That’s the virtually gleeful conclusion in an article in the Washington Examiner final December. Now, it’s true they based mostly that conclusion on a Legislative Analyst’s Office report. Nonetheless, that conclusion was based mostly on the (inappropriate) use of the (nationwide stage) Sahm rule to state stage unemployment charges. And as Dr. Sahm has remarked, this isn’t the precise strategy to go — somewhat one wants to look at the suitable threshold for a given state earlier than utilizing it to deduce a recession.

Nicely, let’s check out some indicators.

Determine 1: California Nonfarm Payroll Employment (darkish blue), Philadelphia Fed early benchmark measure of NFP (pink), Civilian Employment (tan), actual wages and salaries linearly interpolated, deflated by nationwide chained CPI (sky blue), GDP (crimson), coincident index (inexperienced), all in logs 2021M11=0. Supply: BLS, BEA, Philadelphia Fed [1], [2], and writer’s calculations.

We now have a considerably bifurcated image — much like that on the nationwide stage — the place employment measures (NFP, early benchmark NFP, and coincident index) present progress by 2023, whereas deflated wages and salaries haven’t recovered to 2021M11 ranges by 12 months’s finish. GDP was rising by 2023 although.

Observe that the coincident index — based mostly on nonfarm payroll employment, common hours labored in manufacturing by manufacturing employees, the unemployment charge, and CPI-deflated wage and wage disbursements — outpaces different measures considerably. For what it’s price, the Philadelphia Fed’s state-level business cycle chronology doesn’t point out a recession in 2023.*

As for recession within the offing, the UCLA Anderson School forecast (March 13) notes:

The California economic system is forecasted to proceed to develop sooner than the U.S. however not by a lot. The dangers to the forecast are the identical as these for the nation: political and geopolitical. There’s the potential for rates of interest to disrupt the present enlargement on the draw back, and elevated worldwide immigration and accelerated onshoring of technical manufacturing on the upside.

The unemployment charge for the primary quarter of this 12 months is anticipated to common 4.7%, and the typical for 2024, 2025 and 2026 is anticipated to be 4.6%, 3.8% and three.9%, respectively. The forecast for 2024, 2025 and 2026 is for complete employment progress charges to be -0.6%, 2.1% and 1.5%. Non-farm payroll jobs are anticipated to develop at a 1.4%, 1.7% and 1.2% charge throughout the identical two years.

Actual private revenue is forecast to develop by 2.0% in 2024, 2.9% in 2025 and a couple of.7% in 2026. Despite the upper rates of interest, the continued demand for a restricted housing inventory coupled with state insurance policies that induce new homebuilding ought to outcome to start with of a restoration this 12 months, adopted by stable progress in new house manufacturing thereafter. Our expectation is for 123,000 web new items to be permitted in 2024, and permitted new items to develop to 159,500 by the tip of 2026. For sure, this stage of house constructing signifies that the prospect for the personal sector to construct out of the housing affordability downside over the subsequent three years is nil.

* Some readers may recall the nice 2017 California-in-recession debate with PoliticalCalculations, here. The Philadelphia Fed fails to establish a recession for California in 2017-18.

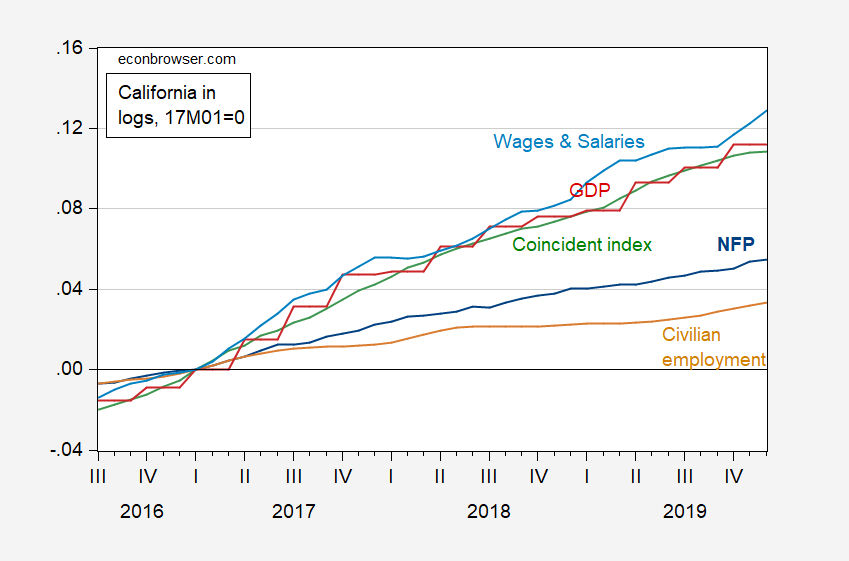

Ironman speculated {that a} recession had begun, on the premise of 12 month transferring common on collection based mostly on the family survey. Right here’s the precise end result.

Determine 2: California Nonfarm Payroll Employment (darkish blue), Civilian Employment (tan), actual wages and salaries linearly interpolated, deflated by nationwide chained CPI (sky blue), GDP (crimson), coincident index (inexperienced), all in logs 2021M11=0. Supply: BLS, BEA, Philadelphia Fed [1], and writer’s calculations.

Conclusion: Beware the household survey employment series at the state level.

That’s the virtually gleeful conclusion in an article in the Washington Examiner final December. Now, it’s true they based mostly that conclusion on a Legislative Analyst’s Office report. Nonetheless, that conclusion was based mostly on the (inappropriate) use of the (nationwide stage) Sahm rule to state stage unemployment charges. And as Dr. Sahm has remarked, this isn’t the precise strategy to go — somewhat one wants to look at the suitable threshold for a given state earlier than utilizing it to deduce a recession.

Nicely, let’s check out some indicators.

Determine 1: California Nonfarm Payroll Employment (darkish blue), Philadelphia Fed early benchmark measure of NFP (pink), Civilian Employment (tan), actual wages and salaries linearly interpolated, deflated by nationwide chained CPI (sky blue), GDP (crimson), coincident index (inexperienced), all in logs 2021M11=0. Supply: BLS, BEA, Philadelphia Fed [1], [2], and writer’s calculations.

We now have a considerably bifurcated image — much like that on the nationwide stage — the place employment measures (NFP, early benchmark NFP, and coincident index) present progress by 2023, whereas deflated wages and salaries haven’t recovered to 2021M11 ranges by 12 months’s finish. GDP was rising by 2023 although.

Observe that the coincident index — based mostly on nonfarm payroll employment, common hours labored in manufacturing by manufacturing employees, the unemployment charge, and CPI-deflated wage and wage disbursements — outpaces different measures considerably. For what it’s price, the Philadelphia Fed’s state-level business cycle chronology doesn’t point out a recession in 2023.*

As for recession within the offing, the UCLA Anderson School forecast (March 13) notes:

The California economic system is forecasted to proceed to develop sooner than the U.S. however not by a lot. The dangers to the forecast are the identical as these for the nation: political and geopolitical. There’s the potential for rates of interest to disrupt the present enlargement on the draw back, and elevated worldwide immigration and accelerated onshoring of technical manufacturing on the upside.

The unemployment charge for the primary quarter of this 12 months is anticipated to common 4.7%, and the typical for 2024, 2025 and 2026 is anticipated to be 4.6%, 3.8% and three.9%, respectively. The forecast for 2024, 2025 and 2026 is for complete employment progress charges to be -0.6%, 2.1% and 1.5%. Non-farm payroll jobs are anticipated to develop at a 1.4%, 1.7% and 1.2% charge throughout the identical two years.

Actual private revenue is forecast to develop by 2.0% in 2024, 2.9% in 2025 and a couple of.7% in 2026. Despite the upper rates of interest, the continued demand for a restricted housing inventory coupled with state insurance policies that induce new homebuilding ought to outcome to start with of a restoration this 12 months, adopted by stable progress in new house manufacturing thereafter. Our expectation is for 123,000 web new items to be permitted in 2024, and permitted new items to develop to 159,500 by the tip of 2026. For sure, this stage of house constructing signifies that the prospect for the personal sector to construct out of the housing affordability downside over the subsequent three years is nil.

* Some readers may recall the nice 2017 California-in-recession debate with PoliticalCalculations, here. The Philadelphia Fed fails to establish a recession for California in 2017-18.

Ironman speculated {that a} recession had begun, on the premise of 12 month transferring common on collection based mostly on the family survey. Right here’s the precise end result.

Determine 2: California Nonfarm Payroll Employment (darkish blue), Civilian Employment (tan), actual wages and salaries linearly interpolated, deflated by nationwide chained CPI (sky blue), GDP (crimson), coincident index (inexperienced), all in logs 2021M11=0. Supply: BLS, BEA, Philadelphia Fed [1], and writer’s calculations.

Conclusion: Beware the household survey employment series at the state level.

{kind=link}