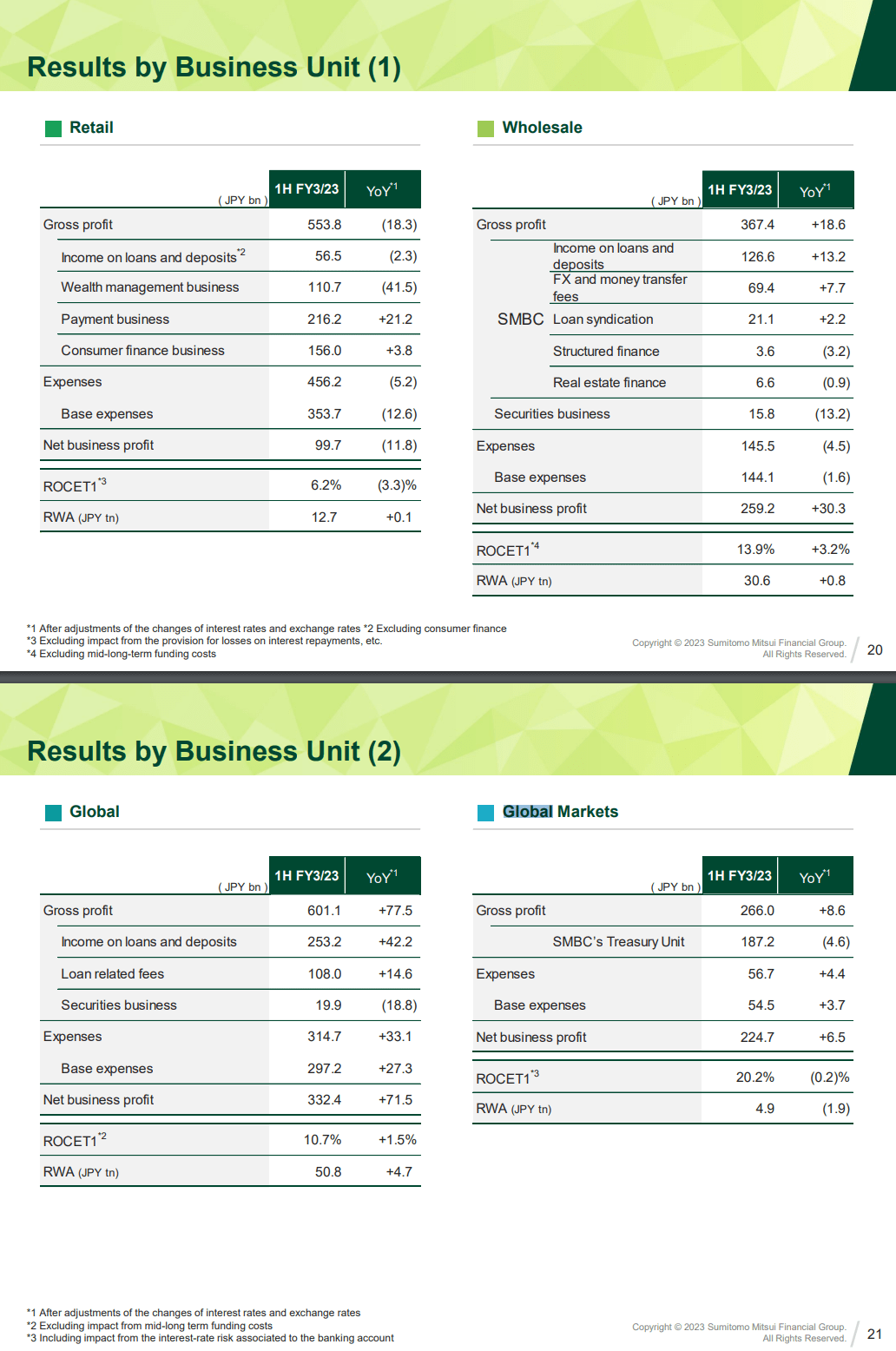

Observe that whereas deposits are substantial, SMFG has different companies that contribute meaningfully to revenue.

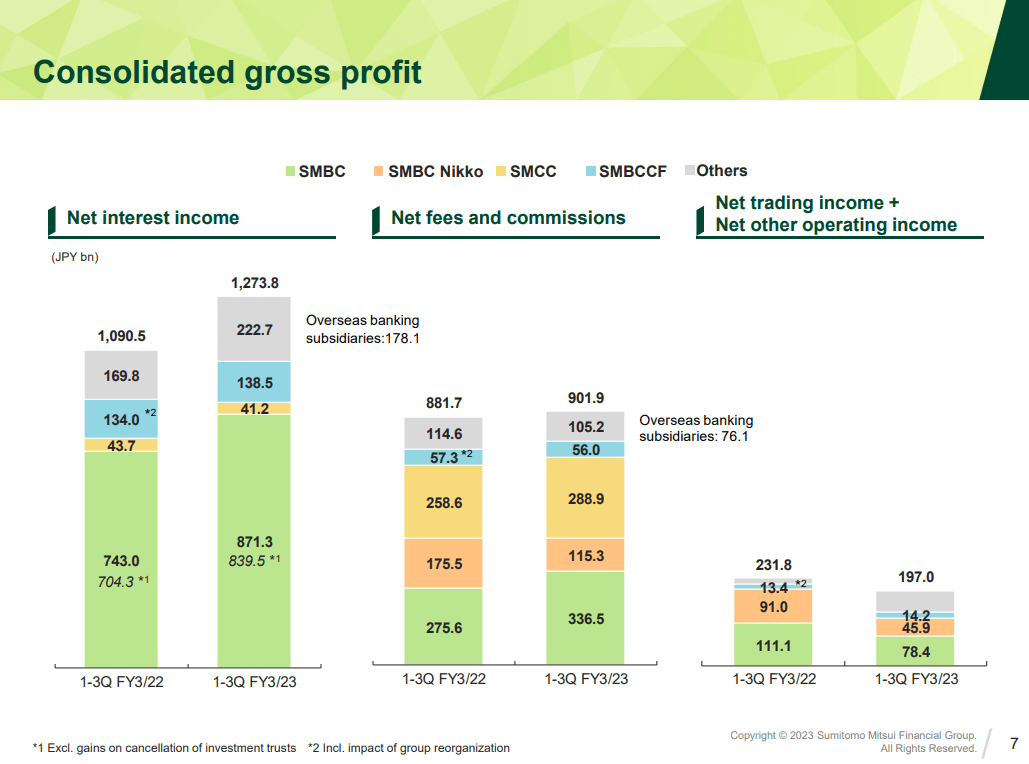

SMFG Snapshot

The SMCC and SMBCCF companies are bank card and client finance companies. Whereas they’re additionally a part of the financial savings and loans construction of the stability sheet, the profile of shorter time period loans signifies that the problems with period hole and solvency threat aren’t actually contributed to by these segments. Restoration of client sentiment in Japan, significantly across the restoration of the Yen, has helped these client going through companies recuperate properly. Basically, mortgage development has additionally helped develop internet curiosity revenue.

Different Phase Breakdown (Q3 2023 Pres)

Companies going through corporates have been doing nicely too, with resumed treasury administration and dealing capital demand serving to out the worldwide markets companies, in addition to the promoting of spinoff merchandise related to larger provide chain and inflation concern amid geopolitical instability.

In any other case, securities going through companies suffered, totally on missing buying and selling income from equities, the place the Nikkei has been comparatively steady and volatility within the Japanese inventory markets fairly minimal during the last yr related to continued financial lodging and comparatively restricted inflation.

All of SMFG’s companies that depend on consumer confidence have accomplished decently this yr, with weak spot primarily being in buying and selling income and the promoting of funding merchandise together with native funding trusts. Basically, retail gross sales of funding funds and home funding merchandise has been a little bit of a catastrophe; the wealth administration enterprise is accountable for virtually all of the adverse forces on the Q3 and cumulative Q3 outcomes. Regardless of this, internet revenue is up within the decrease teenagers YoY.

Reportable Phase Breakdown (Investor Report as of Q3 2023)

Backside Line

A few of the main macro components regarding Japan-facing buyers are associated to the brand new management on the BoJ and sure modifications in financial coverage. Whereas perennially low inflation in Japan has motivated an accommodative coverage, the decline of the Yen has been the first challenge, mirrored additionally within the resilience of SMFG’s enterprise in promoting international bonds, presumably the one product that Japanese buyers are nonetheless shopping for meaningfully. BOJ Chief Ueda is prone to elevate charges barely, however this could energise the buying and selling and different segments of the worldwide markets enterprise. It additionally offers them house to deploy their massive money balances at larger charges, the place they maintain comparatively low ranges of securities in comparison with different main banks. There may very well be some fund inflows again into Japan as retail buyers turn out to be assured as soon as once more within the Yen, which has burned households closely in 2022.

Charges won’t rise sufficient, not even shut, to create the form of credit score and banking issues that exist proper now within the US round latest banking fragilities.

Lastly, we must always touch upon SMFG’s capital return coverage. It’s fairly aggressive, a departure from typical Japanese exercise. Buybacks are fairly excessive at round 3%, and that is on high of a 4% yield that’s prone to be defensible.

We expect SMFG demonstrates resilience within the probably vary of financial eventualities for Japan, and really is a really robust datapoint for why buyers ought to usually be contemplating Japan, whose surroundings is extremely insulated from that of the West on account of its differing credit score surroundings. It isn’t an remoted economic system, however credit score situations are going to be an enormous differential throughout markets and make a giant distinction to the economic system, with Japan being very favourably positioned with what will likely be continued financial lodging, a minimum of relative to different international locations. SMFG is a refreshingly stable establishment because of money balances.

Nonetheless, we nonetheless see higher alternatives out there. A 9x PE is low, however we do not see the necessity to power a banking publicity when there are such a lot of sectors on the market that commerce at even decrease valuations in additional unmined locations out there. SMFG will not be going into our portfolio.

{kind=link}