Yuri_Arcurs/E+ by way of Getty Pictures

On Monday, Broadband providers platform supplier Calix, Inc. or “Calix” (NYSE:CALX) reported Q1/2024 outcomes in step with the steering offered by administration within the Q4/2023 stockholder letter:

Regulatory Filings

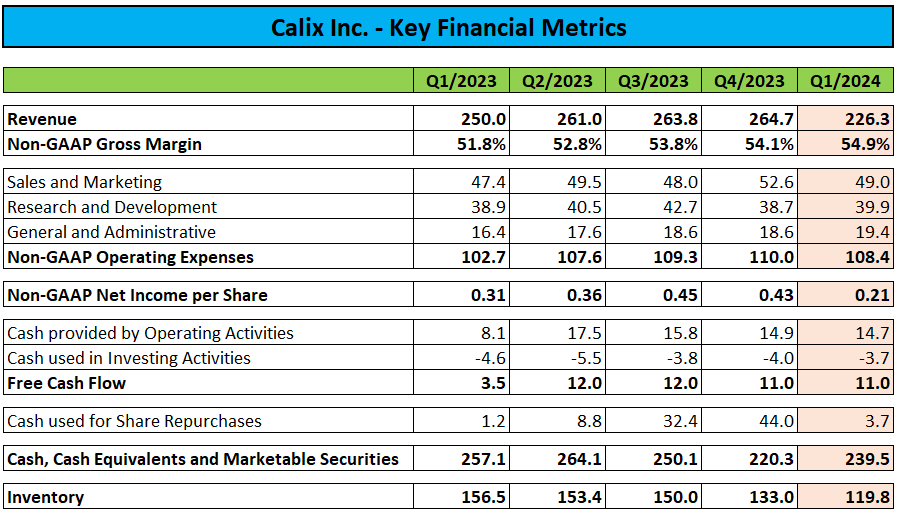

Whereas revenues and profitability had been down each sequentially and year-over-year, gross margins reached new all-time highs.

As well as, the corporate continued to generate strong free money stream and completed the quarter with $239.5 million in money, money equivalents and marketable securities. Calix continues to don’t have any debt.

Following aggressive share buybacks within the second half of FY2023, repurchases slowed right down to $3.7 million in Q1.

Nonetheless, the corporate’s steering for Q2 got here in properly under consensus expectations for a second quarter in a row:

Q1 Stockholder Letter

On the mid-point of the offered prime line vary, Calix will miss analyst expectations by virtually 15% with profitability additionally falling properly wanting the $0.24 consensus estimate.

Whereas administration had warned buyers of momentary headwinds within the firm’s equipment enterprise, they apparently underestimated the magnitude of the affect.

(…) The equipment ({hardware} methods) portion of our enterprise continues to be challenged by three predominant components.

The primary is the continued indecision by our prospects relating to whether or not they apply for BEAD or different governmental funding sources.

The second is the shortening of lead instances to our prospects, which has the impact of decreasing the quantity of shoppers’ stock whereas on the similar time limiting our visibility.

Third, there’s a set of shoppers which have prolonged the analysis of their spending plans into the second quarter of 2024 or have modified their funding priorities for 2024 to focus on including new subscribers in present community builds versus persevering with to aggressively construct new networks.

We imagine every of those components will resolve themselves over the course of this 12 months.

Please notice that administration beforehand anticipated Q1 to mark the low level for the 12 months, with revenues rising sequentially thereafter.

Nonetheless, the brand new stockholder letter is missing an announcement relating to the corporate’s anticipated income trajectory for the steadiness of 2024, which does not precisely bode properly for the second half of the 12 months.

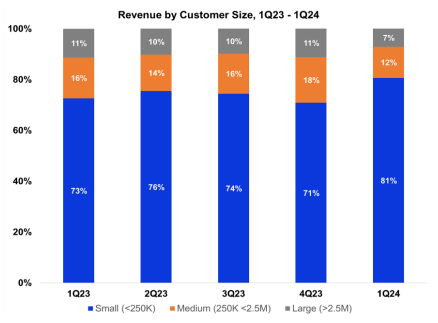

Notably, the corporate’s medium-sized and huge prospects held again on purchases:

Income from medium-sized prospects was 12% of income within the first quarter of 2024, down from 18% within the prior quarter, and decreased 41% in absolute {dollars} due primarily to a few important prospects on this class decreasing their purchases.

Income from giant prospects was 7% of income for the primary quarter of 2024, down from 11% within the prior quarter, and down 46% in absolute {dollars} from the fourth quarter of 2023. The lower was primarily as a consequence of a buyer persevering with to guage their buy plans for brand new community builds.

Stockholder Letter

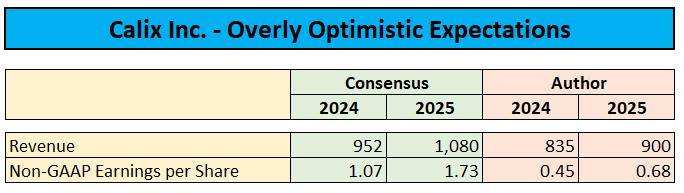

In my view, I don’t count on this sample to reverse within the second half of the 12 months. If true, the corporate’s 2024 revenues and earnings per share could be a far cry from the present consensus estimates of $951.5 million and $1.07, respectively.

Even worse, in accordance with a latest LightReading article, stimulus {dollars} from the federal government’s much-touted $42.5 billion Broadband Fairness Entry and Deployment (“BEAD”) program are actually prone to stream later than initially anticipated, which might additionally put 2025 expectations in danger.

Consequently, I might count on analysts to scale back estimates throughout the board over the subsequent couple of weeks.

Based mostly on assumptions for no materials enchancment within the second half of this 12 months and average development resuming in 2025, a valuation of 37x 2025 earnings per share seems to be wealthy.

Yahoo Finance / Creator’s Estimates

With headwinds probably lasting properly into subsequent 12 months and the inventory not precisely a discount, I see little incentive for buyers to purchase the drop right here.

Backside Line

Calix, Inc. reported Q1/2024 outcomes largely in step with administration’s projections, however for a second consecutive quarter, the corporate’s steering fell properly wanting expectations as bigger prospects held again on equipment buy orders.

Including insult to harm, authorities rural broadband entry stimulus funding would possibly expertise delays, thus additionally placing 2025 estimates in danger.

Consequently, I might count on analysts to scale back projections and value targets throughout the board over the subsequent couple of weeks.

With present headwinds not prone to abate within the close to time period and valuation nonetheless wealthy, I do not see any cause to personal the inventory right here.

{kind=link}